Crizac Limited IPO Review: A Deep Dive into the International Education Recruitment Opportunity

Jul 3, 2025

Crizac Limited, a distinguished B2B education platform specializing in worldwide student recruitment, is poised to launch its Initial Public Offering (IPO) on July 2, 2025, with the subscription window closing on July 4, 2025. This ₹860 crore offering, absolutely an Offer for Sale (OFS), offers an exciting opportunity for investors seeking exposure to the burgeoning global education sector. As an OFS, the company itself will not acquire any proceeds from the IPO, with having the funds and finances often reaping an advantage to the selling shareholders. This comprehensive review about the Crizac IPO delves into Crizac’s business model, financial performance, market dynamics, and related risks to provide investors with holistic information and understanding.

Company Overview and Business Model

Crizac Limited, integrated in January 2011 as GA Educational Services Private Limited and later rebranded in February 2024, operates as a B2B education platform targeted on cross-border student recruitment. The organization facilitates international student placements for higher training institutions in key English-speaking destinations inclusive of the United Kingdom, Canada, the Republic of Ireland, Australia, and New Zealand (ANZ), with a particular strength in recruiting college students from India to the United Kingdom.

Its operational backbone is a proprietary technology platform that seamlessly connects a great network of training agents with global universities. As of March 31, 2025, Crizac had 10,362 registered agents globally having an approximate figure with 3,948 active agents across more than 39 nations, including India, the UK, Nigeria, Pakistan, and Bangladesh. This platform automates essential capabilities like software and application monitoring, document management, and eligibility evaluation, permitting Crizac to process a considerable volume of student applications efficiently. Between FY23 and FY25, the organization processed over 7.11 lakh student programs for more than 173 international establishments, along with renowned universities like the University of Birmingham, Coventry University, and Glasgow Caledonian University.

Crizac's revenue model is mainly commission- based, deriving a percent from the training costs or placement revenue shared by its partner universities. This asset-light model does not directly charge students or agents, which helps low-friction onboarding and scalability. The corporation is established in India with co-primary operations in London, UK, and maintains a global presence through specialists and consultants in international locations inclusive of Cameroon, China, Ghana, and Kenya.

Industry Landscape and Market Opportunity

Crizac operates within the dynamic global student mobility market, which has experienced a large growth, achieving 6.9 million students studying overseas in 2024, up from 4.8 million in 2015. The market is projected to make and expand further similarly to around USD 7.4 trillion by 2030, with better training and higher education being a significant phase. India plays an important position in this trend, being one of the top two nations for international students. In 2023, 1.3 million Indian students pursued their education abroad, that value is projected to exceed 1.5 million by 2025 and acquire 2.5 million by 2030, driven by aspirations for global perspectives and international training. The UK and USA are key locations, with each experiencing a 23% year-over-year growth in Indian enrollments in 2024.

.

The sector is presently processing a rapid digital transformation, moving from legacy specialists to scalable, tech-driven platforms offering automation and transparency. Crizac's B2B generation backbone aligns well with this modification, enabling it to function as a strategic intermediary in India's outbound education market, valued at USD 28 billion (about ₹2.39 lakh crore) in 2023. The corporation is strategically positioned to take advantage from three structural tailwinds: growing outbound student demand from India, international universities outsourcing student recruitment, and the continued edtech-led disruption. Crizac also aims to expand its service offerings to consist of ancillary services like student loans, foreign exchange, and housing, moving closer to a complete-stack "education mobility infrastructure" model.

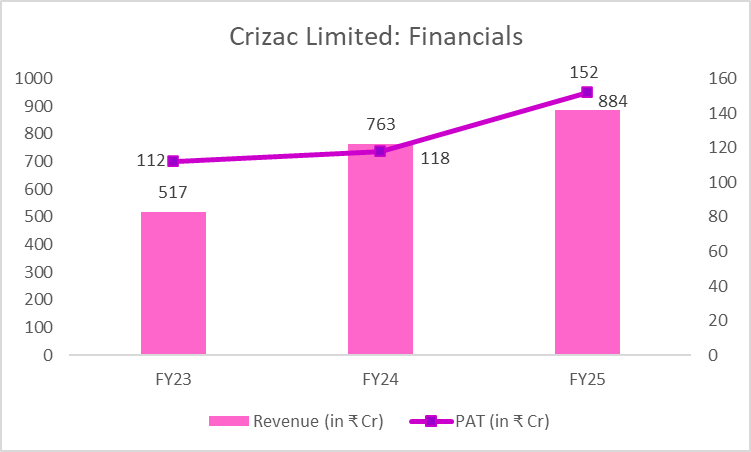

Crizac Limited: Financial Performance

Crizac Limited has demonstrated a robust financial performance over the past three fiscal years, characterized by consistent top-line growth and profitability. The company's revenue from operations has shown a strong upward trajectory, growing from ₹517.85 crore (consolidated) in FY23 to ₹763.44 crore in FY24, and further to ₹884.78 crore in FY25. This translates to a compound annual growth rate (CAGR) of 34.02% in operational revenue between FY23 and FY25.

Profit After Tax (PAT) has also seen healthy growth, increasing from ₹112.14 crore in FY23 to ₹118.90 crore in FY24, and reaching ₹152.93 crore in FY25. The PAT growth from FY23 to FY25 represents a CAGR of 16.78%.

Key profitability margins include an EBITDA margin of 25.05% in FY25, rebounding from 13.52% in FY24, and a PAT margin of 17.28% in FY25. The company also boasts consistently high return ratios, with Return on Equity (ROE) at 30.24% and Return on Capital Employed (ROCE) at 40.03% in FY25.

Crizac maintains an asset-light model with a robust balance sheet, showing total assets of ₹879.62 crore in FY25, up from ₹304.99 crore in FY23. Notably, the company reports zero total borrowings, reflecting a debt-free balance sheet and sound capital discipline. As of March 31, 2025, cash reserves stood at ₹88.827 crore. This financial prudence supports sustainable growth through internal accruals and efficient working capital management.

Promoters and Management Expertise

Crizac Limited benefits from experienced leadership, primarily driven by its three promoters: Dr. Vikash Agarwal, Pinky Agarwal, and Manish Agarwal. These individuals collectively hold approximately 80.48% of the company's pre-offer equity share capital.

Dr. Vikash Agarwal, the Chairman and Managing Director, possesses over 20 years of experience in the education consultancy industry. He was previously associated with Gateway Abroad Ltd. and Crizac Ltd., which operates in the same business line. Manish Agarwal and Pinky Agarwal, co-promoters, have also been associated with the company since 2011 and each bring over 14 years of experience in education consultancy services.

The management team is supported by 368 employees and 12 consultants as of March 31, 2025, who possess deep expertise in the global higher education sector. This strong leadership, coupled with a skilled workforce, contributes significantly to Crizac’s strategic vision and operational success, enabling the company to process a high volume of applications efficiently.

Crizac Limited IPO Structure and Key Details

The Crizac Limited IPO is a Book Built Issue, aggregating to ₹860.00 Crores. The entire difficulty is an Offer for Sale (OFS) of 351.02 lakh stocks, that means no fresh capital can be raised by means of the organization. The price band for the IPO is ready at ₹233 to ₹245 per equity share, with a face value of ₹2 per share.

The IPO subscription duration is from July 02, 2025, to July 04, 2025. The anchor investor bidding is scheduled for July 1, 2025. The lot size for the IPO is 61 shares.

The allotment is expected to be finalized on Monday, July 07, 2025. Shares can be credited to demat debts by Tuesday, July 8, 2025, with refunds initiated on the same day. The stocks are tentatively scheduled to be listed at the BSE and NSE on Wednesday, July 09, 2025.

Objective of the Issue and Utilization of Proceeds

The Crizac Limited IPO is structured as a 100% Offer for Sale (OFS). This means that the company itself will not receive any fresh capital proceeds from the IPO. Instead, the entire ₹860 crore will go to the selling shareholders, primarily promoters Pinky Agarwal (₹723 crore) and Manish Agarwal (₹137 crore).

The primary objective of the offer is to achieve the benefits of listing the equity shares on the stock exchanges. This listing is expected to enhance the company’s visibility and brand image, in addition to provide liquidity to the present shareholders and create a public market for the Equity Shares in India. Investors should be aware that the IPO proceeds will now not be applied for enterprise operations, growth, or debt repayment.

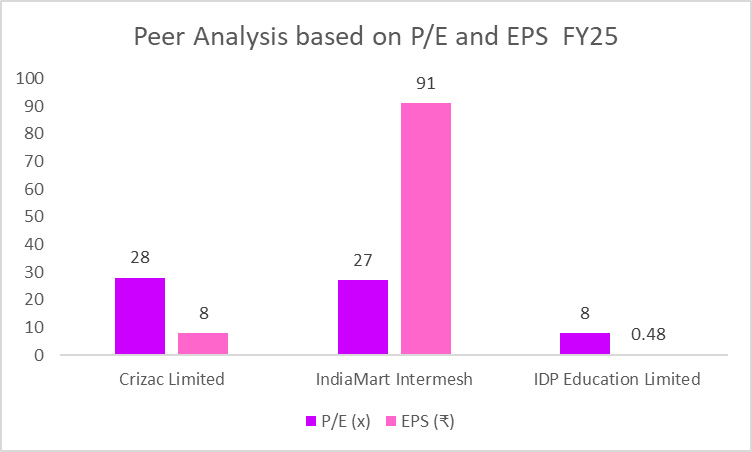

Valuation and Peer Comparison

At the upper price band of ₹245 per share, Crizac Limited's share is valued at a Price/Earnings (P/E) ratio of 28.03x based on its FY25 earnings per share (EPS) of ₹8.74. When in comparison to the industry's average P/E ratio of 17.52x, some analysts recommend the issue seems to be probably overvalued.

Crizac's listed peers, as in line with the provided offer document, encompass IndiaMART Intermesh Limited and IDP Education Limited. A comparative analysis reveals as given within the chart as under:

Strengths and Competitive Advantages

Crizac Limited possesses numerous key strengths and competitive benefits that position it favorably in the worldwide international education sector.

Strong International Student Recruitment Capabilities: Crizac is a leading B2B education platform offering international scholar recruitment solutions, specifically strong within the India-UK training hall, that is the largest outbound scholar marketplace globally. Its community resources applications from over 75 countries.

Deep Institutional Relationships: The organization has cultivated strong, lengthy-standing relationships with over 173 global institutions of higher education, with greater than 20 of its pinnacle and top 30 revenue-generating institutions retaining a relationship exceeding 5 years. These partnerships provide recurring revenue visibility.

Extensive and Diversified Agent Network: Crizac boasts a huge and energetic network, with 10,362 registered retailers globally and 3,948 energetic agents throughout 39 nations as of March 31, 2025. A robust internal machine ensures the selection and nurturing of agents aligned with business enterprise goals.

Scalable, Proprietary Technology Platform: The organization’s cloud-subsidized generation platform gives a centralized system for seamless connections among agents and institutions. This platform helps utility uploads, report management, and AI-driven admission predictions, notably improving efficiency and data safety.

Proven Financial Discipline and Sustainable Growth: Crizac has continuously added profitable increase without relying on external fairness or debt financing, supporting operations absolutely through internal accruals and green running capital management. This is contemplated in continually high Return on Equity (ROE) and Return on Capital Employed (ROCE).

Key Risks and Concerns

Despite its strengths, making an investment in Crizac Limited consists of numerous key risks that capability investors ought to carefully evaluate.

High Revenue Dependence on Select Institutions: A good sized portion of Crizac's revenue is derived from a limited range of global establishments. For example, in FY25, the top three worldwide institutions contributed 53% of sales. The loss or non-renewal of contracts with those key establishments may want to adversely impact enterprise operations and financial overall performance.

Dependency on Active Agent Network: Crizac's business version relies closely on its large and energetic community of worldwide marketers. Any enormous attrition or disruption in agent relationships could negatively affect pupil utility volumes and universal overall performance.

Geographic Revenue Concentration Risk: The agency generates the certain maximum results to some extent provided we can witness the majority of its revenue from the UK (95.12% in FY25, 96.13% in FY24, and 96.42% in FY23). This confined diversification increases exposure to regional regulatory or financial disruptions, which can affect operations and financial stability.

Regulatory and Geopolitical Risks: The business is extraordinarily touchy to global student visa regulations and immigration policy changes. Any inter-country conflicts or global instability can have an effect on scholar enrollment and negatively impact the company’s business operations and future prospects.

Pure Offer for Sale (OFS): Since the IPO is entirely an OFS, no proceeds will be given to the organization, doubtlessly restricting its reinvestment ability and direct investment for future growth initiatives.

Conclusion

Crizac Limited's IPO gives a unique window into a spot, high-boom phase in the global training enterprise. The agency's era-driven B2B platform, coupled with its widespread agent network and deep institutional ties, gives a strong basis for persevered growth. Its strong financial overall performance, characterised by using consistent revenue and profit increase, healthy margins, and a debt-free balance sheet, underscores its operational performance and financial prudence.

However, the pure OFS nature of the IPO means no fresh capital infusion for the company's growth initiatives, and investors must be mindful of the significant revenue concentration on a few institutions and geographies, as well as the inherent regulatory and geopolitical risks. For those with a long-term perspective and a tolerance for the associated risks, Crizac may present a compelling investment opportunity in the evolving landscape of international education.

Stay Connected, Stay Informed –

Don’t miss out on exclusive updates, market trends, and real-time investment opportunities. Be the first to know about the latest unlisted stocks, IPO announcements, and curated Fact Sheets, delivered straight to your WhatsApp.