PhonePe IPO 2025: Digital Payments Giant Targets $1.5 Billion Listing

Jun 30, 2025

PhonePe, a dominant upcoming force in India's digital payments and fintech sector, is poised for a significant Initial Public Offering (IPO) in 2025, aiming to raise approximately $1.5 billion. This strategic decision to go public and shift is anticipated to value the business enterprise at around $15 billion, marking a massive growth from its previous and last private valuation of $12 billion in 2023. The upcoming planned public debut represents a pivotal moment for PhonePe and for India's burgeoning fintech enterprise, signaling the maturation of digital payment structures in the country. PhonePe anticipates filing its Draft Red Herring Prospectus (DRHP) with Indian regulators as early as August 2025, indicating that preparations are gathering massive momentum.

About PhonePe: Journey and Business Model

Founded in December 2015 by Sameer Nigam, Rahul Chari, and Burzin Engineer, PhonePe rapidly emerged as a main digital payments and financial services firm in India. The company's increased growth became considerably reinforced by means of its early adoption and integration with India's Unified Payments Interface (UPI) system, which went live in August 2016. PhonePe's core business model revolves around its mobile software, enabling users to perform a big range of financial transactions, including sending and receiving money, recharging mobiles, paying utility payments, and making in-store payments.

Beyond its foundational payments offerings, PhonePe has strategically varied its services to come to be a complete financial and digital ecosystem. This growth consists of financial services including insurance, lending, and wealth management, along with new consumer technology ventures like Pincode, a hyperlocal e-commerce trade platform, and the Indus App Store, India’s first localized app;ication store. PhonePe generates sales through diversified numerous channels which includes commissions from product promotions on its app, partnerships via its 'Switch' platform, and commissions from cell and phone recharges and also by online purchases. The company additionally piloted processing costs for cell recharges in late 2021, indicating a shift toward diversifying revenues streams even inside its core offerings.

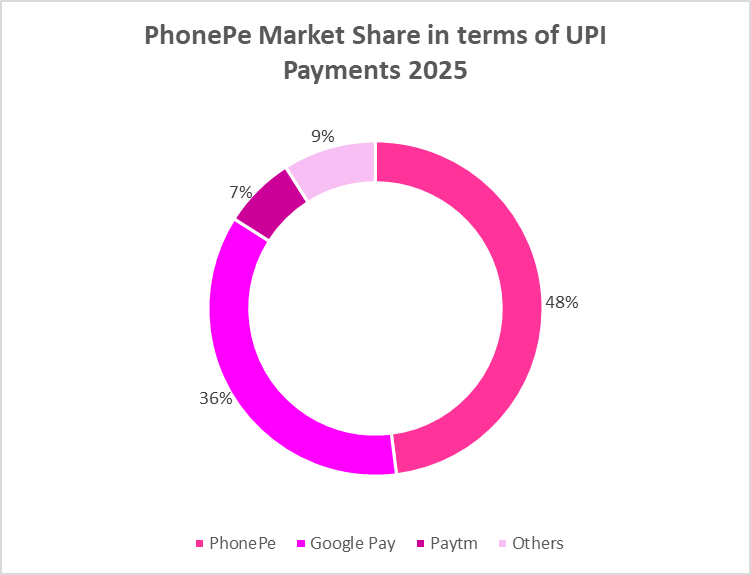

Over the years, PhonePe has grown unexpectedly to be India’s biggest UPI platform by market share proportion, handling nearly half of all UPI transactions in the country. As of 2025, the phonePe platform already serves over 600 million registered users and surpasses more than 40 million merchants, processing close to 310 million transactions daily. As of January 2025, PhonePe accounted for nearly half of all UPI transactions in India, ultimately commanding a dominant 48.4% market share.

Strong Financial Performance Driving IPO Aspirations

PhonePe has demonstrated strong and robust financial growth with a significant growth trajectory in the direction of profitability that lays down a sturdy foundation for its upcoming IPO ahead. In the financial year FY24, the enterprise stated an outstanding operating sales and revenue of ₹5,064 crore, marking a 73% to 74% year-on-year growth from ₹2,914 crore in FY23. This enormous sales increase highlights the accelerating adoption of PhonePe's services throughout India.

Significantly, PhonePe has additionally made significant development in its profitability journey. While it stated a net loss of ₹1,996 crore in FY24, this represents a 28.6% to 29% discount from its ₹2,795 crore loss in FY23. More drastically, apart from employee stock option (ESOP) prices, PhonePe accumulated an adjusted Profit After Tax (PAT) of ₹197 crore in FY24, a terrific turnaround from a loss of ₹738 crore within the previous financial year. The corporation's payments enterprise mainly suggested an adjusted PAT of ₹710 crore in FY24, reinforcing its core operational efficiency, strength and demonstrating a path to average profitability. This overall financial performance is a key factor enabling PhonePe to put together for a public listing.

Unrivaled Market Leadership: Users, Merchants, and Transactions

PhonePe has solidified its function as India's main digital payments platform, commanding an unprecedented marketplace share within the UPI surroundings. As of May 2025, PhonePe processed 47.6% of UPI transactions in terms of volume and an outstanding 50% by value, handling ₹12.56 lakh crore, surpassing its closest competitors.

The platform boasts an immense user and customer base, with over 610 million registered customers as of June 2025, and a significant acceptance network of over 40 million merchants. PhonePe also approaches over 290 million to 340 million day by day transactions, showcasing its essential role in India's digital economy. Its annualized Total Payment Value (TPV) exceeds $1.6 trillion, cementing its leadership position globally, even surpassing businesses like PayPal and Stripe on this metric. A big portion of PhonePe's customers and merchants (85%) are positioned outside India's top eight cities, demonstrating its massive penetration into non-metro areas and its commitment to financial inclusion. In January 2025, PhonePe additionally accounted for over 48% of general UPI transactions, even as Google Pay accompanied with 36.91%, and Paytm's share dipped to 6%.

Strategic Backing from Walmart and Domicile Shift

As we shed light on PhonePe's journey, it has been simply intertwined with Flipkart and its ultimate parent, Walmart. PhonePe was acquired by means of Flipkart in 2016, and finally became part of Walmart's portfolio when the retail giant received a majority stake in Flipkart in 2018. A big improvement prior to the IPO was the entire possession separation of PhonePe from Flipkart in December 2022, allowing both entities to pursue impartial growth paths. Walmart remains the majority shareholder in PhonePe and Flipkart.

This separation and Walmart's continued backing are strategically crucial for PhonePe's IPO. Walmart’s backing and support provides financial balance and credibility, bolstering investor sentiment in PhonePe's business model and sturdy growth potential. The IPO additionally offers an opportunity for Walmart to monetize its investment and unlock cost from its Indian assets.

A key prerequisite for its Indian listing was PhonePe's decision to shift its domicile and abode from Singapore to India. This "reverse flipping" method, finished in December 2022, included an ₹8,000 crore tax charge to the Indian authorities by using its investors, inclusive of Walmart, underscoring the dedication to an Indian public listing and aligning with local regulatory frameworks. PhonePe also converted from a private limited organisation to a public limited company in April 2025, an obligatory step for Indian IPOs, similarly signaling its readiness for enhanced transparency and governance in the public market.

Regulatory Compliance and the Indian IPO Landscape

Navigating India's regulatory landscape is a crucial element of PhonePe's IPO. The process as we know is typically governed by the Securities and Exchange Board of India (SEBI) via and through consideration of its Issue of Capital and Disclosure Requirements (ICDR) Regulations, which resulted in mandate stringent eligibility standards, disclosure norms, and due diligence. PhonePe's conversion to a public limited business enterprise in April 2025 was a prerequisite and crucial aspect under the Companies Act, 2013, to permit it to offer shares to the public.

The corporation's engagement of distinguished investment banks along with Kotak Mahindra Capital, JPMorgan Chase, Citigroup, and Morgan Stanley reflects the dimensions and institutional aid for the IPO. These firms will handle and manage the entire offering, ensuring compliance with SEBI's recommendations on diverse factors, such as the preparation and filing of the DRHP.

A significant regulatory consideration for PhonePe is the National Payments Corporation of India's (NPCI) proposed 30% market share cap for UPI participants. While this cover and cap remains a long-term threat, NPCI prolonged the cut-off date or deadline for compliance to December 2026, offering PhonePe with some breathing room. This regulatory thing, combined with the overall volatility determined in Indian fintech IPOs, underscores the need for PhonePe to demonstrate persisted continuous growth and diversification.

Competitive Dynamics and Diversification Challenges

PhonePe operates in an enormously competitive Indian digital payments market, facing bold opponents along with Google Pay, Paytm, and Amazon Pay. While PhonePe and Google Pay together dominate the UPI panorama, conserving over 80% of the marketplace proportion, intense competition persists, in particular as players expand beyond center payments.

A key mission for PhonePe, in spite of its market management, is its heavy reliance on payments and bills for revenue generation. In FY24, PhonePe's financial offerings commercial enterprise contributed the handiest ₹207.4 crore, a trifling 4% of its overall revenue, with 95% nonetheless derived from its payments business enterprise. This revenue concentration exposes PhonePe to margin pressures, particularly given regulatory changes just like the elimination of Merchant Discount Rate (MDR) furthermore fees on UPI transactions, which affect payment corporations' revenue streams.

While PhonePe has invested significantly in diversifying into insurance, lending, and wealth management, scaling these new verticals has tested difficult. For example, insurance revenues, though growing substantially, nevertheless constitute a small part of the total, and its credit business remains nascent. This confined diversification makes PhonePe more vulnerable to sector-specific downturns or regulatory headwinds impacting the payments space.

Conclusion

The market anticipates PhonePe's IPO with vast enthusiasm, viewing it as a great opportunity to put money into a market leader inside India's hastily expanding virtual economy. The reported $15 billion valuation target is visible as a reflection of its scale, market dominance, and the sturdy backing from Walmart.

However, a few expert evaluations advise caution, specifically in light of the blended overall performance of previous fintech listings in India, consisting of Paytm, whose stock extensively declined post-IPO. Analysts emphasize the significance of scrutinizing PhonePe's long-term period profitability and its capability to diversify revenues streams beyond core payments, which continue to be a dominant portion of its income. The grey market premium for PhonePe's unlisted shares reflects high investor interest but also raises questions on expected potential overvaluation in the pre-IPO marketplace.

Despite those considerations, PhonePe's set up market management, significant user and merchant network, robust economic overall performance, and strategic boom tasks function it as a compelling investment opportunity. The IPO is anticipated to be a landmark event for the Indian fintech sector, providing capital for PhonePe to cement its marketplace position and retain its innovation-driven boom in India’s digital economy.

Stay Connected, Stay Informed –

Don’t miss out on exclusive updates, market trends, and real-time investment opportunities. Be the first to know about the latest unlisted stocks, IPO announcements, and curated Fact Sheets, delivered straight to your WhatsApp.