Waaree Energies Ltd FY24 Results and Business Update

25 September 2024

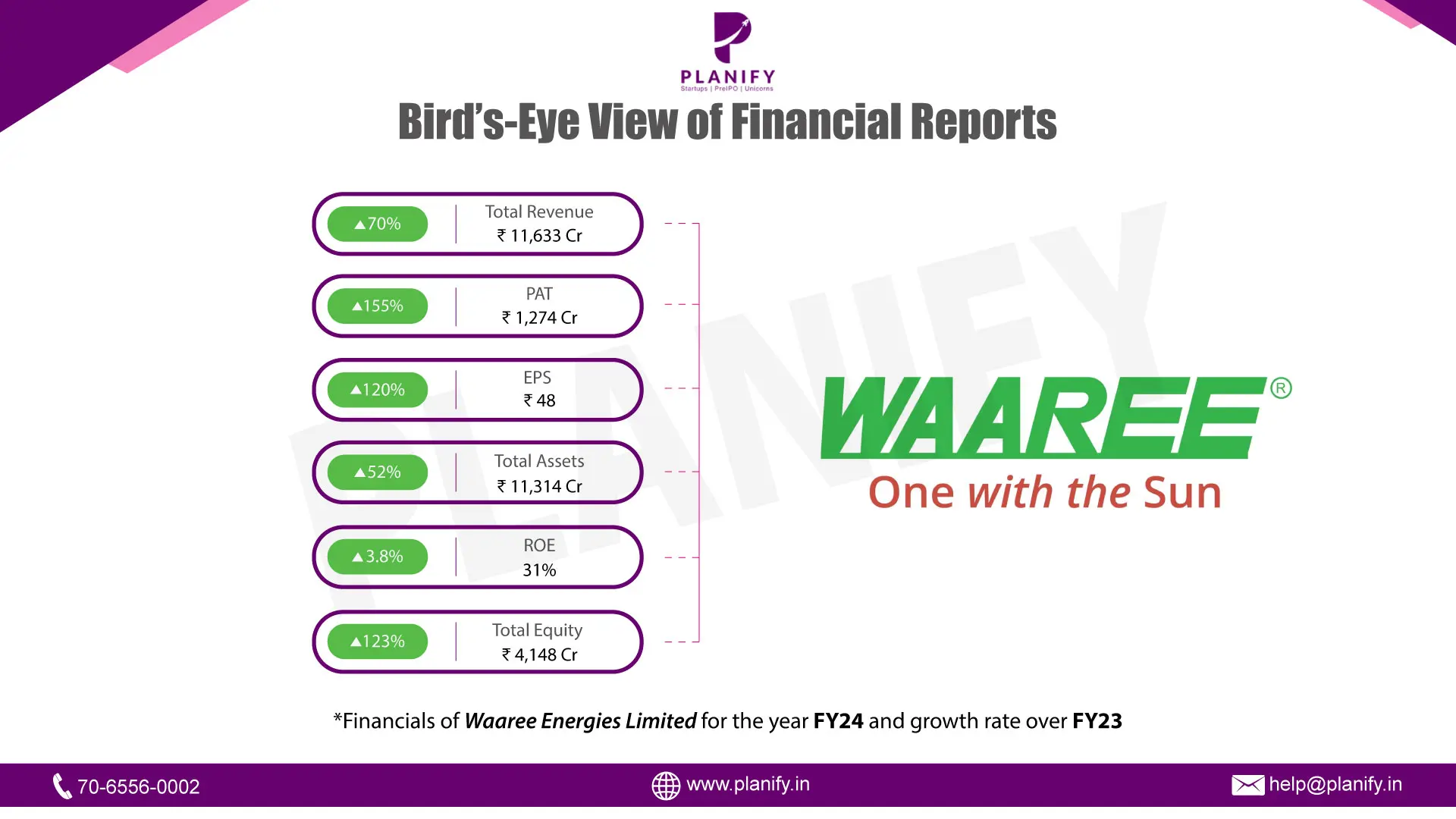

Waaree Energies Ltd, India's largest solar module manufacturer, delivered robust financial and operational results for FY24, marking another year of significant growth and strategic progress.

The company reported an impressive 68.8% year-on-year (YoY) growth in revenue from operations, reaching ₹1,13,976.09 million for FY24. This surge in revenue was complemented by a remarkable 154% YoY growth in profit after tax (PAT), which soared to ₹12,743.77 million. Waaree’s expansion into various verticals of the solar energy business, along with its strategic focus on exports, contributed significantly to these results.

Waaree Energies has maintained a strong foothold in the market with its 12 GW solar module manufacturing capacity, which positions it as a leader in India's renewable energy sector. During FY24, the company executed 704 MWp of EPC projects and managed a portfolio of over 500 MWp in operations and maintenance (O&M) services, further highlighting its execution capabilities.

The company’s order book stood strong at 19,928.12 MW as of March 31, 2024, demonstrating its ability to attract substantial contracts. Moreover, Waaree is focusing on expanding its capacity, aiming to establish 21 GW of solar cell capacity and 11.4 GW of ingot-wafer capacity by FY26-27. This includes the commissioning of a 6 GW fully integrated facility for the production of ingots, wafers, solar cells, and modules in Odisha, along with 1.6 GW of capacity in the United States, solidifying its global expansion ambitions.

Business Strategy and Growth

Waaree’s strategy revolves around capacity expansion, operational excellence, and international growth. The company’s plans to commission 5.4 GW of additional solar cell capacity by FY24-25 are a critical component of its roadmap for growth. Waaree’s ongoing efforts to increase its U.S. manufacturing presence, with a 3 GW facility under development, showcase its strategic intent to tap into global markets, especially in regions like the U.S. where solar demand is rising.

Export sales, particularly to the U.S., have become a dominant revenue stream for the company. In the first quarter of FY24 alone, exports accounted for 73% of total revenue, with the U.S. contributing a substantial 65% of the company’s revenues. Waaree's increasing reliance on international markets does pose potential risks, particularly with regard to fluctuating demand and policy changes in the U.S. However, the company’s leadership in innovation, cost-efficiency, and capacity expansion across markets positions it well to mitigate these risks.

Retail sales, although a smaller part of Waaree’s overall business (contributing 9.96% to total revenue in FY23), continue to grow, supported by programs like the PM Surya Ghar Muft Bijli Yojana. However, this vertical is largely concentrated in Gujarat, and any adverse demand fluctuations from this region could impact Waaree’s business.

IPO Update: A Key Milestone

Waaree Energies Ltd is gearing up for its initial public offering (IPO), which is expected to launch in mid-October 2024, according to recent updates. The IPO is projected to raise ₹3,000 crore through a combination of fresh equity and an offer for sale (OFS) of up to 32 lakh shares. The company received regulatory approval for its IPO on September 20, 2024, and has outlined its plans to use the proceeds for capacity expansion and general corporate purposes.

A significant portion of the funds raised will be utilized to establish a 6 GW ingot-wafer, solar cell, and module manufacturing facility in Odisha, further bolstering Waaree’s production capacity. The OFS includes shares from promoter entities such as Waaree Sustainable Finance Private Limited and Chandurkar Investments, as well as shares from individual shareholders like Samir Surendra Shah.

The company's aggregate installed capacity of 12 GW as of June 2023, and its strategic focus on the U.S. market and retail expansion, provide a compelling investment thesis for potential investors. Additionally, Waaree’s financial performance, with revenues more than doubling from FY22 to FY23 (from ₹2,854 crore to ₹6,750 crore), and a nearly five-fold increase in PAT, showcases the company’s growth trajectory and financial resilience.

Challenges and Risks

Despite its impressive financial performance, Waaree faces several challenges. The company’s heavy reliance on the U.S. market for revenue presents risks associated with geopolitical and trade uncertainties. In FY24, 76.11% of its revenue came from just 10 customers, with its largest customer contributing 20% of total revenue, signaling high customer concentration risk.

Additionally, Waaree’s expansion into retail, particularly in Gujarat, exposes it to regional demand fluctuations. Moreover, the company’s ability to execute its U.S. capacity expansion will be crucial in determining its future growth trajectory, and any delays or inefficiencies could impact its financial performance.

Conclusion

Waaree Energies Ltd has delivered an outstanding performance in FY24, marked by substantial revenue and profit growth, a robust order book, and ongoing expansion in manufacturing capacity. With its IPO set for mid-October 2024, the company is poised to scale new heights, driven by strategic investments in both domestic and international markets. However, navigating risks such as export dependency and customer concentration will be critical to sustaining its growth momentum in the years ahead.

As of FY24, Waaree's EPS stands at ₹48.05 per share, implying that the company's shares are trading at a fair value of ~60 P/E presenting a lucrative investment opportunity.

Stay Connected, Stay Informed –

Don’t miss out on exclusive updates, market trends, and real-time investment opportunities. Be the first to know about the latest unlisted stocks, IPO announcements, and curated Fact Sheets, delivered straight to your WhatsApp.