Planify Feed

Date: Fri 19 Sep, 2025

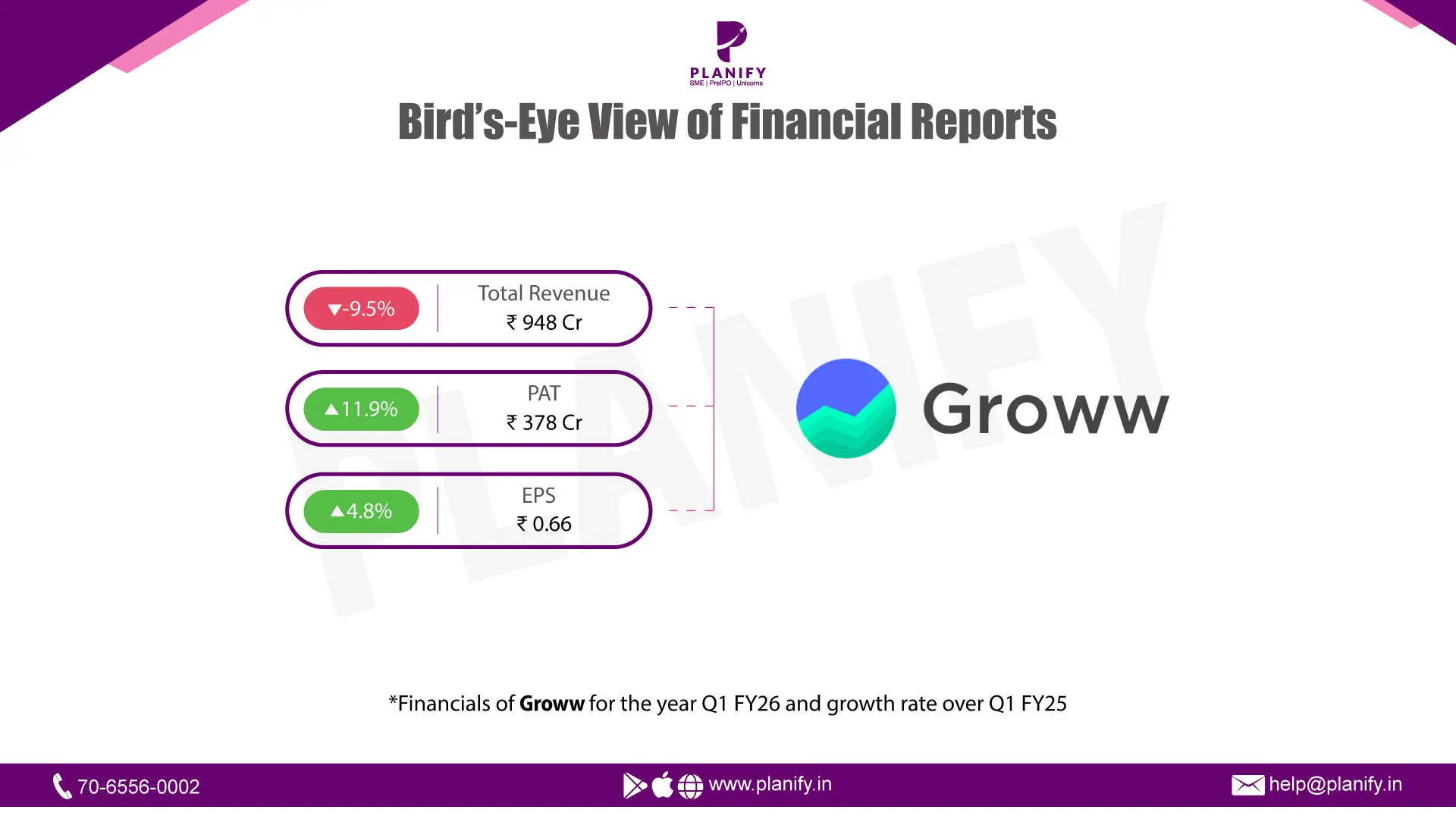

- Financial Performance (Q1FY26 vs Q1FY25): In Q1FY26, Groww reported a dip in revenue, with total income declining 9.5% YoY to ₹948 Cr from ₹1,048 Cr in Q1FY25, primarily due to lower broking commissions. Despite this, operating leverage supported profitability, as Profit Before Tax (PBT) rose 9.7% YoY to ₹503 Cr versus ₹458 Cr last year. Net Profit (PAT) grew 4.8% YoY to ₹378 Cr from ₹338 Cr in Q1FY25, making it Groww’s most profitable first quarter so far.

- Operational Metrics (Q1FY26 vs Q1FY25): Operational performance remained robust, with EBITDA rising to ₹483 Cr, translating into a margin of 50.9%, compared with 40.0% in the same period last year. Net profit margin improved to 39.9% in Q1FY26 from 32.3% in Q1FY25, highlighting efficiency gains at scale. Contribution margin stood healthy at 85.2%, broadly stable YoY, indicating strong cost discipline despite higher transaction volumes. Customer traction also strengthened, as the active customer base grew to 14.38 Mn, a 33.4% YoY increase, while customer assets reached ₹2.61 Lakh Cr, up 59.1% YoY.

- Strategic Developments: Q1FY26 was a mixed quarter for Groww, with softer revenue but record profitability at the bottom line. The company continued to expand its user base and customer assets at a healthy pace, reflecting strong trust in the platform. Efficiency gains supported margins even as trading activity moderated, showing that the business is able to scale sustainably. Groww remains focused on broadening its product suite, deepening engagement with retail investors, and investing in technology to enhance customer experience. With its IPO plans already in motion, the company is positioning itself for the next phase of growth while balancing profitability with long-term expansion.

Date: Fri 19 Sep, 2025

Ever wondered what goes into building the new highways, swanky residential buildings, or even the sprawling renewable energy farms popping up across India? A lot of it starts with something as fundamental as a wire. And quietly, behind the scenes, a company named JD Cables has been laying the groundwork for this transformation. Now, the West Bengal-based manufacturer is stepping into the spotlight with its public listing, aiming to accelerate its growth story in a market that is on the rise.

JD Cables Ltd, a key player in India’s wire and cable industry, is raising ₹95.99 crore through its SME IPO. The company manufactures a wide range of aluminium and copper cables used across power distribution, EPC projects, and industrial infrastructure, and has steadily scaled operations to tap into India’s growing energy and transmission needs.

- The IPO opens on September 18 and closes on September 22. The IPO consists of a fresh issue of ₹84.41 crore and an Offer-for-Sale (OFS) of ₹11.58 crore. Promoter Piyush Garodia will sell 7.6 lakh shares via OFS, while the fresh issue includes ~55.53 lakh new shares. The IPO offered a lot size of 800 shares, requiring a minimum investment of ~₹1,21,600. The company intends to use proceeds largely for working capital, debt repayment, and general corporate purposes.

- What makes this IPO stand out is the strong anchor book backing: a total of 20 anchor investors have committed ~₹27.05 crore, including Alpha AIF VentureX Fund I, HDFC Bank among them, which signals institutional confidence. The listing has also seen a grey market premium (GMP) jump ~20%, reflecting positive market sentiment.

Financially, JD Cables has shown strong growth in recent years. In FY25, revenue stood at ₹250.70 crore (up from ~₹100.85 crore in FY24). Net profit after tax jumped to ₹22.15 crore in FY25 compared to ₹4.58 crore in FY24, indicating strong margin improvement.

In the price band of ₹144 to ₹152 per share, JD Cables is inviting the public to join its journey, hoping to connect the dots between its wires and investor returns.

The wires and cables sector in India is red-hot, driven by a trifecta of infrastructure, real estate, and industrial growth. We've seen other major players in this space, like Polycab and RR Kabel, become market darlings, and JD Cables hopes to follow a similar trajectory.

Date: Fri 19 Sep, 2025

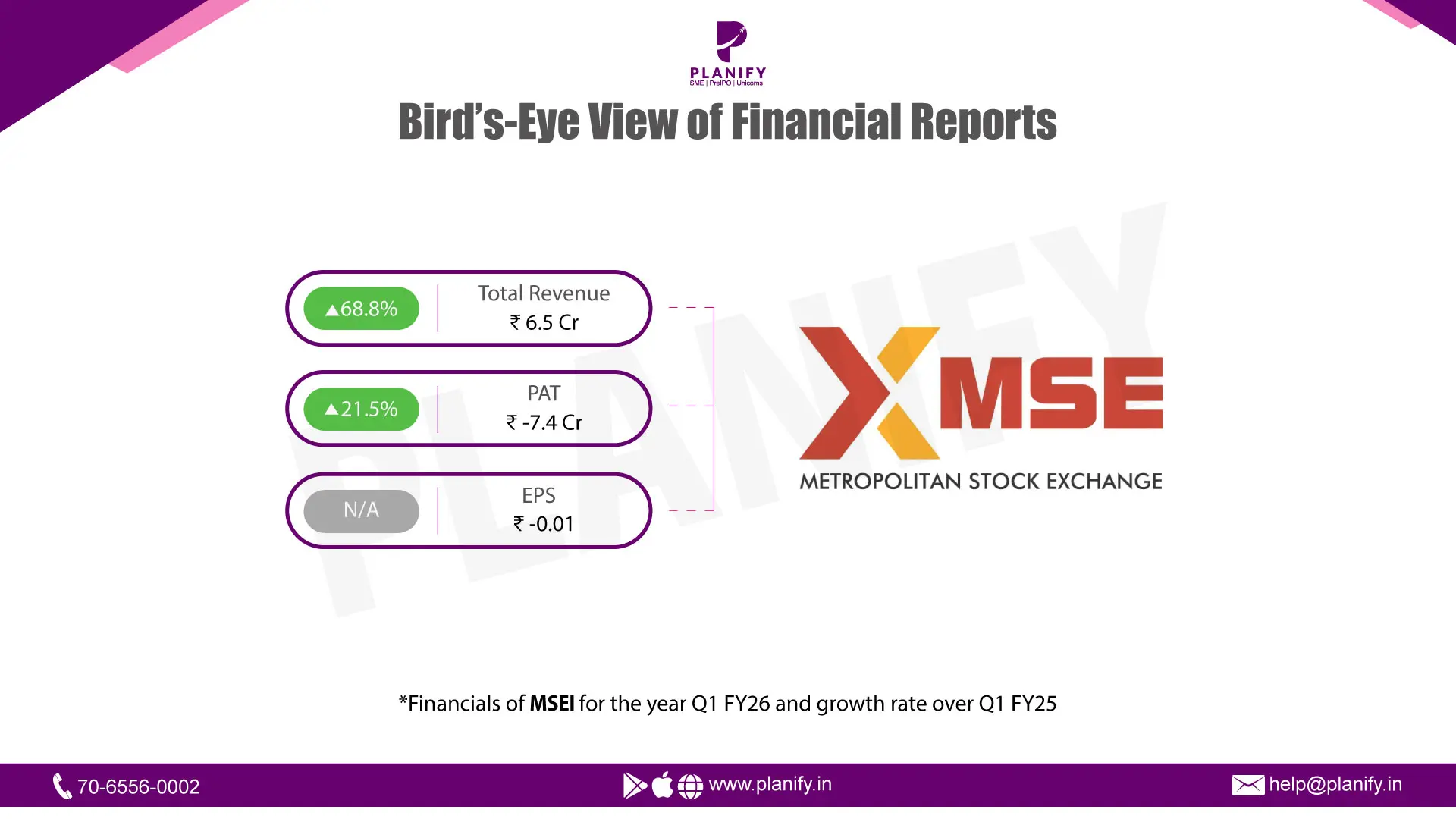

- Financial Performance (Q1FY26 vs Q1FY25): In Q1FY26, MSEI reported a 68.8% YoY increase in total income to ₹6.5 Cr, compared with ₹3.8 Cr in Q1FY25, primarily driven by higher other income (₹5.5 Cr vs ₹2.7 Cr last year). Revenue from operations, however, fell 11.2% YoY to ₹0.95 Cr against ₹1.1 Cr in Q1FY25, highlighting continued pressure in core trading volumes. Operating expenses remained elevated, resulting in a loss before tax (LBT) of ₹7.4 Cr, which narrowed by 21.5% YoY from a loss of ₹9.5 Cr in the prior year. At the net level, the company posted a loss of ₹7.4 Cr, compared with a loss of ₹9.5 Cr in Q1FY25. Earnings Per Share (EPS) improved marginally to ₹ (0.01) from ₹ (0.02) last year.

- Operational Metrics (Q1FY26 vs Q1FY25): Net loss margin improved to (115.2%) in Q1FY26 from (247.6%) in Q1FY25, aided by higher other income cushioning the bottom line. Cost pressures persisted, with employee expenses up 25.7% YoY at ₹4.7 Cr and finance costs rising sharply to ₹0.18 Cr (vs ₹0.06 Cr).

- Strategic Developments:Q1FY26 was marked by significant equity issuance and capital structure changes. The company completed a large private placement of equity shares in January 2025 and further approved an issue of up to 500 Cr shares in August 2025 to reputed investors, strengthening its capital base. Additionally, the reappointment of Ms. Latika S. Kundu as MD & CEO for a three-year term underscores continuity in leadership. While the exchange continues to post operating losses, the improvement in income mix (boost from other income), narrowing of losses, and strengthened equity position provide some stability. However, subdued operational revenue highlights the challenge of reviving core trading activity, which remains crucial for long-term sustainability.

Date: Fri 19 Sep, 2025

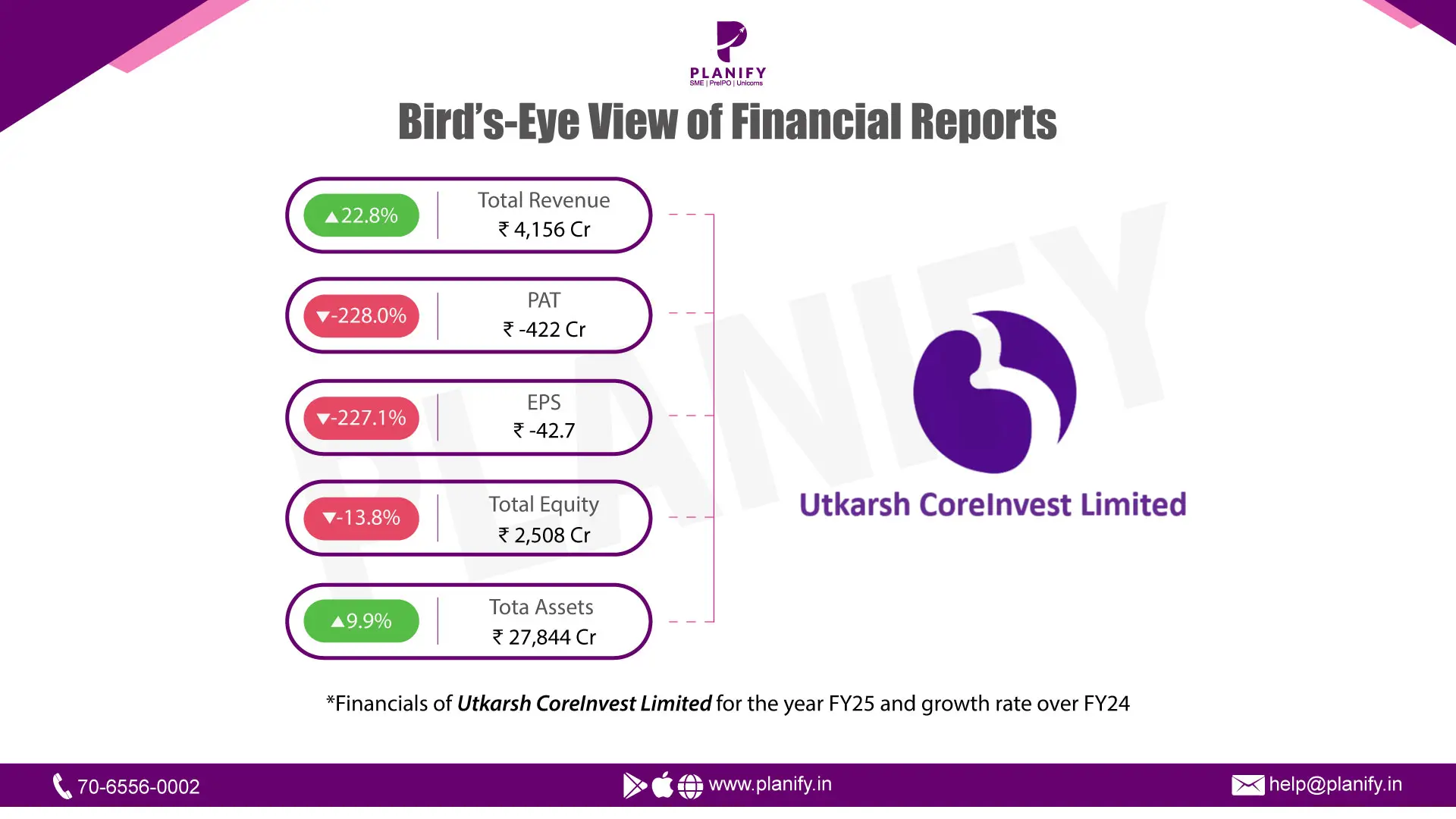

- Financial Performance (FY25 vs FY24): FY25 turned out to be a challenging year for Utkarsh CoreInvest. On a consolidated basis, total income rose by 22.8% YoY to ₹4,156 Cr (vs ₹3,384 Cr in FY24). However, due to significantly higher impairments and operating costs, the company posted a loss before tax (LBT) of ₹556 Cr in FY25 compared to a profit of ₹439 Cr in FY24. Consequently, the company slipped into a net loss of ₹422 Cr in FY25, versus a profit of ₹330 Cr last year. EPS also turned negative at ₹ (42.7) compared to ₹33.6 in FY24. This reversal highlights the severe stress on earnings, largely driven by asset quality issues in its banking subsidiary. On a standalone basis, the holding company remained profitable, posting a PAT of ₹30.3 Cr in FY25, up sharply from ₹1.4 Cr in FY24.

- Operational Metrics (FY25 vs FY24): Despite income growth, profitability metrics worsened. The net profit margin dropped to (10.2%) in FY25 from a healthy 9.8% in FY24, reflecting a combination of higher credit costs and weaker operating leverage. Operating margins also contracted as provisions for impairment surged to ₹1,370 Cr in FY25 (vs ₹378 Cr in FY24), a nearly 3.6x increase. On the balance sheet side, consolidated net worth stood at ₹2,508 Cr as of March 31, 2025, compared to ₹2,911 Cr in FY24. Asset quality sharply deteriorated. The Gross NPA ratio spiked to 9.4% in FY25, up from 2.5% in FY24, while the Net NPA ratio rose to 4.8%, versus just 0.03% last year. This erosion in asset quality was the key driver behind the losses and remains the most pressing risk.

- Strategic Developments: FY24, Utkarsh Small Finance Bank (the main subsidiary) got listed, expanding its visibility and capital market access. The bank grew its deposit base by 23.5% to ₹22,235 Cr in FY25 as compared to ₹17,998 Cr last year. Despite weak profitability, the company maintained a comfortable CRAR of 20.9%, though lower than 22.6% in FY24. During FY25, Utkarsh CoreInvest advanced the merger process with Utkarsh Small Finance Bank, which received final board approvals in September 2024 and RBI’s NOC in January 2025. This reverse merger is expected to streamline operations, strengthen capital, and reduce structural overlaps. Going forward, management has indicated sharper focus on improving asset quality, rebalancing towards secured lending, and leveraging technology to drive efficiency and customer acquisition.

Date: Thu 18 Sep, 2025

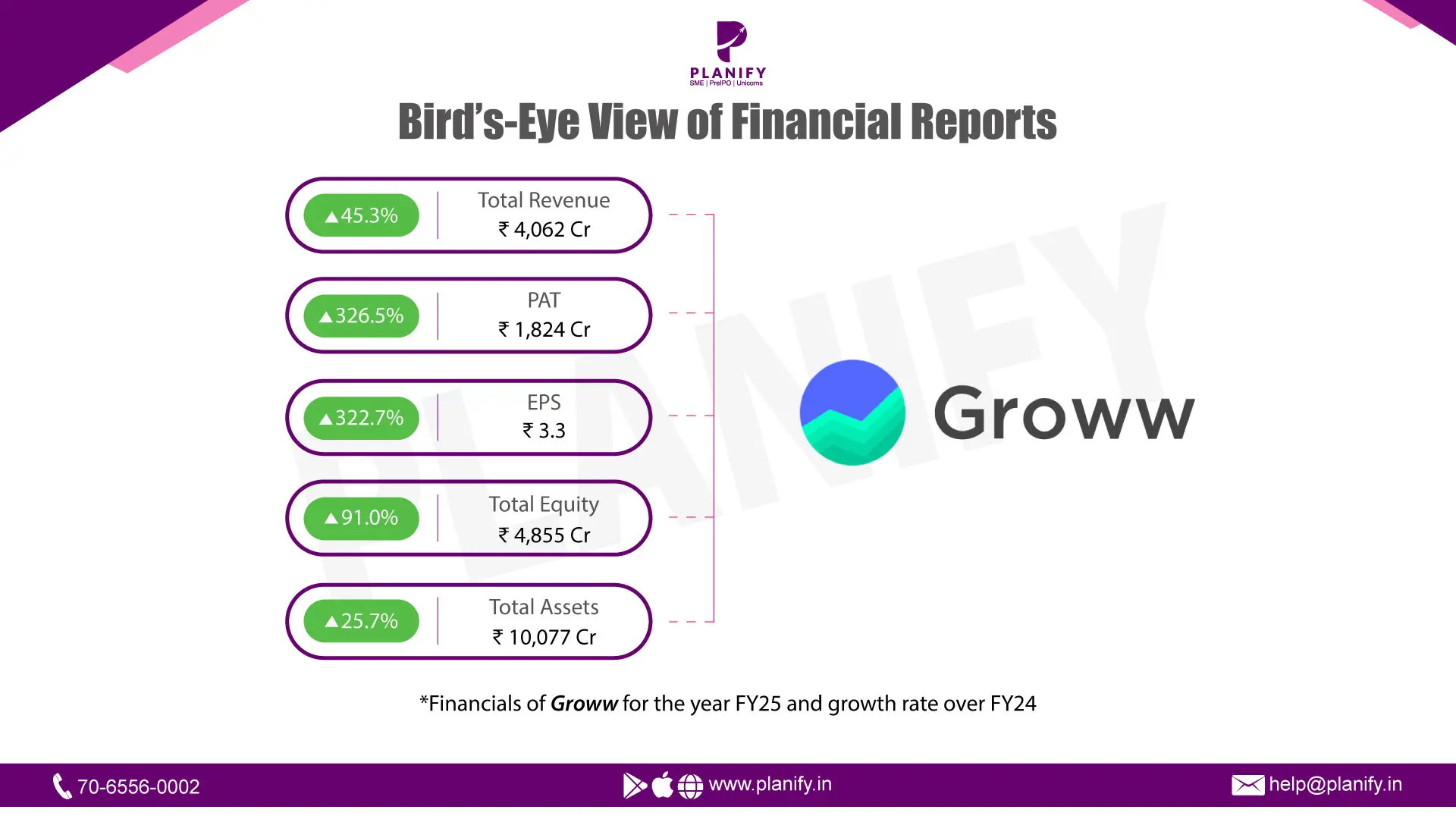

- Financial Performance (FY25 vs FY24): Groww delivered a very strong FY25 with a sharp turnaround from losses in the previous year. Total income for the year rose by 45.3%, reaching ₹4,062 Cr compared to ₹2,796 Cr in FY24, driven mainly by higher broking commissions and a sharp jump in interest income from margin funding. Profit Before Tax (PBT) stood at ₹2,464 Cr in FY25, against a loss in FY24, reflecting strong operating leverage and absence of one-off expenses. Net profit (PAT) came in at ₹1,824 Cr, reversing the ₹806 Cr loss last year.

- Operational Metrics (FY25 vs FY24): Groww’s profitability and customer metrics improved meaningfully during the year. EBITDA expanded to ₹2,306 Cr with margin improving to 59.1% from 56.4%, showing better efficiency as revenues scaled up. Net profit margin recovered to 44.9% in FY25 from a negative 28.8% in FY24. Contribution margin remained stable at 85.4%, reflecting effective cost control despite higher scale. The active customer base increased by 47.8% to 13.9 Mn, while total customer assets surged by 78.6% to ₹2.17 Lakh Cr from ₹1.21 Lakh Cr in FY24. Strong growth in revenues per employee and consistent operating leverage supported higher earnings, even as technology and transaction costs rose with higher trading volumes.

- Strategic Developments: FY25 proved to be a landmark year for Groww, with record profitability, strong user growth, and rising customer assets reflecting the company’s ability to scale efficiently. Operating leverage supported stable margins, even as investments in technology and infrastructure continued. To build on this momentum, Groww has filed for an IPO in 2025. The proposed listing aims to strengthen its capital base, widen product offerings, and accelerate investments in digital platforms. It will also provide an exit route for existing investors and enhance visibility in India’s growing wealth-tech space. Looking ahead, the company plans to deepen customer engagement, expand in underserved markets, and drive adoption of newer products such as margin financing and lending. While Groww has emerged as a profitable fintech leader with growing market share, maintaining margin discipline in an increasingly competitive broking industry will remain a key focus area.

Date: Thu 11 Sep, 2025

Notice of the 1st Extra Ordinary General Meeting (“EGM”) of Incred Holdings Limited, which is scheduled for Wednesday, October 1, 2025 at 12:00 Noon (IST) through video conferencing (“VC”)/ other audio-visual means (“OAVM”) to transact the following businesses:

Special Business:

To consider and if thought fit, to pass, with or without modification(s) the following resolution as a Special Resolution:

- Approval of the initial public offer of equity shares of the company through a fresh issue and an offer for sale of equity shares of the company: The Company plans to raise up to ₹1,500 crore through a fresh issue of equity shares via IPO (book building method), with pricing and terms decided by the Board based on market conditions. The new shares will have the same rights as the existing shares.

- Approval for increasing the limit of investment by non-resident Indian or overseas citizen of India in the share capital of the company: The Company seeks shareholder approval to raise the NRI/OCI investment limit from 10% to 24% of its paid-up equity capital as per FEMA rules.

- Approval for adoption of the altered articles of association of the company

- Approval for amendment of the employee stock option plan of the company

Instructions at glance

Cut-off date | Wednesday, September 24, 2025 |

Commencement of remote e-voting | Friday, September 26, 2025 at 09:00 A.M. (IST) |

End of remote e-voting | Tuesday, September 30, 2025 at 05:00 P.M. (IST). |

AGM | Wednesday, October 01, 2025 at 12:00 Noon (IST) |

Date: Wed 10 Sep, 2025

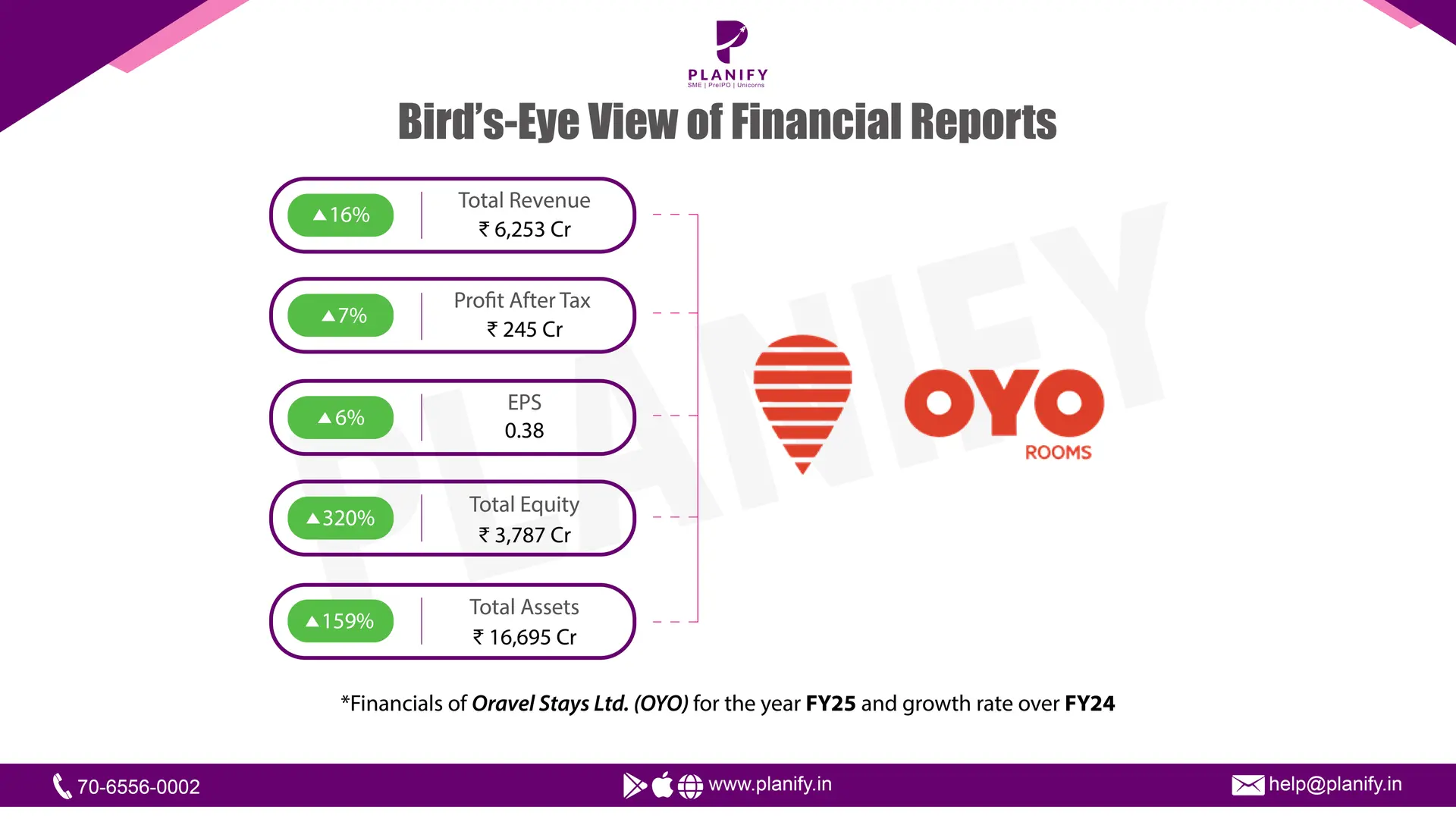

- Financial Performance- For FY25, the revenue of the company has increased by 16% from Rs. 5389 Cr. in FY24 to Rs. 6253 Cr. in FY25, as in recent years, the company has expanded well beyond its original budget hotel model into multiple countries, the homes segment and more. Its portfolio now includes vacation homes, luxury and experiential stays, such as Sunday Hotels and Pallette Hotels), its European brands DanCenter, CheckMyGuest and Belvilla, extended stay accommodation, such as Studio 6 through its acquisition of US hospitality giant G6 Hospitality, workspaces (such as Innov8), hospitality technology solutions and more. The Company maintained PAT positivity throughout the fiscal year, recording a profit of Rs. 245 Cr in FY25 ( 7% up from FY24), reflecting consistent performance improvements and built-in operating leverage driven by strategic expansion across premium segments, integration of acquisitions, and technology-led operations, Resulting in the increased EPS of the company by 6% from Rs. 0.36 in FY24 to Rs. 0.38 in FY25.

- Financial Position- The company’s total assets rose sharply from ₹6,443 Cr. in FY24 to ₹16,695 Cr. in FY25, supported by strong expansion across segments. Between March 2023 and March 2025, the homes portfolio grew organically from 79,000 to 1,20,000 storefronts, while hotels expanded from 13,000 to 21,000. Further scale came from the integration of CMG (2,000 storefronts) and G6 Hospitality (1,500 storefronts). Equity also surged 320% to ₹3,787 Cr. in FY25 (from ₹901 Cr. in FY24), driven by fresh issuance of equity and preference shares and an 11% rise in securities premium reserves.

- Future Outlook- The company plans to accelerate growth in the premium hospitality segment by scaling brands such as Sunday, Townhouse, Collection O, and Palette, while continuing to invest in technology, allocate capital prudently, and expand in high-potential markets like the US. It also aims to boost customer loyalty, drive operational efficiency, prepay Term Loan B opportunistically, and pursue value-accretive acquisitions to enhance its balance sheet and global presence. By March 31, 2025, the company was serving over 100 million customers across more than 35 countries, with industry trends signaling sustained global travel demand, though varying by region and segment.

Date: Tue 09 Sep, 2025

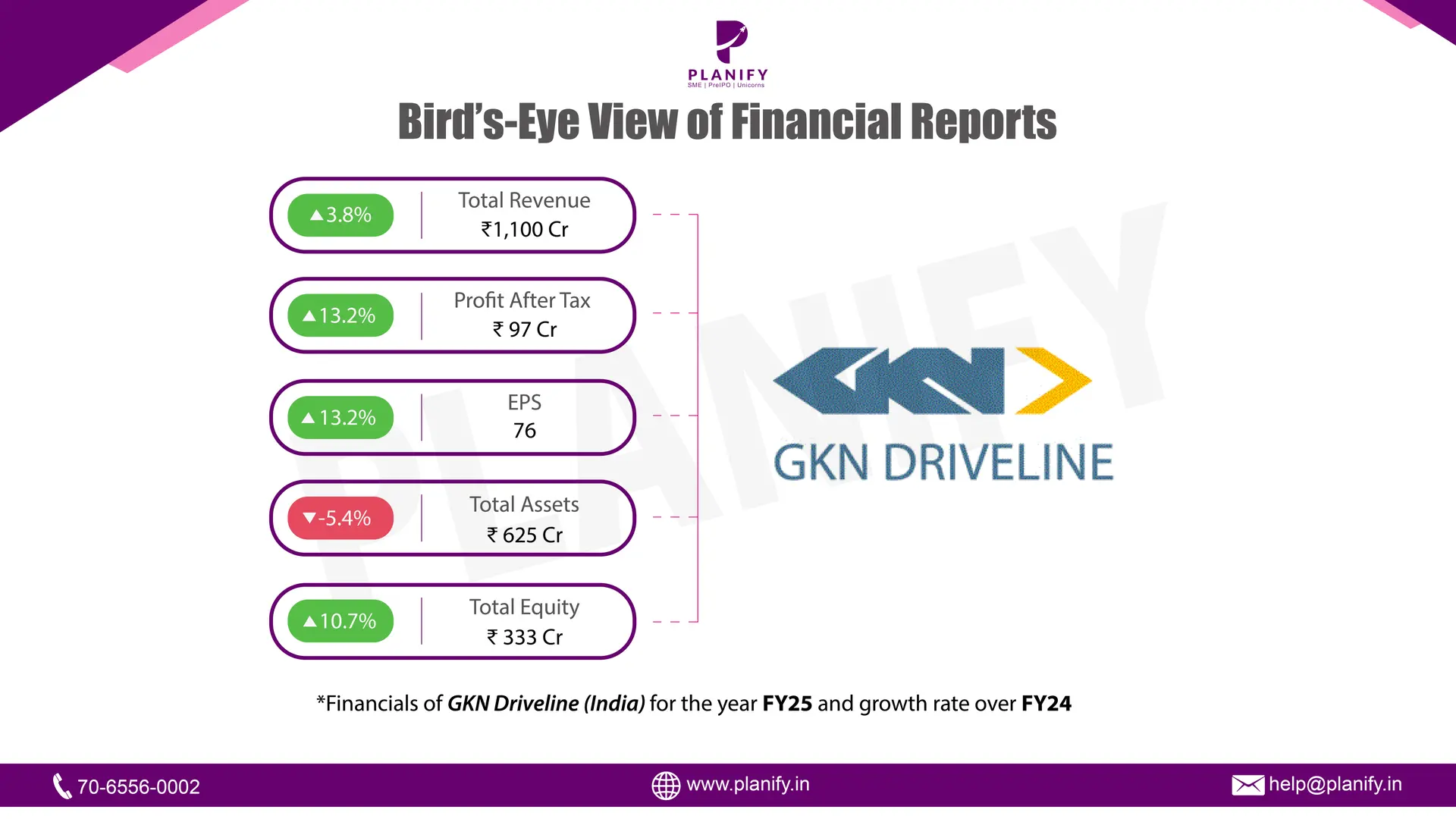

Financial Performance (FY25 vs FY24): GKN Driveline (India) delivered steady topline growth in FY25 despite a challenging automotive environment, with revenue from operations rising 3.8% to ₹1,091.8 Cr from ₹1,051.8 Cr in FY24, taking total income to ₹1,100.2 Cr versus ₹1,060.1 Cr last year. Profitability improved as operating leverage supported margins, with EBITDA at ₹175.1 Cr (16.0% margin) against ₹159.4 Cr (15.2% margin) in FY24, while Profit Before Tax (PBT) increased 12.5% to ₹130.4 Cr from ₹115.9 Cr and Net Profit (PAT) grew 13.2% to ₹97.2 Cr from ₹85.9 Cr, leading to EPS rising to ₹7.6 from ₹6.7.

Operational Metrics (FY25 vs FY24): Cost of materials consumed rose marginally to ₹576.0 Cr from ₹571.2 Cr, while employee expenses increased to ₹143.0 Cr vs ₹138.9 Cr and other expenses grew to ₹210.0 Cr from ₹197.2 Cr; finance costs remained low at ₹2.5 Cr vs ₹2.3 Cr and depreciation was stable at ₹42.2 Cr vs ₹41.3 Cr. Profitability metrics strengthened with net margin improving to 8.9% from 8.2%, return on equity rising to 0.31x from 0.29x, and current ratio improving to 1.17x from 1.05x. The balance sheet remains conservative with equity at ₹320.0 Cr vs ₹287.8 Cr, zero debt, and cash & cash equivalents at ₹65.7 Cr vs ₹110.5 Cr in FY24, reflecting dividend payout.

Strategic Developments: The Board declared an interim dividend of ₹50/share (FV ₹10), amounting to ₹63.9 Cr, treated as final for FY25. The company’s plants at Faridabad, Dharuhera, Pune, Oragadam, and Kadi secured multiple OEM audits with top ratings and also won quality & safety awards. Export revenue remained stable at ₹53.5 Cr vs ₹54.8 Cr in FY24, with foreign currency inflows of ₹54.0 Cr. Strategic focus areas during the year included cost rationalization, localization, green energy initiatives, and ramp-up of new business wins.

Date: Tue 09 Sep, 2025

Notice is hereby given that the 14th Annual General Meeting (AGM) of Oravel Stays Ltd. (OYO) will be held on Friday, September 26, 2025, at 5:30 PM (IST) through Video Conferencing (“VC”) or Other Audio-Visual Means (“OAVM”), to, inter alia, consider and transact the businesses set out below:

Ordinary Resolution

- To receive, consider, and adopt:

- The audited standalone financial statements of the Company for FY25, along with the Auditors’ Report and the Board’s Report thereon;

- The audited consolidated financial statements of the Company for FY25, together with the Auditors’ Report thereon.

- To consider the re-appointment of Mr. Aditya Ghosh (DIN: 01243445), Non-Executive Director, who retires by rotation and, being eligible, has offered himself for re-appointment.

- To appoint M/s. Walker Chandiok & Co LLP, Chartered Accountants (Firm Registration No. 001076N/N500013), as the Statutory Auditors of the Company and to authorize the Board of Directors to fix their remuneration.

Special Resolution

- To approve the issuance of fully paid-up bonus equity shares of face value Rs. 1/- each, in the ratio of 1:1 (i.e., one new equity share for every one existing equity share held), to the eligible shareholders whose names appear in the Register of Members/beneficial owners’ records of the Company as on Tuesday, September 30, 2025 (“Record Date”).

- To consider and approve the alteration and increase of the authorized share capital of the Company from Rs. 16,31,13,59,300/- to Rs. 24,31,13,59,300/-, consequent to the increase in the equity share capital of the Company.

- To approve and consider the increase in the Employee Stock Option (ESOP) Pool of the Company by granting an additional 8,80,00,000 stock options under the existing Employee Stock Option Plan-2018 (“ESOP Plan”) of the Company.

The remote e-voting facility shall commence on Monday, September 22, 2025 at 9:00 AM (IST) and remain open until Thursday, September 25, 2025 at 5:00 PM (IST).

Date: Tue 09 Sep, 2025

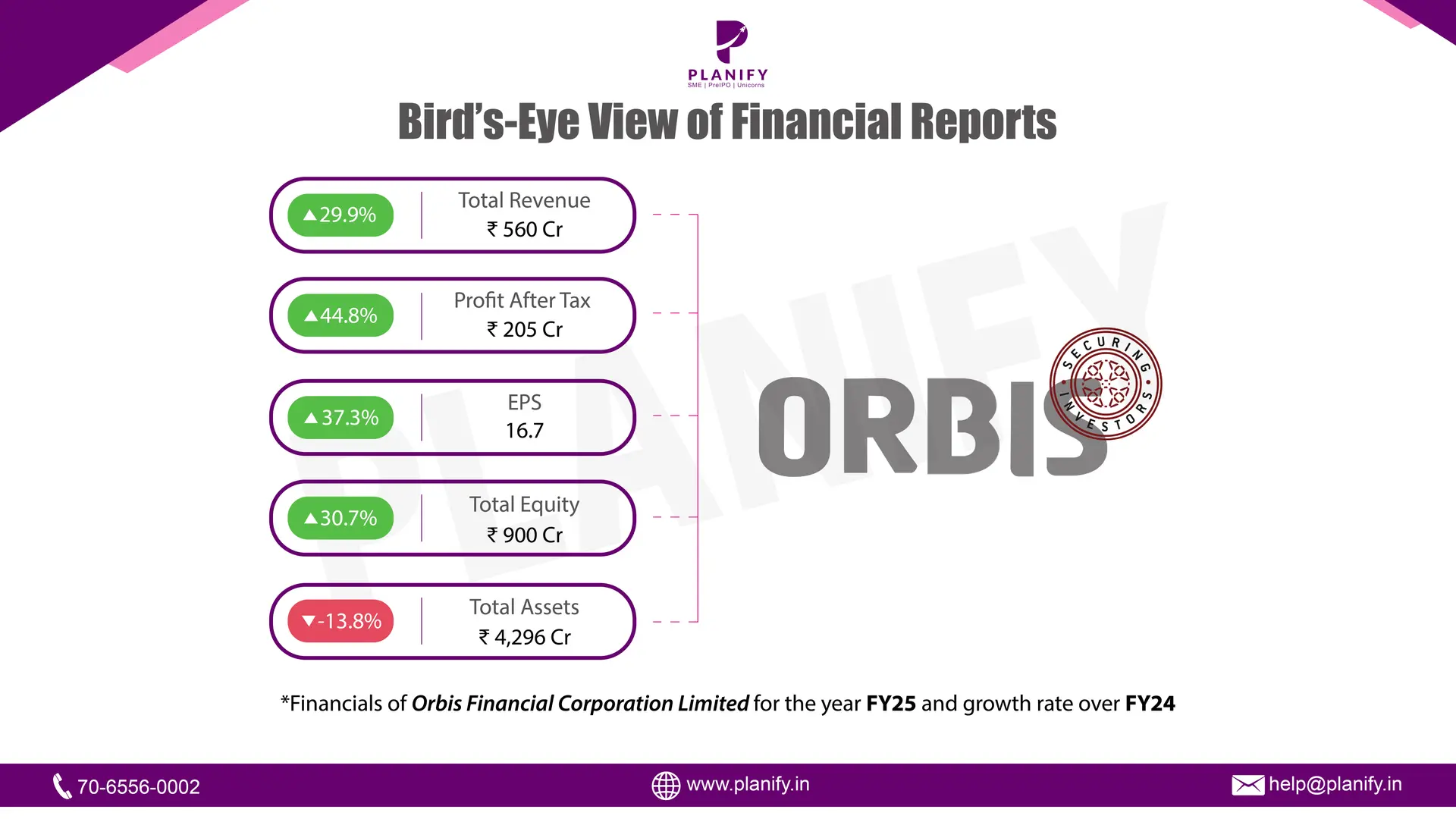

- Financial Performance (FY25 vs FY24): Orbis Financial Corporation delivered a strong performance in FY25. Total income rose 29.9% to ₹560 Cr, compared with ₹431 Cr in FY24. This was led by higher revenue from operations across custodial, clearing, and fund accounting services. Profit Before Tax (PBT) increased 46.9%, reaching ₹275 Cr, versus ₹187 Cr last year. Net Profit (PAT) grew 44.8% to ₹205 Cr from ₹141 Cr. Earnings per share (EPS) also improved strongly, with basic EPS at ₹16.7 (vs ₹12.2 in FY24) and diluted EPS at ₹15.7 (vs ₹11.3), reflecting healthy earnings momentum.

- Operational Metrics (FY25 vs FY24): Despite the higher base, profitability strengthened. Operating profit (EBITDA) stood at ₹379 Cr, up 48.3% from ₹256 Cr in FY24. The EBITDA margin expanded to ~68% from ~59%, indicating strong cost efficiency. Net profit margin also improved to 36.5% in FY25 versus 32.8% in FY24, reflecting better leverage of fixed costs and disciplined expense management. Finance costs rose to ₹99 Cr (from ₹65 Cr) due to higher working capital needs, but were well covered by operating profits. Net worth rose to ₹900 Cr from ₹688 Cr, supported by strong profit accretion and equity issuances, while the debt-to-equity ratio improved to ~3.8x from ~6.2x, reflecting lower reliance on borrowings. Cash and bank balances stood at ₹3,984 Cr, providing ample liquidity for growth.

- Strategic Developments: Orbis Financial Corporation delivered robust double-digit growth across revenue, profits, and EPS in FY25, with margin expansion and stronger balance sheet metrics. On the business front, the company consolidated its group structure under Orbis Trusteeship Services Pvt. Ltd. and Orbis Financial Services (IFSC) Pvt. Ltd., with the latter progressing towards securing a final Finance Company license from IFSCA, opening up new avenues in GIFT City. To strengthen human capital, Orbis granted 15.1 lakh ESOPs and allotted ~25 lakh equity shares under stock option plans, while also enhancing shareholder returns with a higher dividend of ₹1.80 per share in FY25 (vs ₹1.00 in FY24).

Date: Tue 09 Sep, 2025

Notice of the 19th Annual General Meeting ("AGM") of Orbis Financial Corporation Limited, which is scheduled for Tuesday, September 30, 2025, at 03:00 p.m. (IST) at OASIS, AIR By Ahuja Residences, 25, J-10, DLF Phase 2, Sector 25, Gurugram, Sarhol, Haryana 122002 in physical mode to transact the following businesses:

Ordinary Business:

- To consider and adopt the Audited Standalone Financial Statements for the year ended March 31, 2025 and the reports of the Board of Directors and Auditors thereon.

- To consider and adopt the Audited Consolidated Financial Statements for the year ended March 31, 2025 and the report of the Auditors thereon.

- To declare a final dividend at the rate of 18 % i.e Rs. 1.80 per equity share on face value of Rs. 10/- each for the financial year ended March 31, 2025.

- To appoint a director in place of Mr. Rup Chand Jain (DIN: 00092600), who retires by rotation, and being eligible, has offered himself for re-appointment.

- Appointment of Mr. Om Prakash Dani (DIN: 00180703) as Independent Director

Special Business:

- Re-appointment and Remuneration of Mr. Shyamsunder Basudeo Agarwal (DIN: 08516709) as Managing Director (designated as Managing Director and Chief Executive Officer) of the Company.

- To approve conversion of loan (credit facilities) from HDFC Bank Limited, State Bank of India, AU Small Finance Bank Limited in specific and other Banks, NBFC, Financial Institutions and Body Corporates, etc. in general, into equity shares of the Company pursuant to Section 62 (3) of The Companies Act, 2013 for borrowings availed/to be availed, as the case may be, including by way of Ratification

Instructions at glance

Cut-off date | Tuesday, September 23, 2025 |

Commencement of remote e-voting | Thursday, September 25, 2025 at 09:00 a.m. (IST) |

End of remote e-voting | Monday, September 29, 2025 at 05:00 p.m. (IST). |

AGM | Tuesday, September 30, 2025 at 03:00 p.m. (IST) |

Date: Tue 09 Sep, 2025

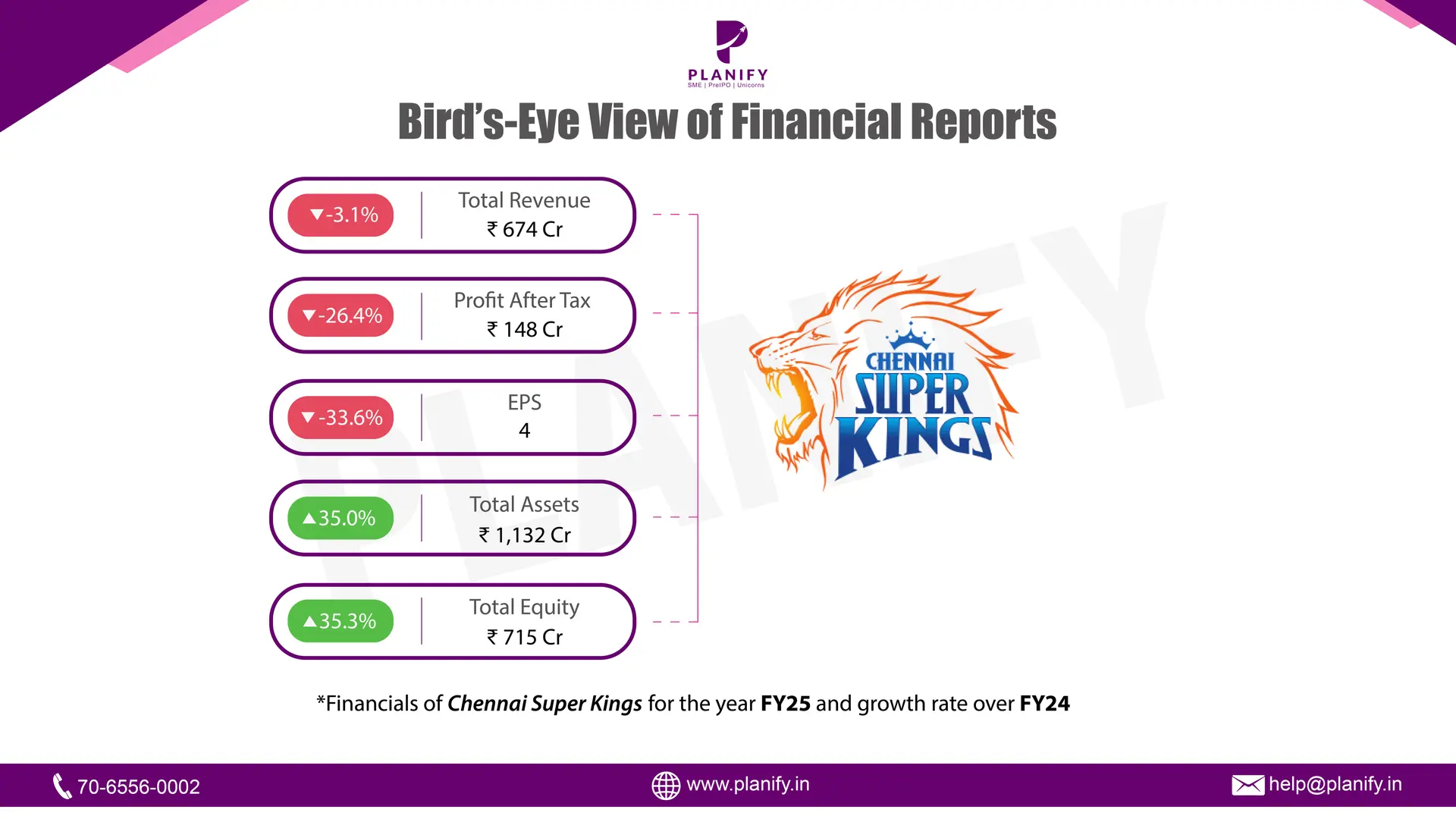

Financial Performance (FY25 vs FY24): Chennai Super Kings Cricket Limited (CSKCL) reported a softer FY25 versus FY24, mainly due to the absence of prize money that had boosted the previous year, with standalone revenue declining 4.8% to ₹644.0 Cr from ₹676.4 Cr. Profitability came under pressure as PBT contracted 20.7% to ₹243.0 Cr from ₹306.7 Cr and Net Profit (PAT) fell 21.0% to ₹180.9 Cr from ₹229.1 Cr, while EPS moderated to ₹4.8 (basic) from ₹7.0 and ₹4.8 (diluted) from ₹6.1. Despite these declines, CSKCL remained profitable, supported by cost controls and strong sponsorships. On a consolidated basis, the group posted Net Profit of ₹151.5 Cr in FY25 vs ₹201.5 Cr in FY24, reflecting similar pressures across global franchises.

Operational Metrics (FY25 vs FY24): Operating expenses rose as cost of operations increased to ₹372.0 Cr from ₹349.2 Cr, driven by franchise fees and higher player remuneration, while employee benefit costs nearly doubled to ₹12.1 Cr from ₹6.2 Cr on account of managerial remuneration and commissions. On the other hand, finance costs fell sharply to ₹1.5 Cr from ₹7.2 Cr due to deleveraging, though depreciation rose to ₹7.6 Cr from ₹2.8 Cr reflecting asset investments. Profitability softened with net margins contracting to 28.1% in FY25 from 33.9% in FY24 and operating margins moderating on higher costs. However, balance sheet strength improved as total assets expanded to ₹1,175.1 Cr from ₹900.1 Cr, supported by higher reserves, with cash & cash equivalents more than doubling to ₹336.4 Cr, significantly enhancing liquidity.

Strategic Developments: Subsidiaries continued to expand their global footprint, with Superking Ventures Pvt Ltd (India) posting revenue of ₹18.1 Cr (vs ₹5.5 Cr in FY24) and PAT of ₹5.5 Cr (vs ₹1.6 Cr loss), driven by strong growth at Super Kings Academy. Joburg Super Kings (South Africa) saw revenue rise to ₹45.3 Cr (vs ₹40.2 Cr) though losses widened to ₹32.8 Cr (vs ₹26.2 Cr) on higher player costs. Super Kings International Inc (USA) reported PAT of ₹1.8 Cr on ₹2.5 Cr revenue, and also acquired 55.5% in Texas Super Kings LLC, which generated ₹3.6 Cr revenue but incurred a ₹7.1 Cr loss in its debut season. The company recommended a dividend of ₹1 per equity share (FV ₹0.10) for FY25, while continuing to prioritize investments in sports academies, global league participation, and cricket ecosystem expansion as part of its growth strategy.

Date: Mon 08 Sep, 2025

Groww, one of India’s fastest-growing fintech platforms, has received approval from SEBI to launch its highly anticipated $1 billion IPO. The public issue is expected to value the Bengaluru-based startup between $7–8 billion, making it one of the most significant fintech listings in India’s market history.

Founded in 2016 by Lalit Keshre, Harsh Jain, Neeraj Singh, and Ishan Bansal, Groww has quickly transformed from a mutual fund investment platform into a full-scale brokerage, becoming the largest stockbroker in India by over 13 million active users.

- Financially, Groww’s momentum has been remarkable. In FY25, the company reported a net profit of ₹1,819 crore,a threefold increase compared to FY24 operational profitability marked as ₹535 crore. Revenue also surged to ₹4,056 crore in FY25, compared to ₹3,145 crore in FY24, reflecting its strong customer base, improved monetisation strategy, and operational efficiency.

- However, In FY24 the bottom line was impacted by a one-time tax outgo of ₹1,340 crore related to the reverse flip of its holding entity from the United States to India, resulting in a reported net loss of ₹805 crore.

Now, Groww is preparing for its biggest leap yet: a $1 billion IPO. With SEBI’s approval in hand, the company is looking at a valuation of $7–8 billion, setting the stage for one of the largest fintech listings in India.

The issue is expected to comprise a mix of fresh shares (to raise new capital) and an offer-for-sale (OFS) from early backers. Among its marquee investors are Tiger Global, Peak XV Partners (formerly Sequoia Capital India), Ribbit Capital, Y Combinator, and ICONIQ Growth.

The IPO proceeds are expected to be channelled into strengthening technology infrastructure, expanding product offerings, and supporting inorganic growth initiatives, including acquisitions like Fisdom, a wealth-tech startup Groww recently acquired in an all-cash deal worth $150 million.

Date: Mon 08 Sep, 2025

The Securities and Exchange Board of India (SEBI) has approved Pace Digitek Limited's Draft Red Herring Prospectus (DRHP), paving the way for the company to launch its Initial Public Offering (IPO). This approval was granted through an observation letter dated August 29, 2025, following the company's DRHP filing on March 27, 2025.

Pace Digitek Limited, headquartered in Bengaluru, is a multidisciplinary solutions provider specialising in the telecom passive infrastructure sector, including telecom tower infrastructure and optical fibre cables.

The company, incorporated in 2007 by Venugopal Rao Maddisetty, has evolved from manufacturing passive electrical equipment to offering comprehensive turnkey solutions across India, Myanmar, and Africa.

Financial Snapshot

The company's revenue from operations surged by 383.81%, increasing from ₹503 crore in FY23 to ₹2,434 crore in FY24. Profit after tax (PAT) also experienced remarkable growth of 1,290.38%, rising from ₹16.53 crore in FY23 to ₹229 crore in FY24. On a consolidated basis, revenue stood at ₹2,438 crore in FY25, almost flat compared to ₹2,434 crore in FY24. However, the profits tell a different story. Consolidated profit increased to ₹279 crore in FY25 from ₹229 crore in FY24, marking a healthy 21% year-on-year growth.

Unlisted share price of Pace Digitek currently trades at around ₹230, implying a P/E multiple of ~14.4x based on FY25 EPS of ₹16. Based on its expected ~₹4,104 crore IPO valuation, the company would be priced at about 15x earnings and ~2x sales.

Pace Digetek IPO Details

- The proposed issue is a pure fresh issue of up to ₹900 crore. The DRHP also enables a pre-IPO placement of up to ₹180 crore; if that’s executed, the fresh issue size will be trimmed accordingly.

- Proceeds are earmarked primarily for capex of ₹630 crore notably to invest in subsidiary Pace Renewable Energies and to set up Battery Energy Storage Systems (BESS) for an MSEDCL-awarded project plus general corporate purposes. Unistone Capital is the sole BRLM and MUFG Intime the registrar.

The industry backdrop also favors Pace Digitek. Data consumption in India is growing at one of the fastest rates in the world, and telecom companies are aggressively expanding fiber and 5G coverage. Government policies like the National Broadband Mission are also pushing for deeper connectivity across urban and rural areas.

Date: Mon 08 Sep, 2025

This could be the biggest listing.

At Reliance Industries’ 48th Annual General Meeting (AGM) held on August 29, 2025, Chairman Mukesh Ambani has unveiled plans to list Jio Platforms in the first half of 2026, describing it as a "very attractive opportunity" for investors. The telecom giant, now serving over 500 million subscribers, continues to expand aggressively into digital services, AI infrastructure, and global partnerships.

- Key priorities include universal connectivity, household digital services, business digitisation, and an "AI Everywhere for Everyone" vision.

- The listing is central to Jio’s AI-first vision, as it introduces its new subsidiary, Reliance Intelligence, and strategic partnerships with Meta and Google to build AI-powered infrastructure and services.

Yet, analysts caution that existing RIL shareholders won’t directly benefit since proceeds will flow into Jio Platforms for expansion, not into dividends or buybacks. Still, the IPO could significantly unlock enterprise value and align India’s telecom leader with its digital and AI ambitions.

This IPO comes with high expectations: analysts estimate a valuation ranging from $111 billion to $154 billion, potentially making it India’s biggest-ever IPO. While this promises significant value creation, especially for pre-IPO global backers such as Google, Meta, and KKR, concerns linger over execution risks, holding company valuation discounts, and missed opportunities from not pursuing a standalone demerger. Jio’s upcoming listing not only tests market appetite for mega IPOs, but also signals a pivotal moment where telecom scale converges with AI-driven ambition in public markets.

Stay Connected, Stay Informed –

Don’t miss out on exclusive updates, market trends, and real-time investment opportunities. Be the first to know about the latest unlisted stocks, IPO announcements, and curated Fact Sheets, delivered straight to your WhatsApp.