Planify Feed

Date: Fri 05 Sep, 2025

Notice of the 19th Annual General Meeting ("AGM") of Fino PayTech Limited, which is scheduled for Monday, September 29, 2025 at 02:15 p.m. (IST) through video conferencing (“VC”)/ other audio-visual means (“OAVM”) to transact the following businesses:

Ordinary Business:

- To receive, consider and adopt the Standalone and Consolidated Audited Financial Statements as per Ind-AS for the Financial Year ended March 31, 2025, together with the Reports of the Board of Directors and Auditors thereon.

- To appoint a Director in place of Mr. Amit Kumar Jain (DIN: 08353693), who retires by rotation and being eligible, offers himself for re-appointment.

Special Business:

- To approve the payment of remuneration to Mr. Amit Kumar Jain (DIN: 08353693), Whole-time Director and Key Managerial Personnel of the Company for the Financial Year 2025-26.

Instructions at glance

Cut-off date | Monday, September 22, 2025 |

Commencement of remote e-voting | Thursday, September 25, 2025 at 09:00 a.m. (IST) |

End of remote e-voting | Sunday, September 28, 2025 at 05:00 p.m. (IST). |

AGM | Monday, September 29, 2025 at 02:15 p.m. (IST) |

Date: Fri 05 Sep, 2025

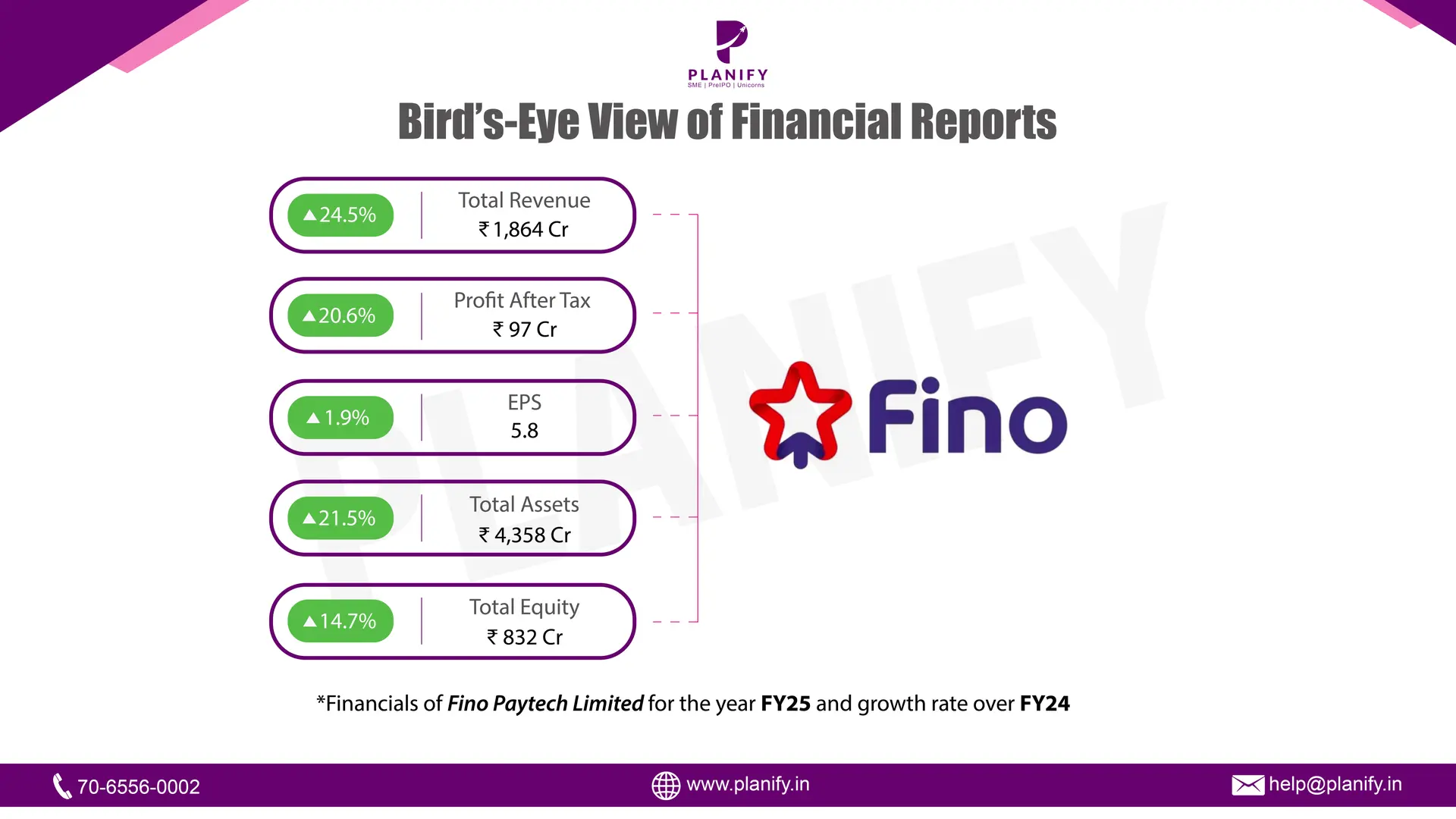

- Financial Performance (FY25 vs FY24): Despite a weaker FY24, the company delivered solid growth on a consolidated level while also turning profitable on a standalone basis in FY25. On a consolidated basis, total income grew by 24.5%, reaching ₹1,864 Cr in FY25 versus ₹1,497 Cr in FY24. Profit Before Tax (PBT) rose 44.0%, to ₹115 Cr from ₹80 Cr. Net Profit (PAT) stood at ₹97 Cr, up 20.6% from ₹81 Cr. EPS improved to ₹5.8 (basic) from ₹5.7, and to ₹5.7 (diluted) from ₹4.6, showing stable earnings momentum despite a marginal increase in equity base. On a standalone basis, the company posted a small revenue decline, with total income at ₹19.4 Cr, down 3.8% from ₹20.2 Cr in FY24. However, PBT turned positive at ₹4.2 Cr, compared to a ₹8.4 Cr loss last year. PAT also improved to ₹3.1 Cr, against a ₹7.2 Cr loss in FY24, reflecting cost control. EPS recovered to ₹0.29 from -₹0.69, highlighting a turnaround at the entity level.

- Operational Metrics (FY25 vs FY24): Consolidated net profit margin came in at 5.2% (vs 5.4% in FY24), a marginal dip due to higher employee and finance costs. Operating profit margin improved slightly to 15.7% from 15.3%, showing efficiency gains at scale. Standalone margins improved meaningfully, with net margin at 16% in FY25 compared to a negative margin last year. This was driven by a sharp reduction in other expenses (₹4 Cr vs ₹16 Cr in FY24). The consolidated balance sheet remains strong, with total assets at ~₹4,359 Cr

- Strategic Developments: Subsidiary Fino Payments Bank was the main growth engine, delivering ₹18,471 Cr revenue and ₹925 Cr PAT in FY25. Smaller subsidiaries such as Fino Trusteeship Services (₹0.4 Cr PAT) were profitable, while FFPL Finserv (₹0.6 Cr loss) and Fino Financial Services (₹0.01 Cr loss) had minimal impact. No dividend was declared for FY25, as the board chose to retain earnings despite strong consolidated profitability. The company issued 2,695 equity shares under ESOPs. Continued investments in financial inclusion and Aadhaar-based authentication services strengthened its ecosystem.

Date: Tue 02 Sep, 2025

The Securities and Exchange Board of India (SEBI) has approved the Draft Red Herring Prospectus (DRHP) of Pace Digitek Limited, paving the way for the company to launch its initial public offering (IPO). The company had filed its DRHP on March 27, 2025, and SEBI granted its approval through an observation letter dated August 29, 2025.

IPO Offer Size

Particulars | No. of Shares | Amount (₹ in crore) |

Fresh Issue | Up to [●] | 900.0 |

Offer for Sale (OFS) | Nil | Nil |

Total Issue Size | Up to [●] | 900.0 |

(The exact number of shares will be finalized closer to the IPO launch. The issue may also include a Pre-IPO placement of up to ₹180 crore, which will reduce the fresh issue size accordingly.)

Key Parties

- Book Running Lead Manager (BRLM): Unistone Capital Private Limited

- Registrar to the Issue: MUFG Intime India Private Limited (formerly Link Intime India Pvt. Ltd.)

Summary

With SEBI’s approval in hand, Pace Digitek can now proceed to file its Red Herring Prospectus (RHP) and announce the IPO opening dates. Investors should watch out for further details on the price band, lot size, and timeline once the RHP is filed.

Date: Tue 02 Sep, 2025

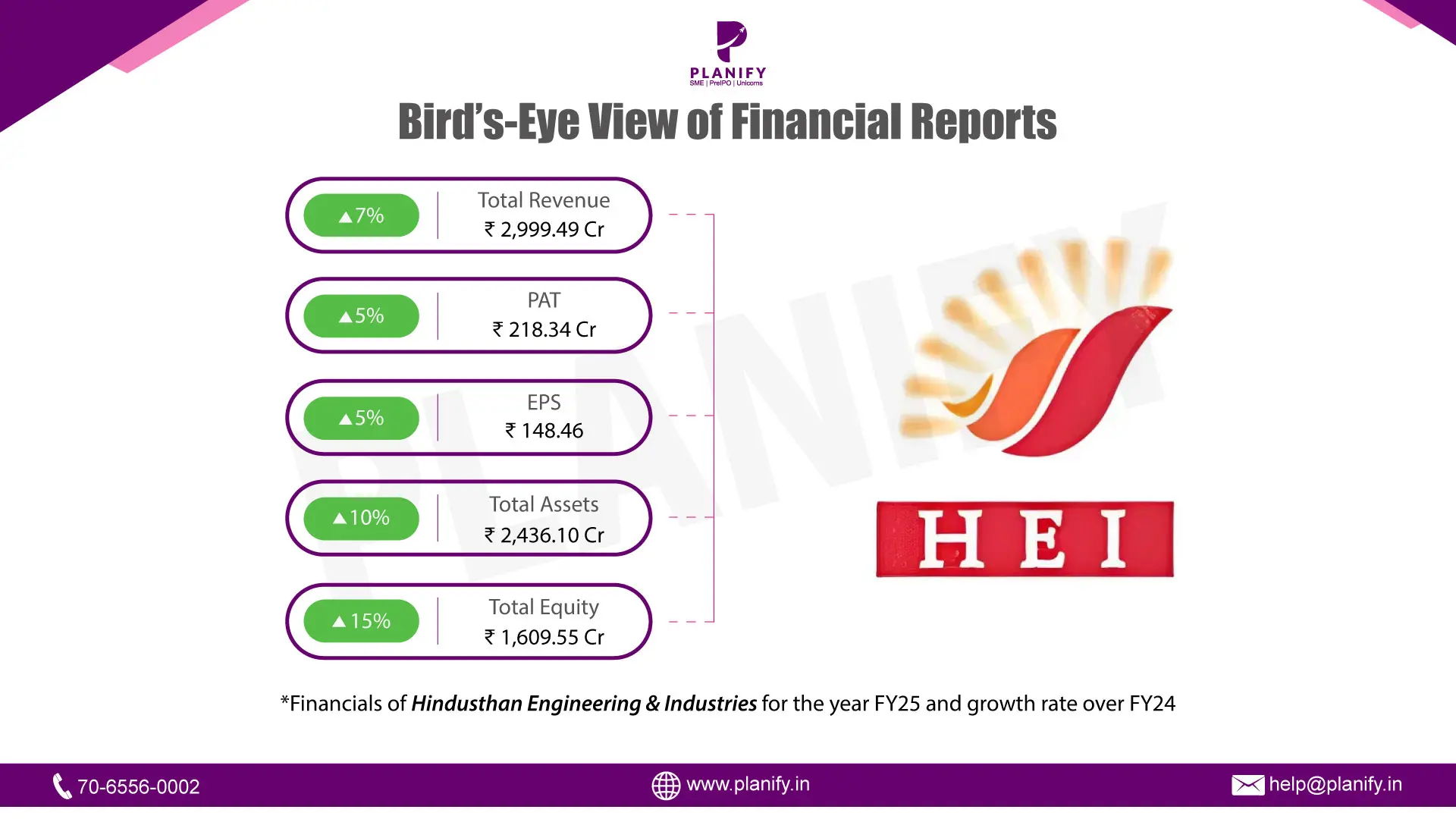

Hindusthan Engineering & Industries Limited delivered consistent financial performance in FY25, demonstrating stability in both revenue and profitability. Alongside moderate earnings growth, the company reinforced its balance sheet through stronger equity and asset expansion, positioning itself for sustainable long-term growth.

- Revenue: In FY25, the company recorded a total revenue of ₹2,999.49 crore, reflecting a 7% increase over FY24. This steady growth underlines the company’s ability to sustain top-line expansion in a competitive market environment.

- Net Profit and EPS: Profit After Tax (PAT) stood at ₹218.34 crore, showing a 5% rise year-on-year. Similarly, Earnings Per Share (EPS) increased by 5% to ₹148.46, highlighting that profitability gains translated directly into improved shareholder returns.

- Assets & Equity: On the balance sheet side, total assets reached ₹2,436.10 crore, up 10% from the previous year, indicating continued capacity building and investment. More significantly, total equity rose 15% to ₹1,609.55 crore, strengthening the company’s capital base and reinforcing financial resilience.

Hindusthan Engineering & Industries closed FY25 with stable revenue growth, improved profitability, and stronger equity. While growth rates were moderate compared to high-growth peers, the company’s steady performance and balance sheet reinforcement signal long-term stability, making it well-positioned to capture future opportunities.

Date: Tue 02 Sep, 2025

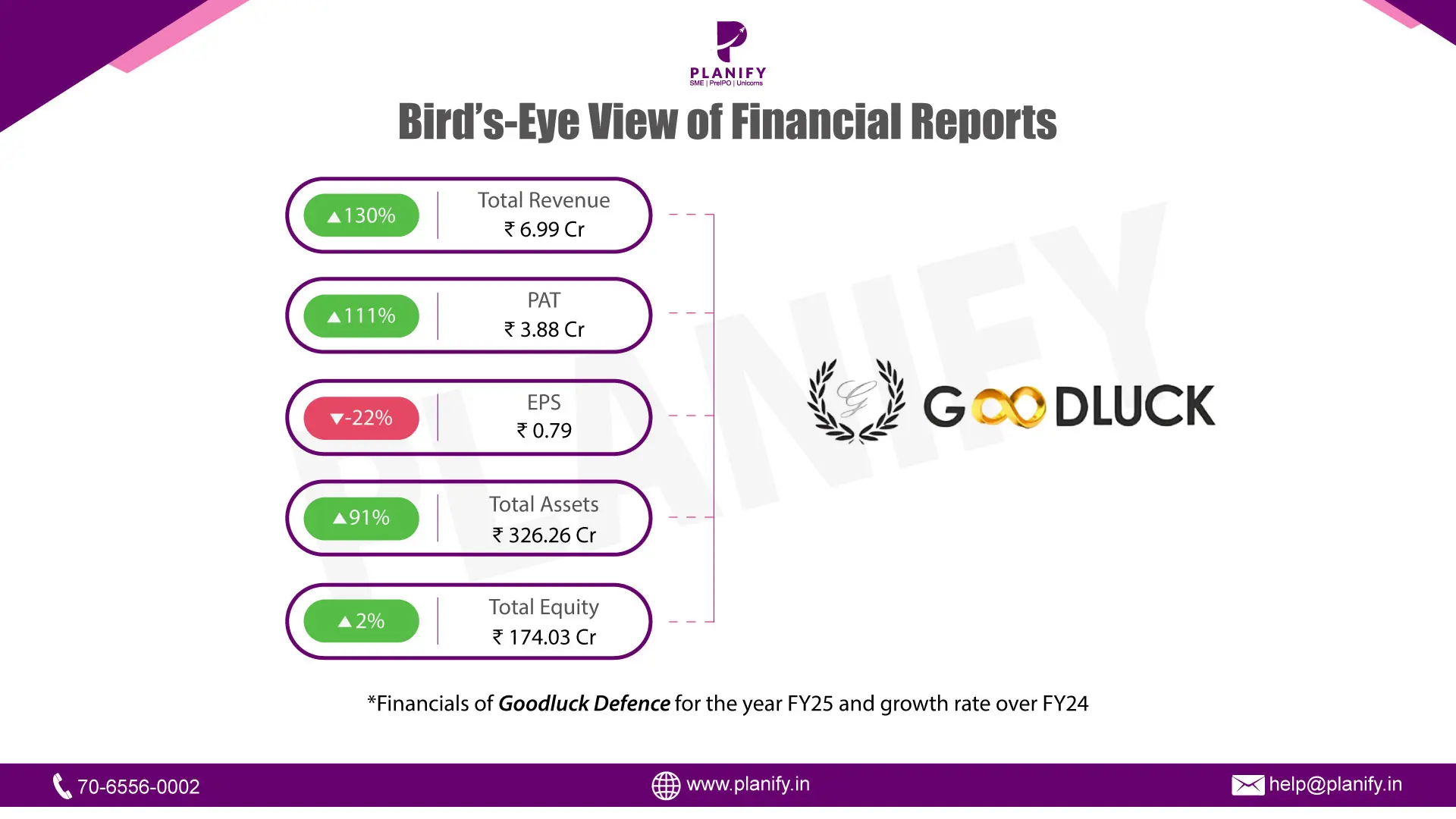

Goodluck Defence’s FY25 performance reflects exceptional revenue and profit growth, showcasing its operational strength and expanding scale.

- Revenue: In FY25, Goodluck Defence reported a total revenue of ₹6.99 crore, reflecting an impressive 130% year-on-year growth over FY24. This surge underscores the company’s robust top-line momentum, indicating that its operations and market presence have expanded significantly compared to the previous year.

- Profitability & EPS: The company’s profitability also saw a sharp improvement, with Profit After Tax (PAT) rising to ₹3.88 crore, a growth of 111% year-on-year. However, despite this robust bottom-line growth, the Earnings Per Share (EPS) declined by 22% to ₹0.79.

- Assets & Equity: On the balance sheet side, total assets increased substantially to ₹326.26 crore, marking a 91% rise over the previous year. In contrast, total equity grew modestly by just 2% to ₹174.03 crore. The sharp rise in assets compared to equity suggests that the company relied more heavily on borrowings or external liabilities to fund its expansion, indicating a higher leverage position.

- Goodluck Defence delivered outstanding revenue and profit growth in FY25, underscoring its strong operational performance and accelerating scale of operations. However, the decline in EPS and disproportionate asset-equity growth raises caution around shareholder returns and leverage. Sustaining profitability while balancing capital structure will be critical for driving long-term value.

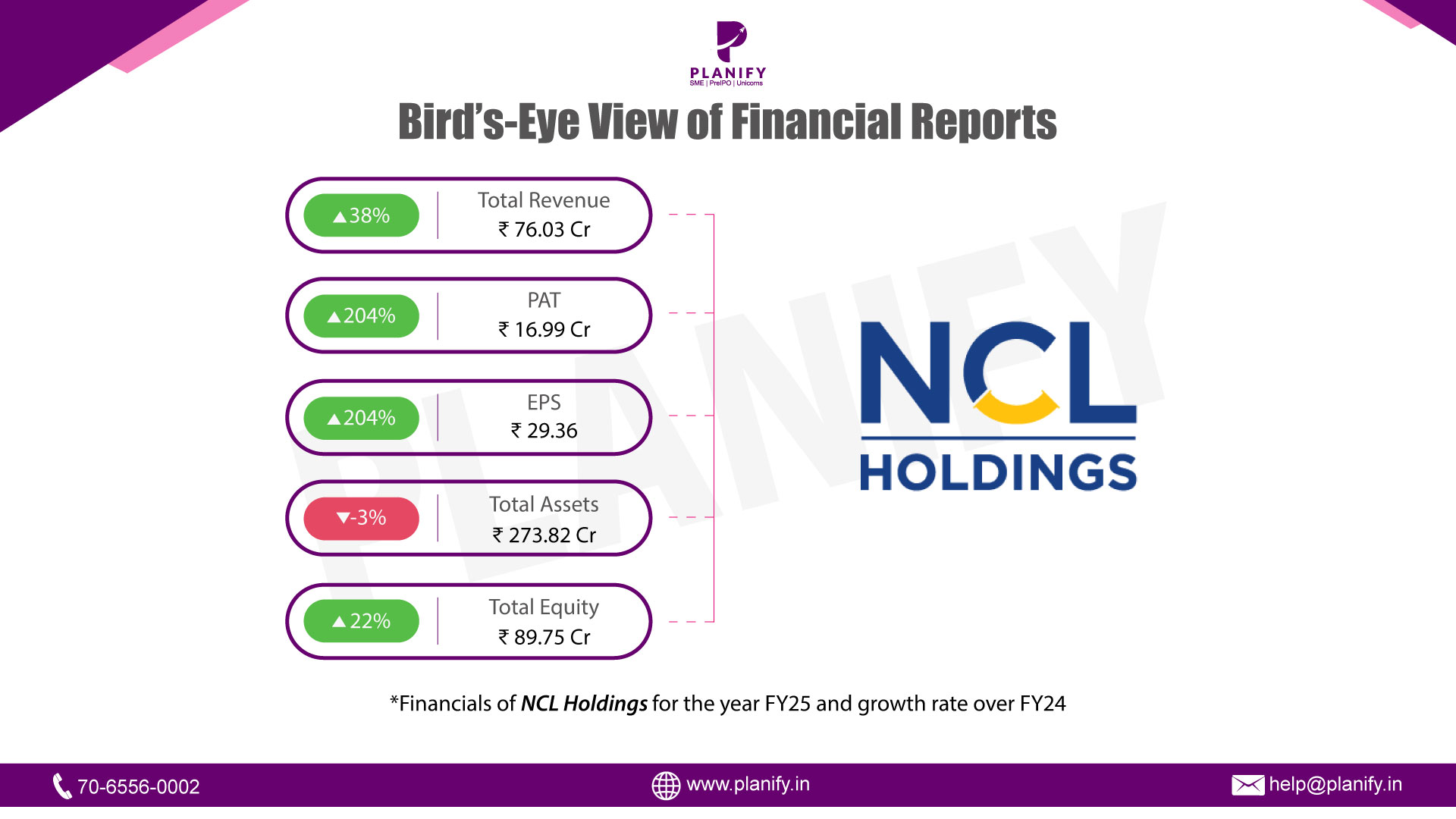

Date: Tue 02 Sep, 2025

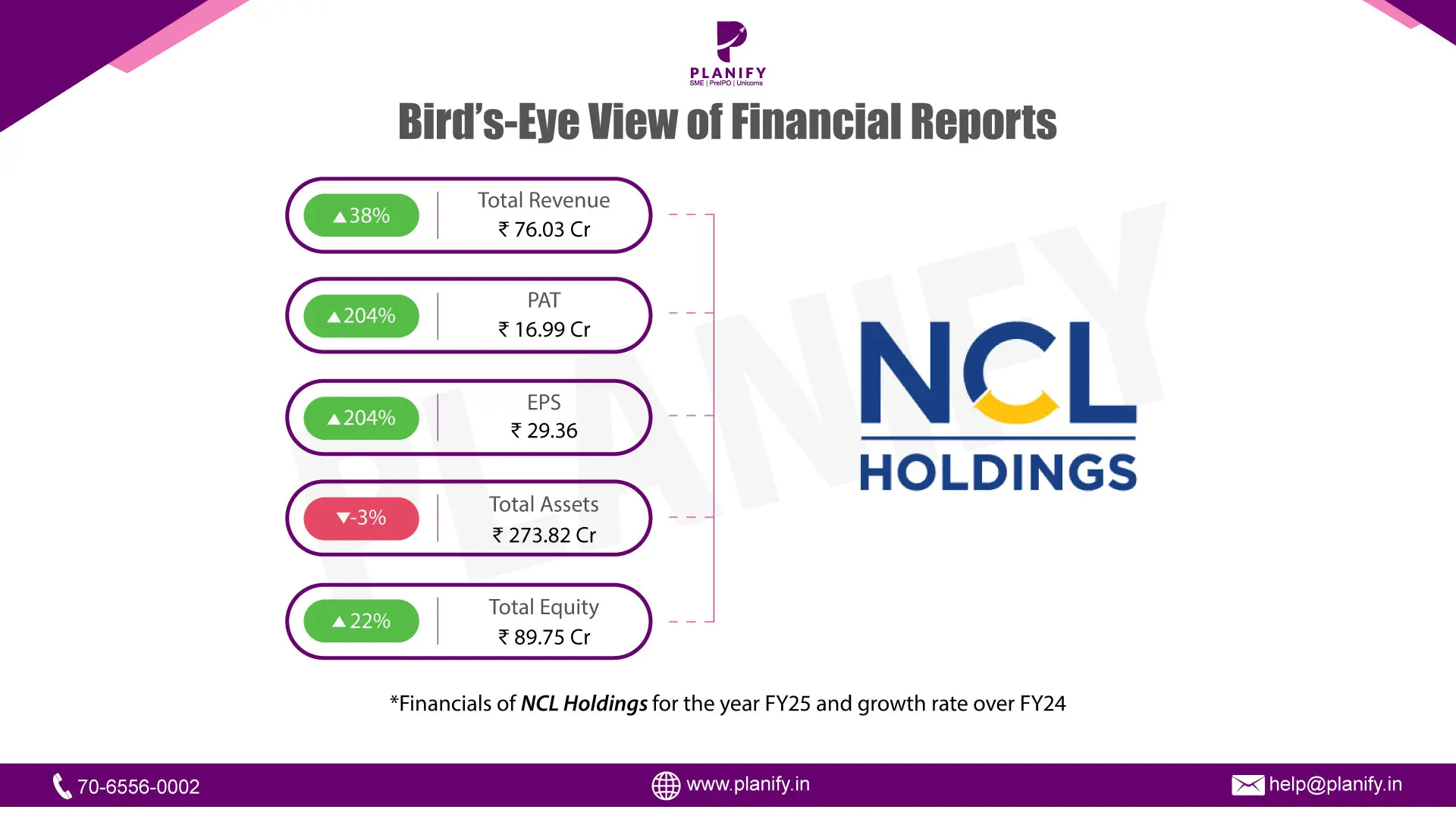

NCL Holdings Limited has delivered a solid performance in FY25, reflecting its ability to scale revenues while significantly boosting profitability. The company’s financials indicate strong operational efficiency, higher shareholder returns, and a stable capital structure, despite a marginal decline in assets.

- Revenue: In FY25, NCL Buildtek reported a total revenue of ₹76.03 crore, marking a 38% year-on-year growth over FY24. This healthy top-line expansion highlights the company’s ability to capture market opportunities and sustain momentum in its core business operations.

- Net Profit and EPS: Profitability witnessed a remarkable surge, with Profit After Tax (PAT) rising to ₹16.99 crore, representing a 204% increase year-on-year. This sharp improvement reflects stronger operational efficiency and cost management. In line with profit growth, Earnings Per Share (EPS) also rose 204%, reaching ₹29.36, underscoring enhanced returns for shareholders.

- Assets & Equity: On the balance sheet front, total assets stood at ₹273.82 crore, registering a marginal 3% decline compared to FY24. This indicates cautious asset utilization despite revenue and profit growth. Meanwhile, total equity increased by 22% to ₹89.75 crore, strengthening the company’s capital base and reflecting improved shareholder value.

NCL Holdings delivered an outstanding financial performance in FY25, with robust revenue growth and a sharp rise in profitability, translating into significantly higher EPS. Although total assets saw a minor dip, the improvement in equity signals financial resilience. Overall, the company is on a strong growth trajectory, balancing profitability with capital strength, which positions it well for future expansion.

{kind=link}

Date: Fri 29 Aug, 2025

Hero FinCorp Ltd (HFCL), the lending arm of Hero MotoCorp, is gearing up for an IPO. The total IPO size is now ₹3,408 crore, marking a reduction from the ₹3,668 crore planned earlier. Hero Fincorp IPO backed by Apollo Global, ChrysCapital and Apis Partners.

Ahead of the IPO, the company completed two pre-IPO placements that not only strengthened its balance sheet but also set the tone for its market valuation. On June 5, 2025, Hero FinCorp raised ₹260 crore by allotting 18.57 lakh shares to 12 investors at a price of ₹1,400 per share, translating to a valuation of nearly ₹25,014 crore. This round brought in marquee investors such as Shahi Exports and RVG Jatropha. This pre-IPO round led to a reduction of ₹260 crore in the fresh issue size of the IPO.

On July 11, 2025, a second round added ₹50 crore from Vattikuti Ventures. This was achieved by allotting 3.57 lakh shares at ₹1,400 per share. This second placement further reduced the fresh issue size by ₹50 crore, bringing the revised fresh issue size to ₹1,790 crore. With these two rounds, the company mobilised ₹310 crore out of its target of ₹420 crore through pre-IPO placements.

At ₹1,400 per share, Hero FinCorp is valued at a P/B multiple of ~2.98x, based on its FY25 book value of ₹452 per share. The company is currently valued at ~ ₹25,014 crore, reflecting investor confidence in its recalibrated strategy and long-term growth prospects.

In Q1 FY26, Hero FinCorp reported a net loss of ₹49.7 crore, reversing from a profit a year ago, despite modest revenue growth to ₹2,333 crore, as compared to Q1 FY25 revenue of ₹2,250 crore. The weakness stemmed from elevated impairment costs, which soared to ₹2,884 crore(FY25) from ₹1,205 crore(FY24) up by 67%, as the company grapples with stress in its unsecured loan book. Provisions rose by 5.3% YoY to ₹740 Cr, and Net NPA increased to 2.50% from 2.15%., forcing management to recalibrate its lending model.

To reassure investors, the company has paused fresh disbursements in unsecured lending and is pivoting toward secured products such as vehicle and SME loans. Management still guides for around 14% loan growth in FY26, highlighting confidence in its franchise strength and distribution network built around Hero MotoCorp dealerships.

Hero FinCorp's IPO strategy bolsters Tier-1 capital, strengthens its lending base, and taps the public markets at a more optimal valuation. The company is strategically shifting gears to strengthen its loan book.

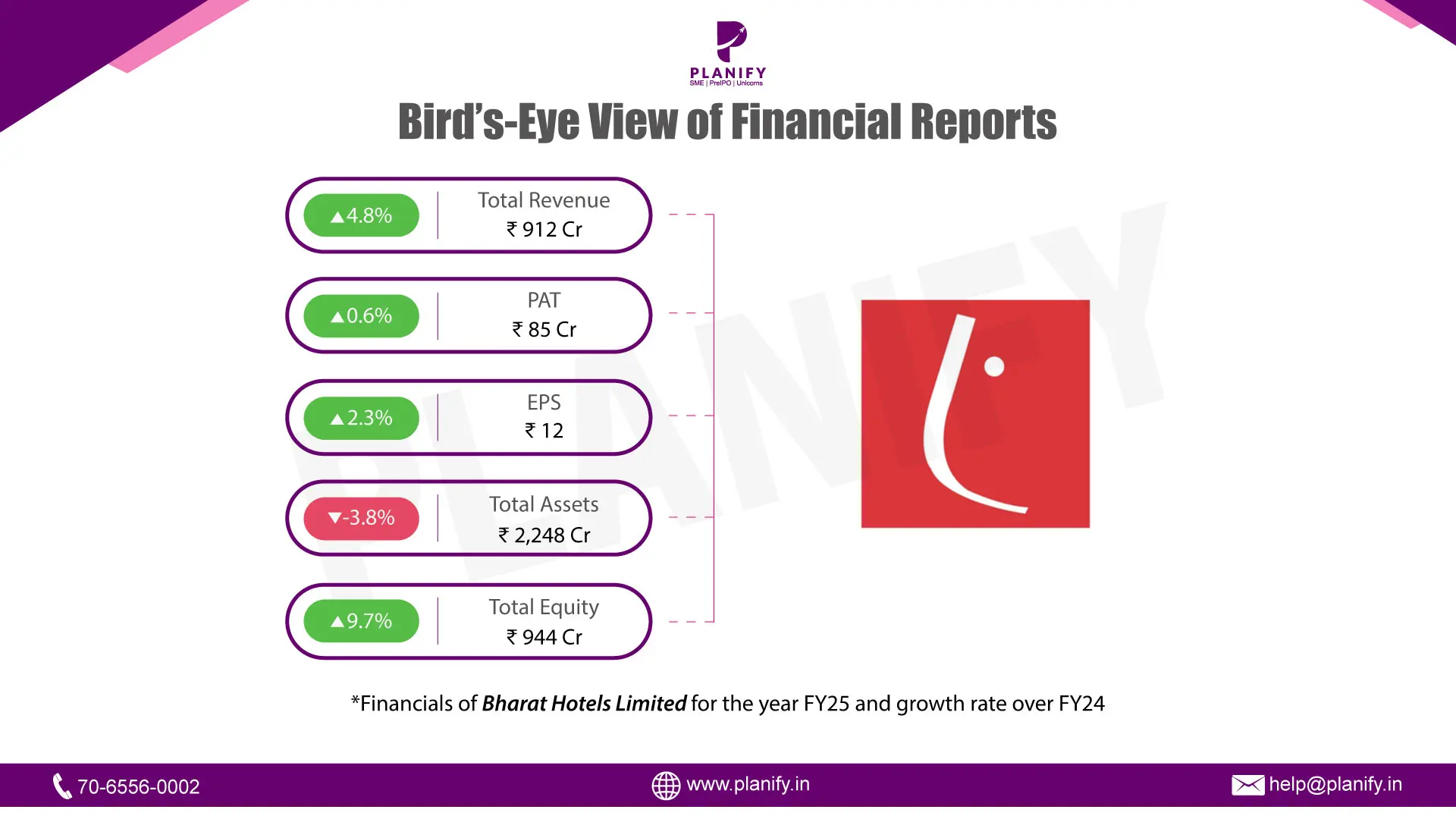

Date: Fri 29 Aug, 2025

- Revenue and Profitability – The company’s consolidated revenue grew by 4.8%, rising from ₹870.72 Cr in FY24 to ₹912.2 Cr in FY25, driven by higher occupancy, improved room rates, and stronger food & beverage sales. This supported a 5% increase in EBITDA, from ₹372 Cr in FY24 to ₹390 Cr in FY25, maintaining margins above 40%. However, higher depreciation and finance costs kept net profit growth moderate, with consolidated PAT at ₹85.3 Cr in FY25 versus ₹84.8 Cr in FY24, ensuring earnings stability.

- Financial Position – The company’s consolidated retained earnings grew sharply from ₹2,740.4 Cr in FY24 to ₹3,617 Cr in FY25, reflecting healthy cash generation. At the same time, deleveraging remained a focus: of the ₹1,100 Cr raised through NCDs in FY23, the outstanding liability reduced to ₹714 Cr by March 2025.

- Future Prospects – The management remains confident about sustained growth in the Indian hospitality industry, supported by strong domestic tourism, rising disposable incomes, and favourable government policies on infrastructure and travel promotion. With an EBITDA margin of over 40%, a focus on operational efficiency, and ongoing debt reduction, the company is well-positioned to capitalize on industry tailwinds. Expansion will be pursued selectively via refurbishments and asset-light management contracts, ensuring profitable growth while maintaining financial prudence.

Date: Tue 26 Aug, 2025

Vikram Solar’s IPO was a book-built issue worth ₹2,079.37 crore, consisting of a fresh issue of 4.52 crore shares (₹1,500.00 crore) and an offer for sale of 1.75 crore shares (₹579.37 crore).

IPO Timeline: Opened on August 19, 2025, closed on August 21, 2025, allotment finalized on August 22, 2025, and listing took place today, August 26, 2025, on the BSE and NSE.

Pricing: Price band of ₹315–₹332 per share; issue price at ₹332. Lot size was 45 shares, requiring a minimum retail investment of ₹14,175. For sNII, minimum investment stood at ₹2,09,160 (630 shares), and for bNII, ₹10,00,980 (3,015 shares).

Post-IPO P/E: 85.88.

Subscription Status

Anchor Investors: 1.00× (1,86,99,120 shares; ₹620.81 Cr)

QIB (Ex Anchor): 145.10× (₹60,052.72 Cr)

Non-Institutional Investors: 52.87× (₹16,412.45 Cr)

bNII: 59.58×

sNII: 39.46×

Retail Investors: 7.98× (₹5,780.37 Cr)

Employees: 5.10×

Overall Subscription:56.42× (₹82,296.51 Cr)

JM Financial Ltd. acted as book-running lead manager; MUFG Intime India Pvt. Ltd. served as registrar.

Neutral Market View

Our platform maintained a neutral rating, viewing Vikram Solar as a turnaround legacy play with potential, but with slower-than-expected performance. Unlisted market prices ranged between ₹180 and ₹485 in the past 18 months.

Legal Development – Fraud Case Filed

On August 26, 2025, the Matunga Police, following a court directive, registered a criminal case of fraud and criminal conspiracy against Vikram Solar (VSL) and Vikram Capital Management Pvt Ltd (VCMPL) along with 11 directors.

The complaint, filed by Nilang Navneet Shah, a director at Mumbai-based Seklink Technologies and Realty Pvt Ltd, alleges he was defrauded under the pretext of a solar module export deal to a US-based buyer, Kopia Power Devco.

Date: Tue 26 Aug, 2025

The Impending Regulation of India's Pre-IPO Grey Market

The murmurs from regulatory corridors have crystallised into a clear signal: the Securities and Exchange Board of India (SEBI) is set to bring the informal pre-IPO grey market under its watchful eye.

India’s capital markets may be on the brink of a structural shift. At a time when the IPO pipeline is booming with nearly ₹4.3 trillion raised in FY25 and another ₹1.4 trillion expected soon. SEBI chairperson Tuhin Kanta Pandey has hinted at the establishment of a regulated platform for pre-IPO share trading. The idea, floated at a recent capital markets conference, is to bring order and transparency to a space currently dominated by the grey market.

The timing of this move is crucial. India’s IPO market is expanding at record speed. In 2024 alone, 337 companies tapped the public markets, 91 on the mainboard and 241 on SME exchanges, raising nearly ₹1.67 lakh crore, with average listing gains of 29%. Yet, on the unlisted side, the scale is even larger. Estimates suggest more than 1,300 profitable unlisted companies together represent nearly ₹150 lakh crore of enterprise value waiting to be unlocked.

In order to bring pre-listing transactions into a structured ecosystem that allows accredited investors, early backers, and ESOP holders to access liquidity in a safe environment.

Currently, early-stage investors and employees often wait years for IPO exits, with ESOPs going underutilized. A regulated venue could change that, allowing accredited investors to buy and sell stakes ahead of listing, with proper settlement systems, tax compliance, and checks to avoid manipulation. It also ensures that the government captures its share of revenues, while companies benefit from cleaner valuation benchmarks.

This move signifies a pivotal shift towards greater transparency and investor protection in India's burgeoning capital markets.

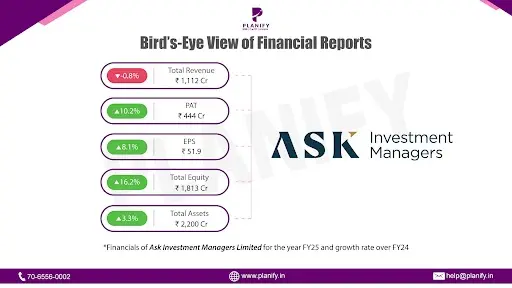

Date: Mon 25 Aug, 2025

- Financial Performance (FY25 vs FY24):ASK Investment Managers reported a mixed performance in FY25. Total income declined slightly by 0.8% to ₹1,112 Cr, compared to ₹1,121 Cr in FY24. This dip was mainly due to lower revenue from operations (₹1,038 Cr vs ₹1,063 Cr last year, down 2.2%), though other income rose 27.9% to ₹75 Cr. Profit Before Tax (PBT) fell by 16.7% YoY, from ₹515 Cr in FY24 to ₹429 Cr in FY25. However, due to lower tax outgo, Net Profit (PAT) improved 10.2% YoY, reaching ₹444 Cr versus ₹403 Cr in FY24. This reflects strong bottom-line resilience despite weaker top-line growth. On a per-share basis, EPS grew 8.1% YoY from Rs.48 per share in FY24 to Rs.52 per share in FY25.

- Operational Metrics (FY25 vs FY24): Margins showed some stress during the year. The operating margin declined as expenses grew faster than revenues – total expenses were up 12.8% YoY at ₹683 Cr vs ₹605 Cr in FY24. This was largely due to higher employee costs (+18.4%), finance costs (+87.3%), and depreciation (+59.6%), reflecting investments in expansion and digital infrastructure. For FY25, the net profit margin stood at ~40%, up from 36% in FY24, helped by a one-time tax adjustment reducing tax liability. However, operating efficiency weakened somewhat, and cost-to-income ratio increased, indicating pressure on operating leverage. On the balance sheet side, ASK strengthened its equity base – net worth rose to ₹1,8135 Cr in FY25 from ₹1,560 Cr in FY24 (+16.2%), while total liabilities declined to ₹386 Cr from ₹569 Cr. The debt-to-equity ratio improved sharply to 0.21x from 0.36x, showing strong financial discipline.

- Strategic Developments: In FY25, ASK Investment Managers focused on strengthening its business model and expanding its offerings. The company received SEBI’s in-principle approval to launch its own mutual fund, marking a significant milestone in diversifying its product portfolio. It also restructured subsidiaries by acquiring ASK Alternatives Managers Pvt. Ltd. and infused ₹250 Cr into ASK Wealth Advisors to support future growth. On the shareholder front, the company declared two interim dividends totaling around ₹222 Cr, reinforcing its commitment to returns. Employee alignment was strengthened through ESOPs and ESARs, while operations expanded with new offices across 27 locations, enhanced NRI platforms in Singapore and Dubai, and international AUM growth through its UCITS platform. These steps reflect ASK’s strategy of scaling up while maintaining strong financial discipline. However, tracking revenue momentum and margin stability will be crucial, as expense growth is outpacing top-line growth.

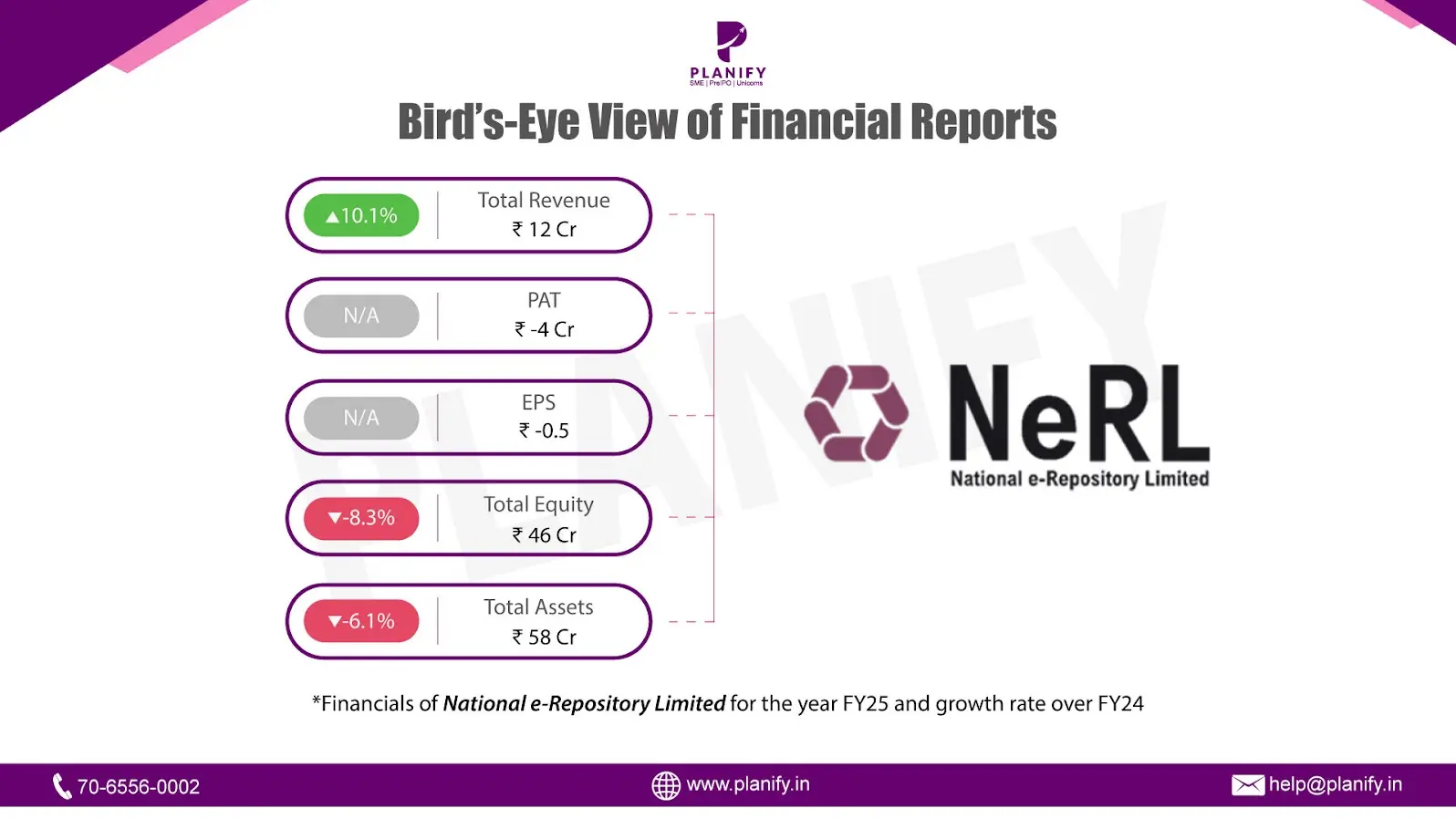

Date: Mon 25 Aug, 2025

- Financial Performance (FY25 vs FY24):NERL delivered steady top-line growth in FY25, though it remains loss-making. Total income for the year grew 10.1%, reaching ₹12 Cr from ₹11 Cr in FY24. This was driven by a 12.5% rise in revenue from operations to ₹9.7 Cr (vs. ₹8.6 Cr) and stable other income of ₹2.4 Cr (vs. ₹2.3 Cr). Profit Before Tax (PBT) stood at a loss of ₹5 Cr, compared with a loss of ₹7 Cr last year – an improvement of 21.0% YoY. Net Loss (PAT) narrowed to ₹4 Cr, compared with ₹5 Cr in FY24, a 20.6% improvement. Earnings per share (EPS) improved from -₹0.62 in FY24 to -₹0.49 in FY25.

- Operational Metrics (FY25 vs FY24): NERL’s operational metrics showed strong growth, led by Emerging Businesses. eNWR quantity grew 40.0% YoY to 138.4 Lakh MT from 98.9 Lakh MT. Value of eNWRs rose 16.7% YoY to ₹66,663 Cr, supported by higher adoption. Loans against eNWRs increased 9.3% YoY to ₹3,293 Cr. Client adoption strengthened, with active depositor/client accounts growing 18.4% YoY to 11,821. On the financial side, the balance sheet remained debt-free, with total assets at ₹58 Cr and equity at ₹46 Cr. Cash balances declined to ₹1 Cr from ₹2 Cr, but liquidity remains healthy. Investments in technology and infrastructure continued, with IT expenses up 25.6% YoY, reflecting its commitment to long-term scalability.

- Strategic Developments: In FY25, NERL continued its shift towards Emerging Businesses, which now contribute ~76% of eNWR value compared with 66% in FY24. The company expanded its pledgee participants (84 in FY25 vs. 76 in FY24) and grew active accounts base, reinforcing its ecosystem. However, since the company continues to be loss-making despite revenue growth, tracking its ability to scale operations profitably and control rising costs will be crucial. Sustained adoption of eNWRs, stronger traction in financing, and cost efficiency will determine how quickly NERL can move towards profitability in the coming years.

Date: Sat 23 Aug, 2025

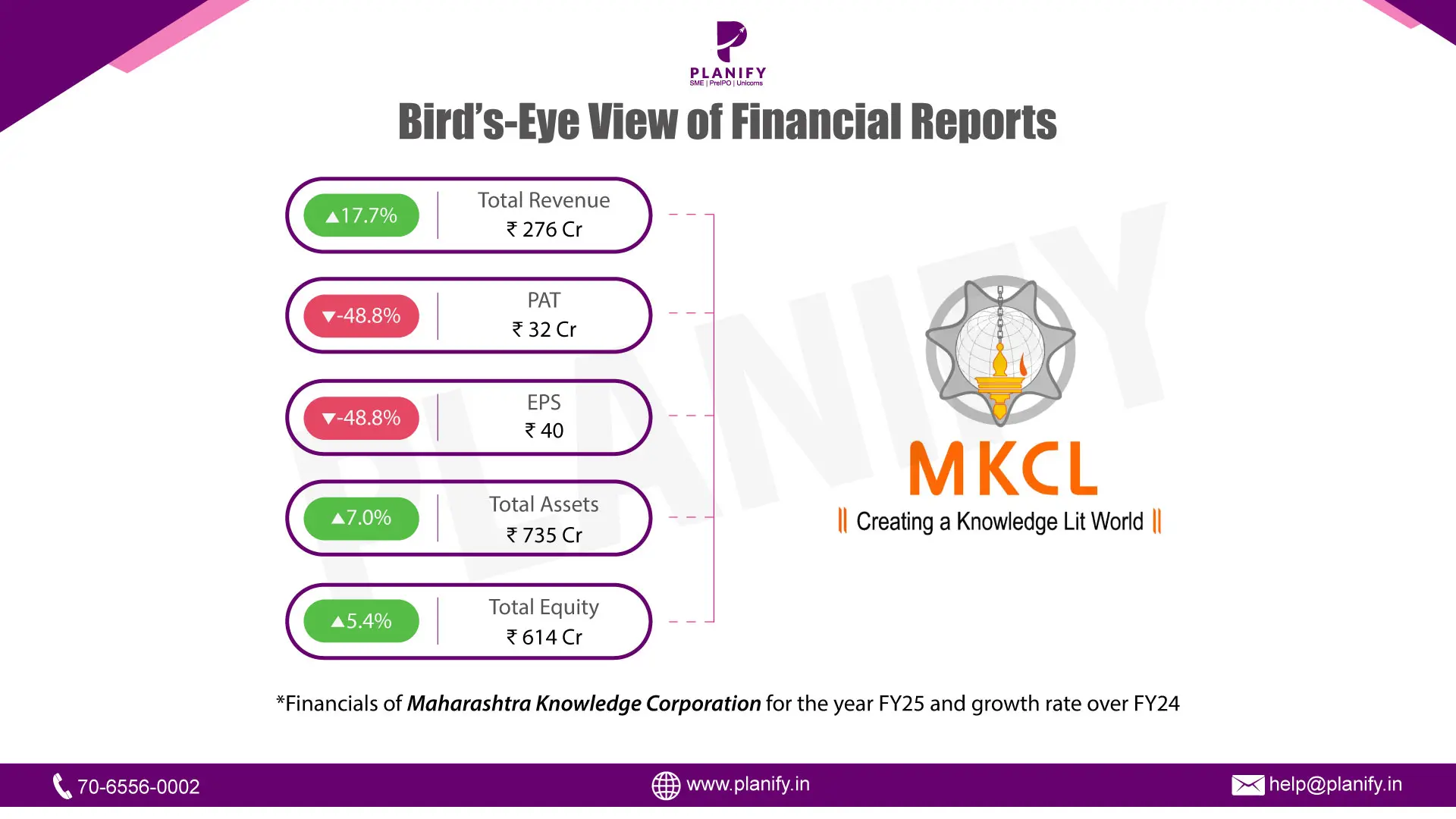

- Revenue and Profitability: MKCL delivered strong topline momentum in FY25: Revenue from operations rose 17.7% YoY to ₹276 crore (₹276 crore vs ₹235 crore), but PAT declined to ₹32 crore (-48.8% YoY). Reported profitability, however, was impacted by a one-time GST Amnesty charge of ₹46 crore. Growth was supported by higher learner volumes across MS-CIT, DEEP/SARTHI and KYP programs.

- Financial Position:The group remains debt-free with healthy liquidity with lease liability of ~₹4 crore. Cash & cash equivalents increased to ₹24 crore (₹24 crore vs ₹17 crore). Operating cash inflow (pre-exceptional) was ~₹10 crore, and investing activities generated ₹47 crore. Retained earnings (balance carried forward) stood at ₹488.0 crore.

- Future Prospects: Underlying demand drivers remain intact: expanding digital literacy & employability programs (MS-CIT enrollments ~7.99 lakh; KLiC and DEEP upticks; KYP traction), and scaling education/governance platforms (Digital University/CampusLive; ExamLive; RecruitLive/TenderLive). International footprints (e.g., Saudi Arabia ExamLive and first KLiC center in Uganda) broaden addressable markets. With one-off GST impact behind, a debt-free balance sheet, rising learner volumes, and AI-enabled product stack position the company for continued growth and margin normalization in FY26, supported by state partnerships and HE digitization.

Date: Wed 20 Aug, 2025

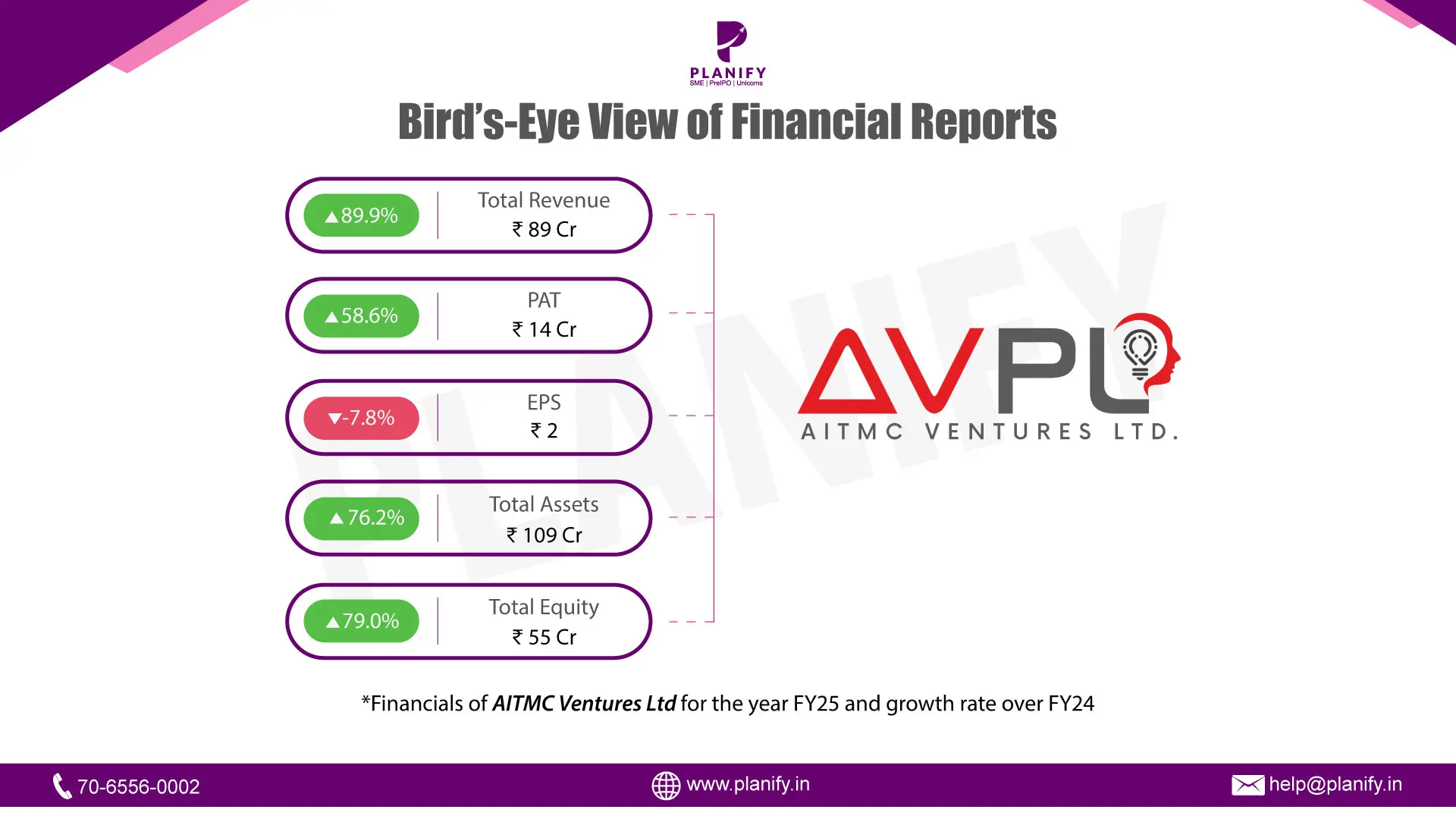

- Strong Revenue Growth: Consolidated revenue rose to ₹89 crore in FY25, up 90% YoY, supported by robust execution across core segments; however, PAT margin moderated to 16% from 19% in FY24, with PAT at ₹14 crore.

- Working Capital Stress: Operating cash flow remained negative at -₹5.8 crore (same as FY24), driven by stretched receivables at ₹44 crore (49% of sales), while inventories stayed stable at ~₹0.6 crore.

- Liquidity Pressures: Trade payables declined to ₹12 crore (vs. ₹16 crore in FY24) and advances to suppliers surged to ₹6.5 crore (vs. ₹0.2 crore in FY24), reflecting tighter cash conversion.

Date: Wed 20 Aug, 2025

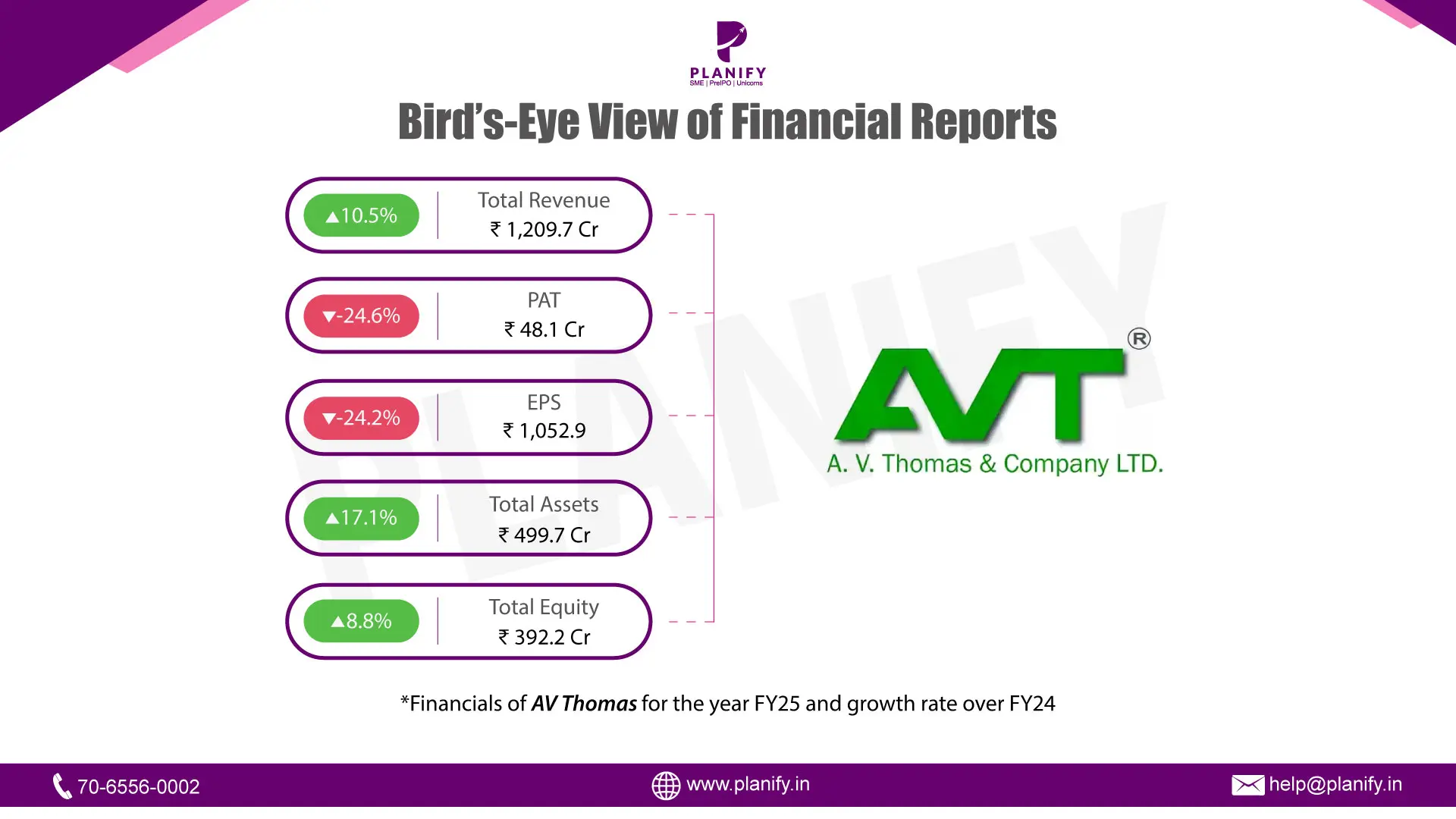

Financial Performance (FY25 vs FY24):

AV Thomas delivered a steady topline in FY25, with consolidated revenue from operations rising 10.4% YoY to ₹1,191 Cr (vs. ₹1,079 Cr in FY24). Total income (including other income) grew 10.5% YoY to ₹1,209 Cr (vs. ₹1,094 Cr).

However, operating performance softened: (vs. ₹82.4 Cr), with margins contracting to 5.8% (vs. 7.6%). PBT declined 22.8% YoY to ₹66.5 Cr (vs. ₹86.2 Cr), and PAT dropped 24.6% YoY to ₹48.1 Cr (vs. ₹63.8 Cr). Net margin compressed to 4.0% (vs. 5.9%). EPS moderated to ₹1,052.9 (vs. ₹1,388.8).

Segmental Performance (FY25 vs FY24):

- Plantation Products (tea, rubber, spices): Revenue rose 6.8% YoY to ₹612 Cr (vs. ₹574 Cr). Segment results declined to ₹49 Cr (vs. ₹57 Cr), with margin compression to 7.9% (vs. 10.0%).

- Consumer Products (packaged foods, beverages, value-added): Revenue grew 13.6% YoY to ₹531 Cr (vs. ₹467 Cr). Segment results slipped to ₹30 Cr (vs. ₹38 Cr), with margins narrowing to 5.7% (vs. 8.1%).

- Others: Revenue jumped 22.6% YoY to ₹4 Cr 8(vs. ₹39 Cr). Segment results turned positive at ₹1.2 Cr (vs. loss of ₹0.6 Cr), indicating improving traction in ancillary operations.

- Revenue Mix: Plantations contributed 51.4% of operating revenue (vs. 53.2% in FY24), Consumer Products 44.6% (vs. 43.3%), and Others 4.0% (vs. 3.6%). This reflects faster growth in Consumer Products but with thinner margins.

Operational Metrics (FY25 vs FY24):

Operationally, profitability lagged topline growth due to cost inflation and higher finance charges. Total expenses rose 12.7% YoY to ₹1,136 Cr (vs. ₹1,007 Cr), outpacing revenue growth. Segment results declined across core businesses: Plantation Products’ profit dropped 15.4% to ₹49 Cr (vs. ₹57 Cr), with margins contracting to 7.9% (vs. 10.0%), while Consumer Products’ profit fell 19.6% to ₹30 Cr (vs. ₹38 Cr), margin narrowing to 5.7% (vs. 8.1%). The “Others” segment turned profitable at ₹1.2 Cr (vs. a ₹0.6 Cr loss in FY24).

At the consolidated level, EBITDA declined 16.2% to ₹69.0 Cr (vs. ₹82.4 Cr) and EBITDA margin contracted to 5.8% (vs. 7.6%). PBT fell 22.8% YoY to ₹66.5 Cr (vs. ₹86.2 Cr), and PAT declined 24.6% to ₹48.1 Cr (vs. ₹63.8 Cr). PBT margin contracted to 5.6% (vs. 8.0%), while net margin fell to 4.0% (vs. 5.9%). Finance costs rose sharply to ₹3.5 Cr (vs. ₹1.5 Cr), further pressuring profitability.

Growth Outlook

Looking ahead, growth will be anchored by the Consumer Products division, while the Plantation segment remains exposed to commodity volatility. The near-term focus must be on margin recovery and improved cash conversion, given FY25 pressure on both segments. With a conservative capital structure and healthy liquidity, AV Thomas has sufficient headroom to fund expansion, invest in brand-building, and pursue premiumization, positioning it well for sustainable, profitable growth in FY26 and beyond.

Stay Connected, Stay Informed –

Don’t miss out on exclusive updates, market trends, and real-time investment opportunities. Be the first to know about the latest unlisted stocks, IPO announcements, and curated Fact Sheets, delivered straight to your WhatsApp.