Planify Feed

Date: Wed 20 Aug, 2025

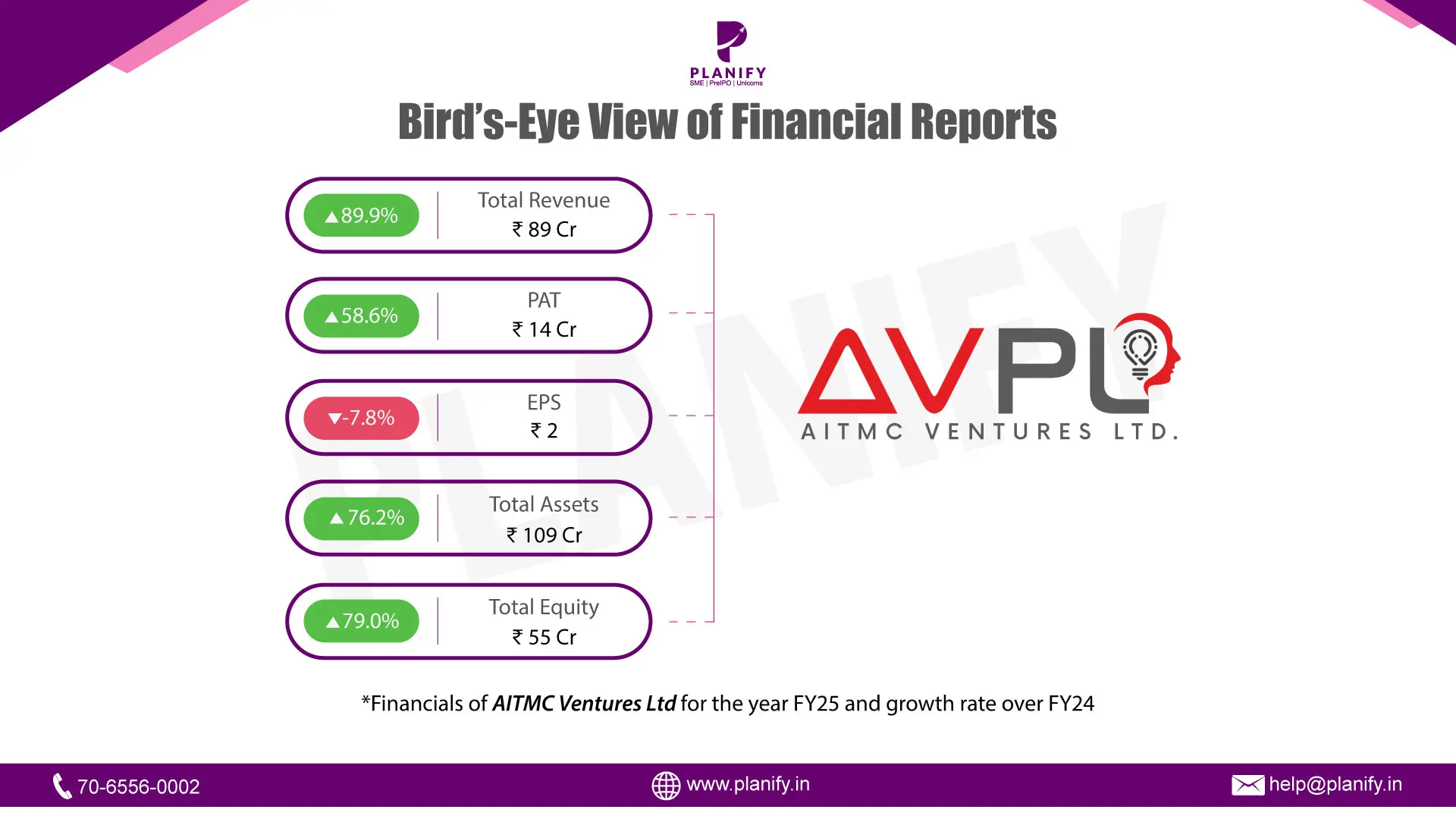

- Strong Revenue Growth: Consolidated revenue rose to ₹89 crore in FY25, up 90% YoY, supported by robust execution across core segments; however, PAT margin moderated to 16% from 19% in FY24, with PAT at ₹14 crore.

- Working Capital Stress: Operating cash flow remained negative at -₹5.8 crore (same as FY24), driven by stretched receivables at ₹44 crore (49% of sales), while inventories stayed stable at ~₹0.6 crore.

- Liquidity Pressures: Trade payables declined to ₹12 crore (vs. ₹16 crore in FY24) and advances to suppliers surged to ₹6.5 crore (vs. ₹0.2 crore in FY24), reflecting tighter cash conversion.

Date: Wed 20 Aug, 2025

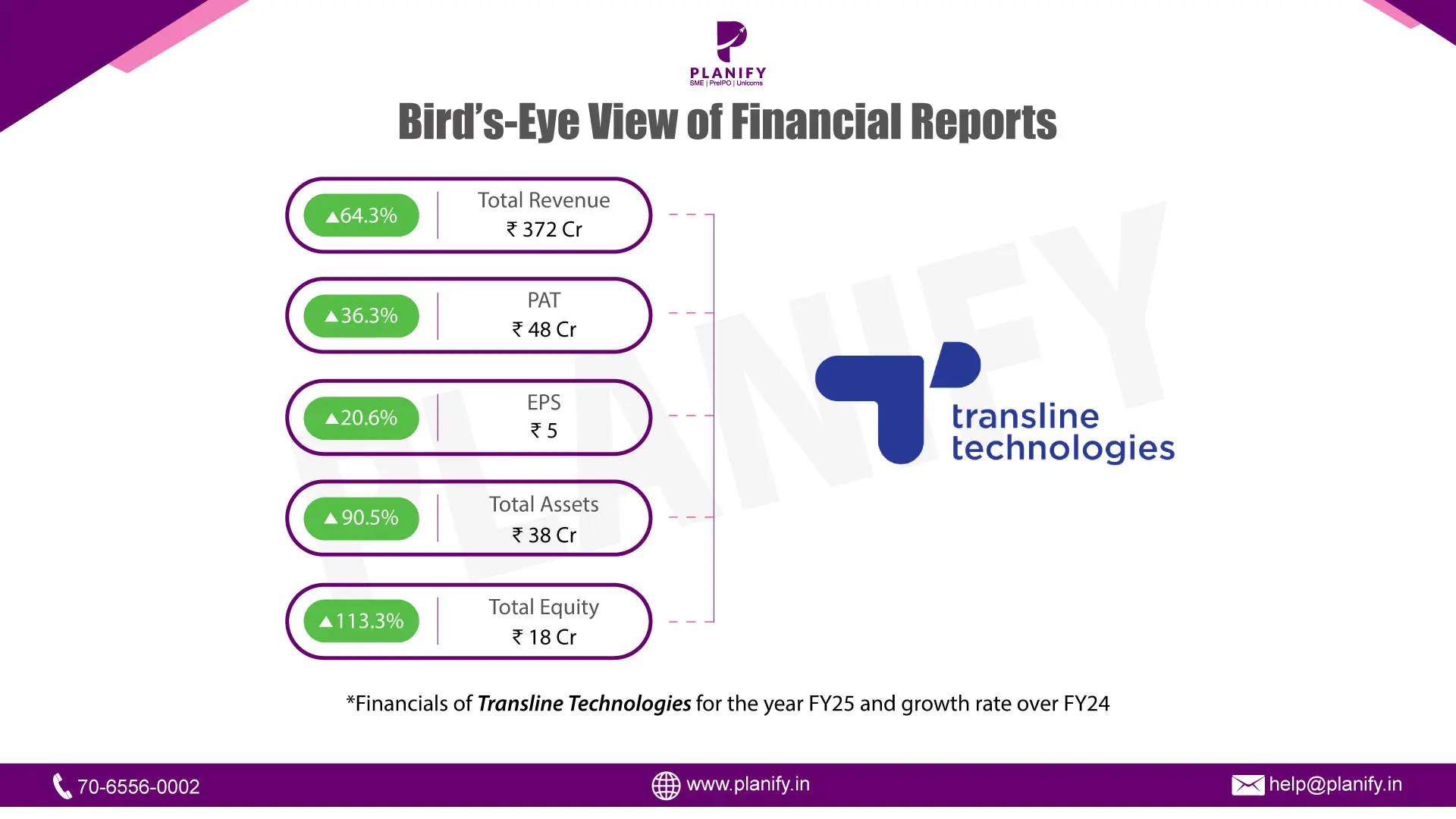

About the Company: Transline Technologies Limited (TTL) is a specialized technology solutions provider focused on integrated security and surveillance systems, biometric authentication platforms, and AI-driven software. Its diversified revenue model includes system integration projects, SaaS subscriptions, hardware and software sales, and technical services. Proprietary platforms such as StorePulse (AI video analytics), CamStore (video compression and storage optimization), and CheckCam (CCTV health monitoring) position TTL as a trusted partner to government bodies, PSUs, smart cities, and enterprises across transportation, retail, logistics, and telecom. In FY25, revenue was well-distributed across video surveillance (36%), biometrics (18%), IT infrastructure (26%), services (19%), and SaaS offerings, backed by capabilities in IoT-enabled infrastructure, system integration, and cloud deployment.

Financial and Operational Performance: The company has delivered strong growth, with consolidated revenue rising from ₹115 crore in FY23 to ₹372 crore in FY25 (~79% CAGR). EBITDA increased to ₹79 crore, with margins expanding to 21%, while net profit improved to ₹48 crore from ₹10 crore in FY23, reflecting disciplined execution and cost optimization. TTL maintains a prudent capital structure with net debt-to-equity at ~0.5x. Operationally, the company closed FY25 with an order book of ~₹199 crore and a steadily expanding customer base (296 in FY25 vs. 158 in FY23). Its 23-member R&D team has been instrumental in developing scalable AI-driven platforms and IoT-integrated solutions, strengthening proprietary SaaS offerings and creating value-added, recurring revenue streams.

Future Outlook: Looking forward, TTL is well-positioned to benefit from India’s infrastructure expansion, energy transition, and government focus on railways, smart cities, and power transmission. The company expects sustained double-digit growth over the next 2–3 years, underpinned by its robust order book, diversification into high-growth verticals, and continued investment in R&D. Management’s strategic vision is to establish TTL as a one-stop, integrated solutions provider for security, surveillance, and smart infrastructure, with increasing emphasis on technology-driven, recurring-revenue models.

Date: Wed 20 Aug, 2025

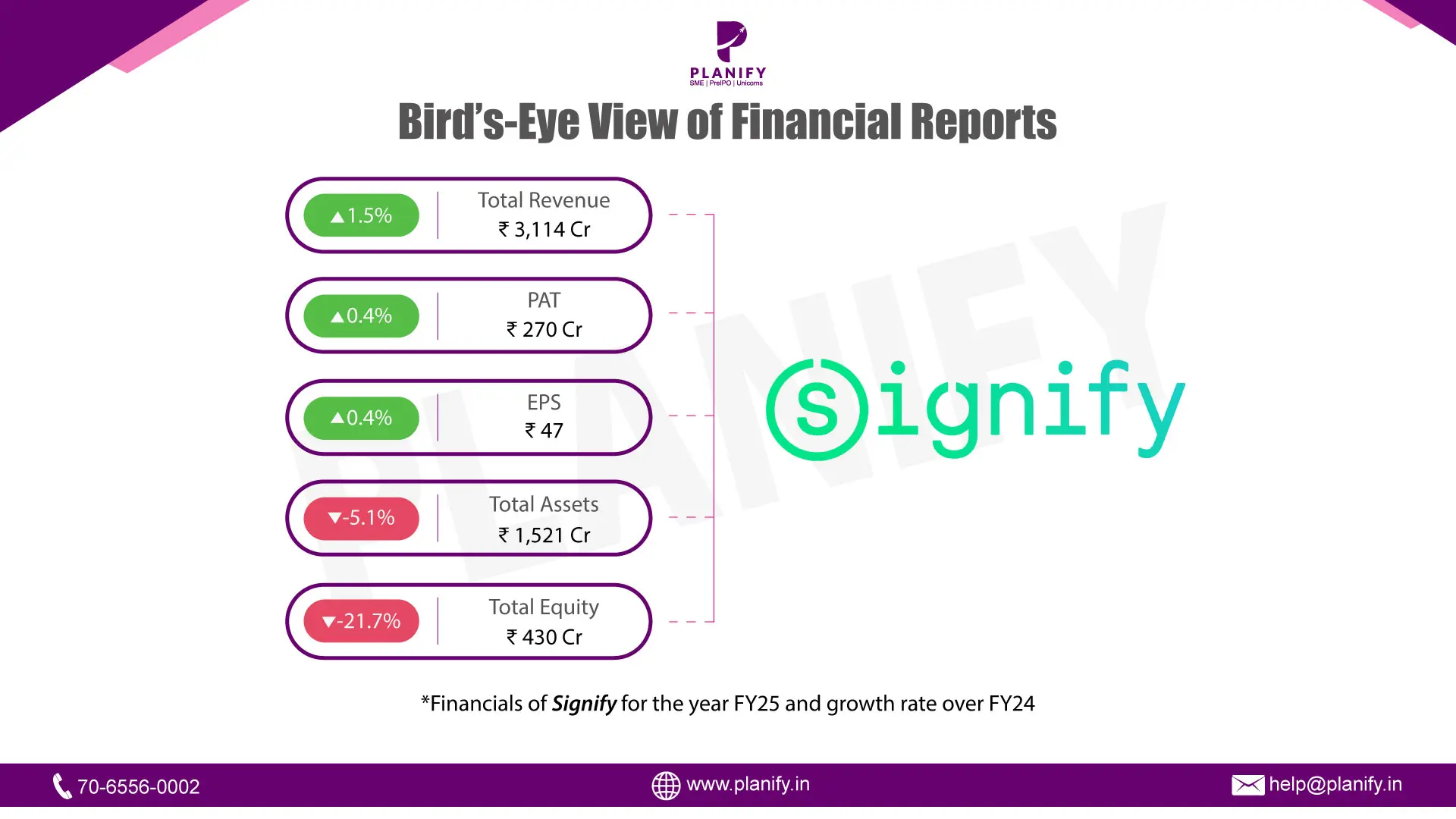

- Financial Developments: In FY25, Signify Innovations India Limited reported a total income of ₹3,143 crore, with Profit Before Tax at ₹366 crore, translating into an EPS of ₹46.96. Despite pricing pressures in the domestic lighting industry, the company maintained profitability and registered year-on-year growth, supported by strong performance in its connected offerings portfolio. Operationally, Signify expanded its retail footprint to 320+ stores with 35 new launches, enhanced its D2C platform with over 1,100 SKUs, and scaled its e-commerce presence. It also entered into a 50:50 joint venture with Dixon Technologies to strengthen local manufacturing and improve cost competitiveness, reinforcing its alignment with the “Make in India” strategy.

- Operational Developments: The company continued to lead the LED transformation in India, with new product launches and expansion of Philips Smart Light Hubs, while also rolling out DIGi Shield, the industry’s first digital warranty management platform. Sustainability remained core, with significant progress in its Brighter Lives, Better World 2025 program — reducing value-chain emissions by 40% against 2019 levels, inclusion in the Dow Jones Sustainability World Index for the 8th consecutive year, and a roadmap to net-zero by 2040. On the CSR front, Signify positively impacted 1.6 million lives, lighting up 840 villages, 191 schools, 53 healthcare centers, and 35 playgrounds across India. These initiatives strengthened both its brand equity and social impact footprint.

- Future Outlook: For FY26, the company expects a demand revival supported by government infrastructure spending and a pickup in private capex. Growth in the professional lighting business is projected to outpace consumer demand, while connected and smart lighting solutions remain the key revenue driver. However, management remains cautious on cost and pricing trends in the current dynamic environment. Priorities include innovation-led product differentiation, expansion in digital and omni-channel sales, further localization through the Dixon JV, and operational excellence. With its strong financial base, proven execution, and sustainability-led strategy, Signify is well placed to sustain its market leadership in India’s ₹30,000+ crore lighting industry while protecting margins and shareholder value.

Date: Tue 19 Aug, 2025

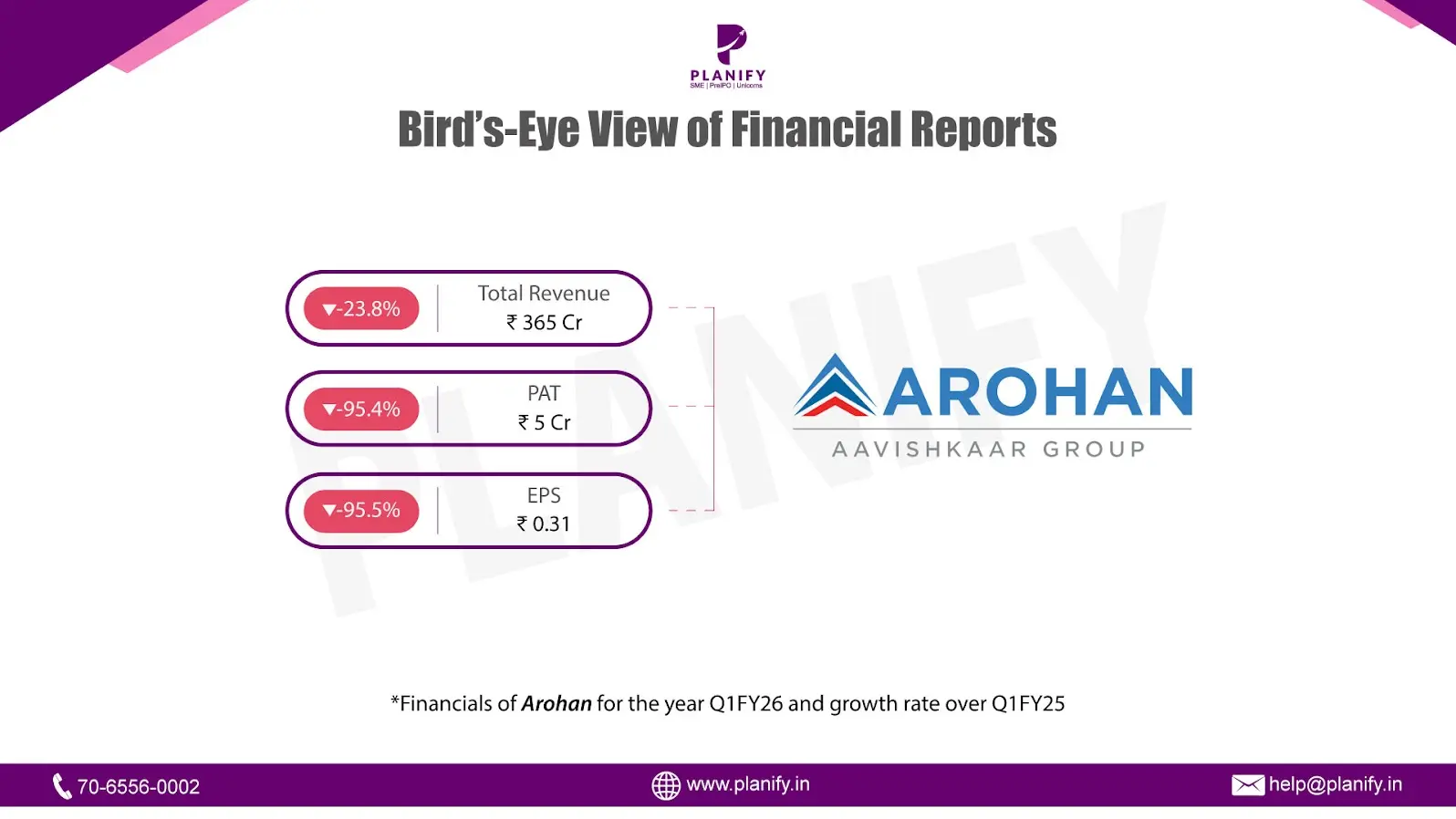

- Financial Performance (Q1 FY26 vs Q1 FY25): In Q1 FY26, Arohan Financial reported total revenue of ₹365 Cr, a decline of 23.8% YoY from ₹479 Cr in Q1 FY25, primarily due to lower interest income and a steep drop in non-interest income. Finance costs fell by 28.5% YoY to ₹126 Cr from ₹177 Cr, but impairment on financial instruments surged to ₹103 Cr, compared to ₹40 Cr in Q1 FY25, reflecting higher credit stress. Profit Before Tax (PBT) stood at ₹6 Cr, down sharply by 95.5% YoY from ₹139 Cr in Q1 FY25. Profit After Tax (PAT) also contracted drastically to ₹5 Cr, a decline of 95.4% YoY from ₹104 Cr last year. Earnings Per Share (EPS) fell to ₹0.31, compared to ₹6.83 in Q1 FY25.

- Operational Metrics (Q1 FY26 vs Q1 FY25): Net Profit Margin: Dropped to 1.3%, from 21.7% in Q1 FY25, underscoring profitability pressure. Gross NPA (GNPA): Stood at 2.61%, slightly up from 2.30% in Q1 FY25, showing deterioration in asset quality. Net NPA (NNPA): Rose to 0.71%, compared to 0.55% last year. Provision Coverage Ratio (PCR): Weakened to 73.16%, from 82.35% in Q3 FY25, showing reduced buffer against credit losses. Capital Adequacy Ratio (CAR): Healthy at 36.6%, providing strong capitalization. Loan Book (Total Assets): Total debts to total assets ratio at 68.9% indicates moderate leverage, with net worth of ₹2,017 Cr, reflecting a stable equity base.

- Strategic Developments: Q1 FY26 was challenging for Arohan Financial, as revenues contracted and profitability was severely impacted by rising impairment costs and weaker non-interest income. The increase in NPAs highlights ongoing asset quality stress, which, coupled with a dip in provision coverage, points to rising risks. However, the company maintains a robust capital adequacy ratio, offering resilience to withstand shocks. With the RBI’s recent lifting of lending restrictions (January 2025), Arohan has resumed disbursements, which should aid loan book growth and revenue revival in the coming quarters. The key focus areas going forward will be improving asset quality, tightening cost structures, and regaining market confidence to restore profitability momentum.

Date: Tue 19 Aug, 2025

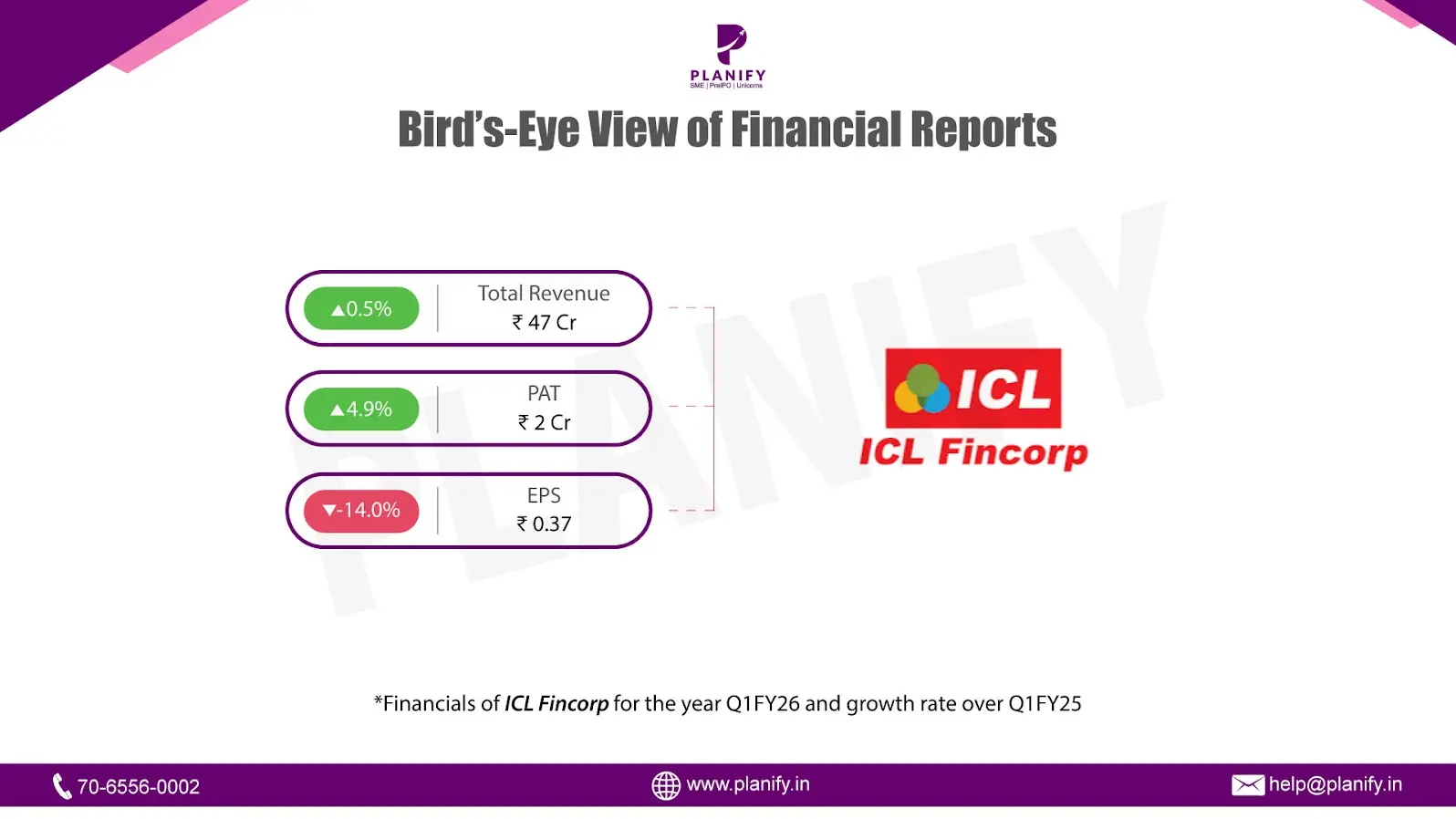

- Financial Performance (Q1FY26 vs Q1FY25): In Q1FY26, ICL Fincorp reported a modest 0.5% YoY growth in total income to ₹47.2 Cr, compared with ₹47.0 Cr in Q1FY25, aided by higher revenue from operations. Operating performance remained largely flat, with Profit Before Tax (PBT) rising marginally by 1.2% YoY to ₹2.88 Cr, against ₹2.86 Cr in the prior year. At the net level, profitability showed a slight improvement, as Profit After Tax (PAT) increased 4.9% YoY to ₹2.1 Cr, versus ₹2.0 Cr in Q1FY25, supported by lower tax outgo. However, Earnings Per Share (EPS) declined to ₹0.37, compared with ₹0.43 a year earlier, reflecting weaker per-share earnings growth.

- Operational Metrics (Q1FY26 vs Q1FY25): Net Profit Margin improved slightly to 4.5% from 4.3% last year, due to tax savings despite flat PBT. Asset Quality: Gross Stage 3 Loan Assets (GNPA) improved to 0.60% from 1.06% in Q4FY25, while Net Stage 3 Loan Assets (NNPA) declined to 0.51% from 0.94%, indicating strengthening collections. Provision Coverage Ratio (PCR) rose to 15.5% from 11.4%. Capital Adequacy Ratio (CAR) declined to 18.0% from 19.3%, but remains comfortably above regulatory requirements.

- Strategic Developments: Q1FY26 was a quarter of stable revenue and marginal profit growth for ICL Fincorp. While income growth remained marginal and PBT was nearly flat, the bottom line saw modest improvement due to lower tax expenses. On the positive side, asset quality strengthened, with both GNPA and NNPA ratios improving and provision coverage increasing, reflecting better recoveries and risk management. However, the decline in capital adequacy and higher leverage highlight increased reliance on borrowings to support growth. Overall, the quarter underscored steady topline performance with thin margins, partly cushioned by encouraging improvements in asset quality.

Date: Mon 18 Aug, 2025

Dear Investors,

We wish to inform you that Imagine Marketing Ltd. (boAt) has scheduled its 12th Annual General Meeting (AGM) on Monday, September 8, 2025 at 11:30 A.M. (IST) through Video Conferencing (VC) / Other Audio Visual Means (OAVM). The AGM Notice and Annual Report for FY2024–25 are available on the company’s Investor Relations page and on the NSDL portal (www.evoting.nsdl.com).

Members holding shares as on September 1, 2025 (cut-off date) can participate and vote. Remote e-voting will be open from September 4, 2025 (9:00 AM IST) to September 7, 2025 (5:00 PM IST). E-voting during the AGM will also be available for members who did not vote earlier. Shareholders may join the meeting virtually via NSDL’s e-voting system and register in advance as speakers (between August 25–31, 2025).

Agenda for the 12th AGM

- Ordinary Business

- Adoption of the Audited Standalone Financial Statements for FY2024–25 along with the Directors’ and Auditors’ Reports.

- Adoption of the Audited Consolidated Financial Statements for FY2024–25 along with the Auditors’ Report.

- Re-appointment of Mr. Vivek Gambhir (DIN: 06527810), Non-Executive Director and Chairman, who retires by rotation and offers himself for re-appointment.

- Special Business

4. Approval of remuneration for Mr. Aman Gupta (DIN: 02249682), Whole-Time Director, for FY2025–26.

- Fixed salary: ₹2.0 crore per annum

- Performance-linked component: ₹0.5 crore per annum (20% of total package)

- Usual perquisites (PF, gratuity, leave encashment, allowances) in line with company policy.

- In the event of no or inadequate profits, the above shall be treated as minimum remuneration in accordance with the Companies Act, 2013.

Investors are encouraged to review the Annual Report FY25, cast their votes via the remote e-voting facility within the stipulated timelines, and attend the AGM for updates on the company’s strategic direction and financial performance.

Date: Mon 18 Aug, 2025

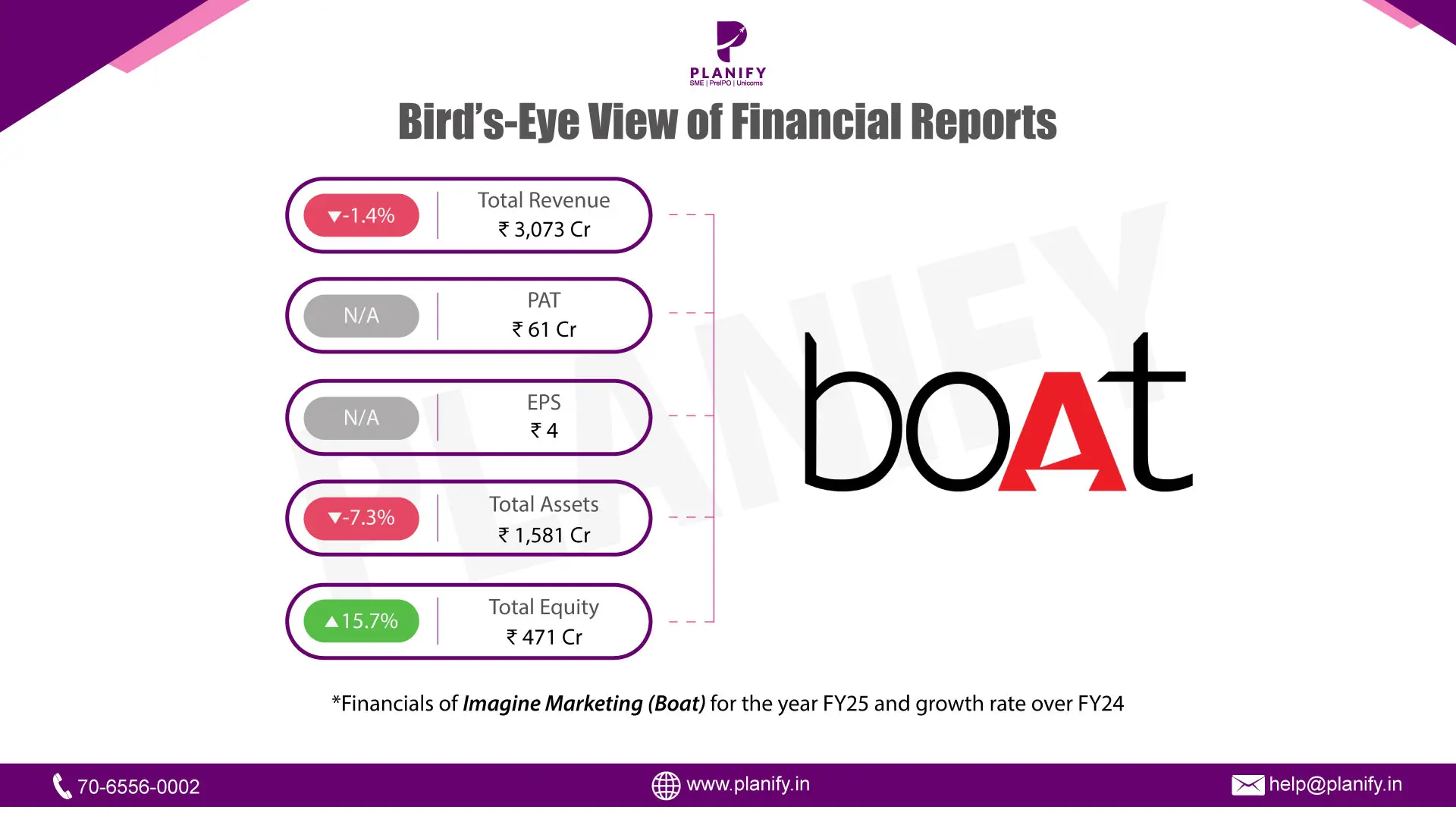

- Financial Performance: Imagine Marketing Ltd. (boAt) delivered a flat performance in FY25, with consolidated revenue of ₹3,073 crs, marking a -1.4% YoY growth because of muted consumer demand and intense competition in the wearables and hearables space. The company reinforced its leadership in India’s audio and wearables segment, maintaining over 40% market share in True Wireless Stereo (TWS) and 30%+ in wearables, supported by strong distribution, innovative product launches, and impactful brand campaigns. PAT stood at ₹61 crs, translating to a margin of 1.9%, reflecting cost optimization efforts continued investments in R&D and marketing.

- Operational Developments: Operationally, boAt strengthened its product innovation and supply chain capabilities, with over 80% of products now manufactured locally under the ‘Make in India’ initiative. The company expanded its retail footprint through 20,000+ touchpoints alongside robust traction on e-commerce platforms. It also broadened its premium product portfolio under boAt, Nirvana, and Rockerz, while diversifying into smartwatches and gaming accessories to enhance its ecosystem play. Strategic partnerships with manufacturers and technology collaborators further improved speed-to-market and cost efficiency, reinforcing its competitive positioning.

- Future Outlook: Looking forward, management remains optimistic about achieving double-digit growth in FY26, underpinned by sustained demand in wearables, premiumization, and international expansion. The company intends to leverage its strong brand equity, expand exports into high-potential markets, and deepen penetration across Tier-II and Tier-III cities. Continued investments in design, R&D, and software capabilities will strengthen boAt’s transition beyond hardware into a connected lifestyle ecosystem. While competitive pricing may keep near-term margins under pressure, the long-term outlook remains positive, with scale, localization, and ecosystem-led innovation supporting both profitability and market leadership.

Date: Mon 18 Aug, 2025

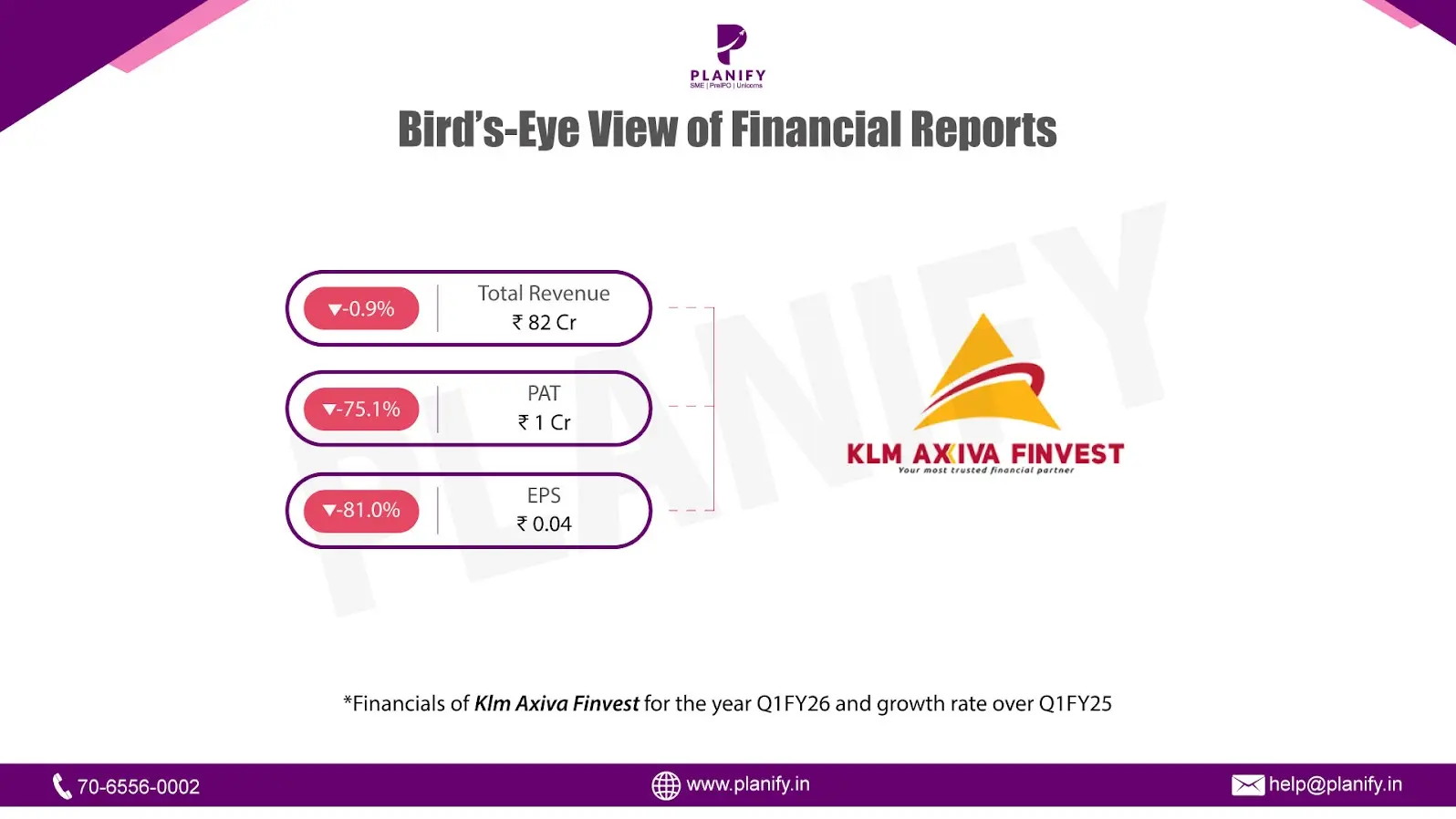

- Financial Performance (Q1FY26 vs Q1FY25): KLM Axiva reported a 0.9% YoY decline in total income to ₹82 Cr in Q1FY26 from ₹83 Cr in Q1FY25, as interest income remained nearly flat at ₹80 Cr (vs ₹81 Cr). Other income, however, rose 22.4% YoY to ₹2 Cr from ₹1.7 Cr, partially offsetting weaker lending yields. Total expenses grew 4.9% YoY to ₹81 Cr (vs ₹77 Cr), driven mainly by higher finance costs (+12.1% YoY to ₹45 Cr). Impairment charges fell sharply to ₹0.5 Cr (vs ₹1.5 Cr), offering some relief. Profit Before Tax (PBT) declined 80.8% YoY to ₹1.1 Cr from ₹5.7 Cr, reflecting pressure from rising costs. Profit After Tax (PAT) dropped 75.1% YoY to ₹1 Cr from ₹4 Cr. Earnings per share (EPS) stood at ₹0.04 in Q1FY26, compared to ₹0.21 in Q1FY25.

- Operational Metrics (Q1FY26 vs Q1FY25): Net profit margin contracted sharply to 1.3% in Q1FY26 from 5.3% in Q1FY25, highlighting reduced profitability. Gross NPA (GNPA) rose to 2.29% from 1.90%, while Net NPA (NNPA) increased to 1.37% from 1.20%, reflecting some deterioration in asset quality. The Provision Coverage Ratio (PCR) remained moderate at around 40.2%. The loan portfolio remained largely flat at ₹1,656 Cr compared to ₹1,660 Cr in Q1FY25, indicating a cautious lending approach. The Capital Adequacy Ratio (CRAR) stood at 16.4%, comfortably above regulatory requirements.

- Strategic Developments:Q1FY26 was a steady quarter for KLM Axiva, with income growth remaining flat and profitability moderating due to higher funding costs and narrower spreads. Asset quality showed a marginal weakening, with both GNPA and NNPA rising slightly but staying within manageable levels. On the positive side, impairment charges declined significantly on a year-on-year basis, and capital adequacy remained comfortably above regulatory requirements. The loan book was largely unchanged, reflecting a cautious and selective approach to disbursements in a tighter credit environment. Looking ahead, the company aims to focus on optimizing funding costs, improving lending margins, strengthening credit underwriting practices, and gradually accelerating loan growth while maintaining asset quality.

Date: Mon 18 Aug, 2025

Dear Investors,

We wish to inform you that the 43rd Annual General Meeting (AGM) of Studds Accessories Limited will be held on Saturday, September 6, 2025, at 4:00 P.M. (IST) through Video Conferencing (VC) / Other Audio-Visual Means (OAVM). The AGM has been convened in compliance with the Companies Act, 2013, SEBI regulations, and applicable MCA circulars.

Key Agenda Items for the AGM

Ordinary Business

To adopt the Audited Standalone and Consolidated Financial Statements for FY2024-25, along with the Board’s and Auditors’ Reports.

To declare a Final Dividend of ₹2.50 per equity share (50% on face value of ₹5 each) for FY2024-25, amounting to an aggregate payout of ~₹9.84 crore, payable to shareholders whose names appear in the Register/Beneficial Owners as on August 30, 2025.

To consider the re-appointment of Mr. Madhu Bhushan Khurana (DIN: 00172770) as Director, who retires by rotation and has attained the age of seventy years, by way of a Special Resolution.

Special Business

4. Appointment of Chandrasekaran Associates, Company Secretaries as Secretarial Auditor for a term of five years (FY2025-26 to FY2029-30), with an initial remuneration of ₹4,00,000 plus taxes and expenses.

5. Approval of Related Party Transaction (RPT) – remuneration to Ms. Chand Khurana, relative of the promoters, for holding an office/place of profit in the company, with remuneration of ₹3,65,826 per month (subject to maximum limit of ₹80 lakh p.a. for five years, effective July 1, 2025).

6. Approval of Related Party Transaction (RPT) – remuneration to Ms. Garima Khurana, relative of the promoters, for holding an office/place of profit in the company, with remuneration of ₹1,94,557 per month (subject to maximum limit of ₹50 lakh p.a. for five years, effective July 1, 2025).

7. Continuation of payment of remuneration to promoter-executive directors (Mr. Madhu Bhushan Khurana, Mr. Sidhartha Bhushan Khurana, and Ms. Shilpa Arora) beyond the 5% net profit threshold prescribed under SEBI Listing Regulations, until the expiry of their respective terms.

Dividend & Shareholder Participation

Shareholders are requested to note that the final dividend of ₹2.50 per share (FY25) will be distributed subject to AGM approval. Voting on all resolutions can be exercised electronically through remote e-voting prior to the AGM or during the meeting via VC/OAVM.

Date: Mon 18 Aug, 2025

Notice is hereby given that the 41st Annual General Meeting (AGM) of the Members of Five-Star Business Finance Limited (the “Company”) will be held on Tuesday, September 9, 2025, at 10:00 AM (IST). The meeting will take place through Video Conferencing (VC) and Other Audio-Visual Means (OAVM) to discuss the following agenda items:

Ordinary Business:

- To receive, consider, and adopt the audited financial statements of the Company for the financial year ended March 31, 2025, together with the reports of the Directors’ and Auditor’s thereon.

- To declare a final dividend for the Financial Year ended March 31, 2025: Resolved that a final dividend of ₹2 per equity share (i.e., 200% of the face value) is hereby declared, as recommended by the Board of Directors, on the fully paid-up equity shares of ₹1 each of the Company for the financial year ended March 31, 2025. This dividend will be paid to the members whose names appear in the Company’s Register of Members as of Thursday, August 14, 2025, which has been established as the record date for this purpose.

- To appoint a director in place of Mr. Thirulokchand Vasan (holding DIN: 07679930), who retires by rotation and, being eligible, has offered himself for re-appointment.

- Appointment of Secretarial Auditors: Resolved that, by Section 204 of the Companies Act, 2013, and related provisions, M/s. S. Sandeep & Associates, Practising Company Secretaries, Chennai (Firm Registration No: P2025TN103600; PR No: 6526/2025), be appointed as Secretarial Auditors for a term of 5 consecutive years from FY 2025-26 to FY 2029-30, at a remuneration of ₹ 2,20,000 (excluding out-of-pocket expenses and taxes) for FY 2025-26.

- Fixing of borrowing limits for the Company: Resolved that, per section 180(1)(c) of the Companies Act, 2013 and applicable laws, the Company consents to the Board of Directors (including any committee authorized by the Board) to borrow up to ₹ 12,000 Crores (Indian Rupees Twelve Thousand Crores only) at any time, including amounts already borrowed, from bankers, NBFCs, financial institutions, or any party permitted by law, whether unsecured or secured.

- Creation of Charges on the assets of the Company

- Offer/invitation to subscribe to Non-Convertible Debentures (NCDs) on a private placement basis: Resolved that, by sections 42 and other relevant provisions of the Companies Act, 2013, and associated regulations, the Board of Directors is authorized to issue and offer Non-Convertible Debentures (NCDs) on a private placement basis, aggregating up to ₹ 4,000 Crores, in one or more series. This authorization includes determining the terms of the issue, timing, utilization of proceeds, and related matters, subject to obtaining necessary approvals from SEBI, Stock Exchanges, and other authorities.

Date: Mon 18 Aug, 2025

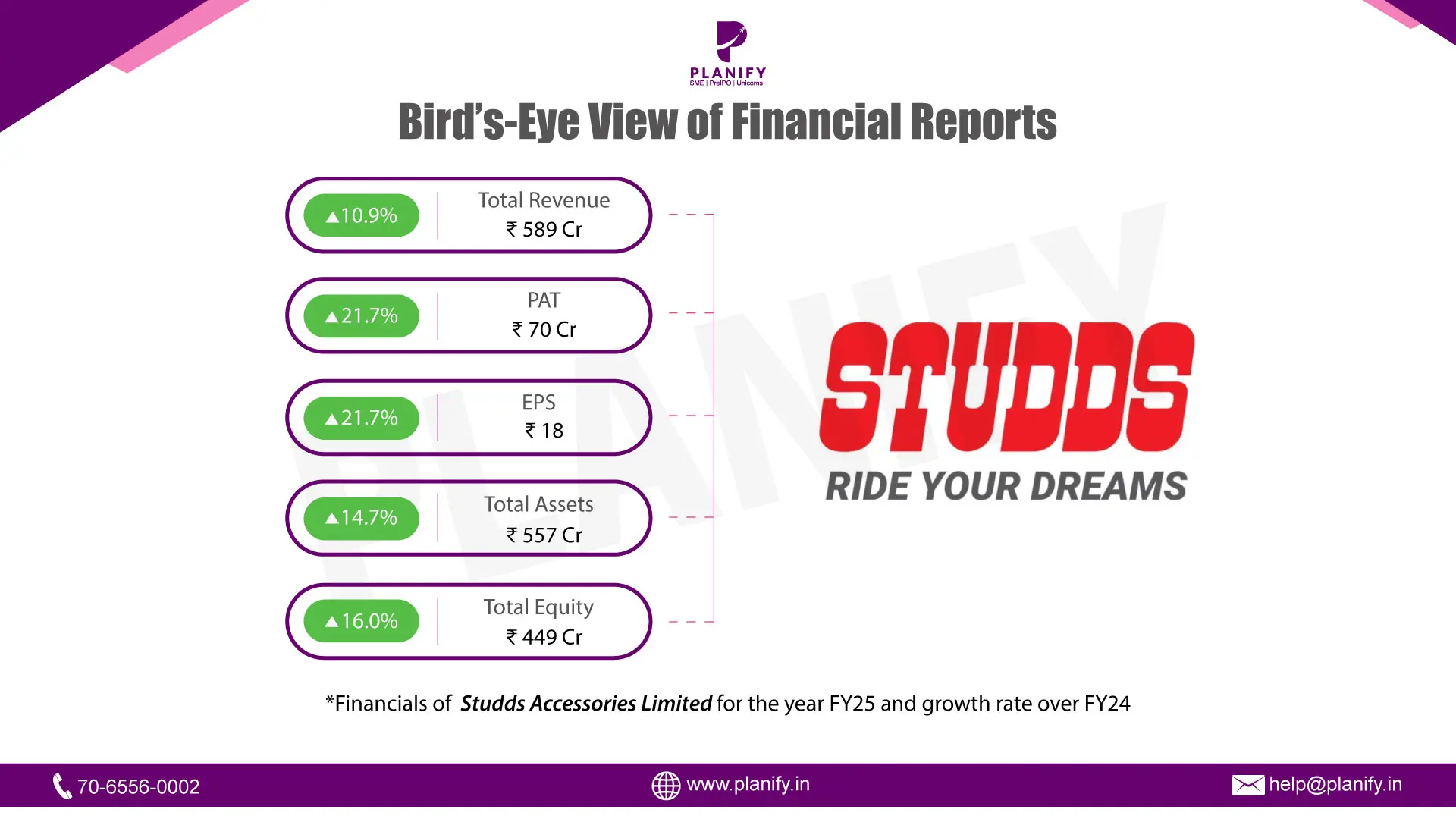

- Financial Performance: Studds Accessories Limited delivered a strong FY25 performance, consolidating its position as the world’s largest two-wheeler helmet manufacturer by volume. Revenue from operations grew ~11% YoY to ₹589 crs, driven by robust demand across domestic and international markets. Exports were a key growth lever, rising ~82% to ₹97 crs. EBITDA expanded to ₹118 crs with margins above 20%, aided by disciplined cost management, stronger procurement practices, and efficiency gains. Profit after tax improved to ₹70 crs, while net worth rose to ₹450 crs, underscoring the company’s financial resilience.

- Operational Developments: Operationally, Studds produced over 7.5 million helmets and boxes, leveraging four advanced facilities in Faridabad and a vertically integrated model that ensures quality, safety, and cost competitiveness. The company introduced smart helmets with Bluetooth connectivity and advanced safety features, alongside its innovative “Thunder Detect” compliance helmet for delivery fleets, showcasing its R&D leadership. Strategic milestones included the acquisition of Bikerz Us Inc. in the US to strengthen its Americas presence and ongoing capacity expansion with a fifth facility scheduled to be operational by FY26. Complementing this, investments in marketing, digital transformation (ERP, WMS, B2B/B2C portals), and sustainability initiatives further enhanced global competitiveness.

- Future Outlook: Looking ahead, Studds is well-positioned to benefit from regulatory mandates for BIS-certified helmets, rising safety awareness, and growing premiumization trends. The Indian two-wheeler helmet market is projected to grow at a 6.1% CAGR to 3.5 crs units by CY29, while global expansion opportunities under the “China+1” strategy remain strong. The company aims to scale production capacity, deepen penetration in the Americas and Europe, and pioneer eco-friendly, tech-enabled products. While risks such as inflationary pressures, raw material price volatility, regulatory costs, and competition from unorganized players remain, Studds’ strong brand equity, innovation pipeline, and capital-efficient model provide a robust foundation for sustained growth.

Date: Mon 18 Aug, 2025

InSolare Energy Limited has announced that the 17th Annual General Meeting (AGM) of the Company will be held on Tuesday, 9th September 2025 at 11:00 A.M. IST at Hotel ITC Welcome, Ashram Road, Ahmedabad and also through Video Conferencing/Other Audio-Visual Means (VC/OAVM).

The following key matters have been placed before shareholders for consideration and approval:

Ordinary Business

Adoption of the audited standalone and consolidated financial statements of the Company for the year ended 31st March 2025, along with the reports of the Board of Directors and Auditors thereon.

Re-appointment of Mr. Sunit Dharamveer Tyagi (DIN: 01025709), Managing Director, who retires by rotation and offers himself for re-appointment.

Special Business

3. Regularisation of Mr. Gajanan Vithal Gandhe (DIN: 02023395) as Non-Executive Independent Director of the Company for a term of five consecutive years up to 25th December 2029.

4. Regularisation of Mrs. Pooja Bahry (DIN: 01091905) as Non-Executive Independent Director of the Company for a term of five consecutive years up to 22nd January 2030.

5. Increase in the Authorised Share Capital of the Company from ₹1.8 crores to ₹30 crores and consequential amendment to the Memorandum of Association.

6. Sub-division of equity shares from face value of ₹10 per share to ₹2 per share, effective from the record date of 12th September 2025.

7. Issue of bonus shares in the ratio of 7:1, i.e. seven fully paid-up equity shares of ₹2 each for every one fully paid-up equity share of ₹2 held, by capitalising reserves up to ₹11 crores.

8. Approval for borrowings over and above the limits specified under Section 180(1)(c) of the Companies Act, 2013, up to an overall limit of ₹1000 crores.

The Board has stated that these proposals are aligned with the Company’s strategy of strengthening governance, augmenting its capital base, enhancing shareholder value, and preparing for a potential Initial Public Offer (IPO) in the near future.

Date: Mon 18 Aug, 2025

It is hereby informed that Madhur Iron & Steel (India) Limited has issued a notice convening its 1st Extra-Ordinary General Meeting (EGM) for the financial year 2025-26. The meeting is scheduled to be held on Saturday, 23rd August 2025 at 5:00 P.M. at the company’s registered office in Bhilai, Chhattisgarh.

The following key matters are proposed for shareholders’ consideration:

Regularisation of Appointment of Independent Director – Mr. Prashant Samantrai (DIN: 07780428) has been recommended for appointment as an Independent Director for a five-year term.

Change in Designation of Director – Mr. Rajesh Modha (DIN: 09419073) has been proposed to be designated as Whole-Time Director for a period of five years commencing from 16th August 2025.

Approval for Loans, Investments, and Guarantees – Authorization is sought for the Board to make investments, give loans, guarantees, or provide security up to a limit of INR 200 crores, exceeding the limits prescribed under Section 186 of the Companies Act, 2013.

Increase in Authorised Share Capital – The authorised capital of the company is proposed to be increased from INR 25 crores to INR 75 crores, with necessary amendments in the Memorandum of Association.

Issue of Bonus Shares – A bonus issue of equity shares in the ratio of 1:1 (one new share for every existing share) has been recommended, by capitalising reserves of INR 14.89 crores.

The Board has stated that these measures are aimed at strengthening the company’s governance, operational capacity, and capital structure, while also rewarding shareholders through the proposed bonus issue.

Date: Thu 14 Aug, 2025

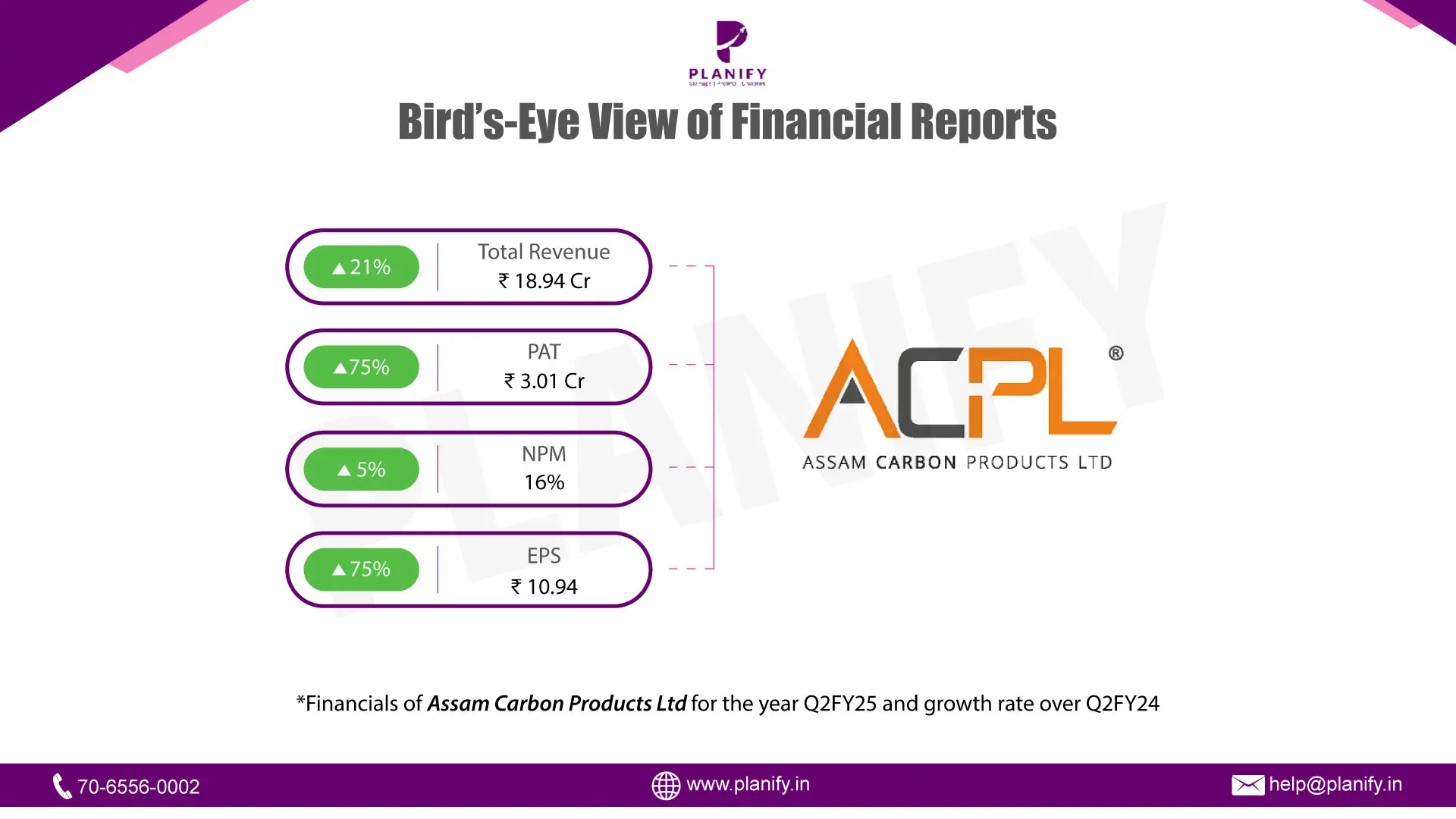

This update provides an overview of Assam Carbon Products Limited's performance for the quarter ended June 30, 2025, highlighting key strategic and operational drivers.

Date: Thu 14 Aug, 2025

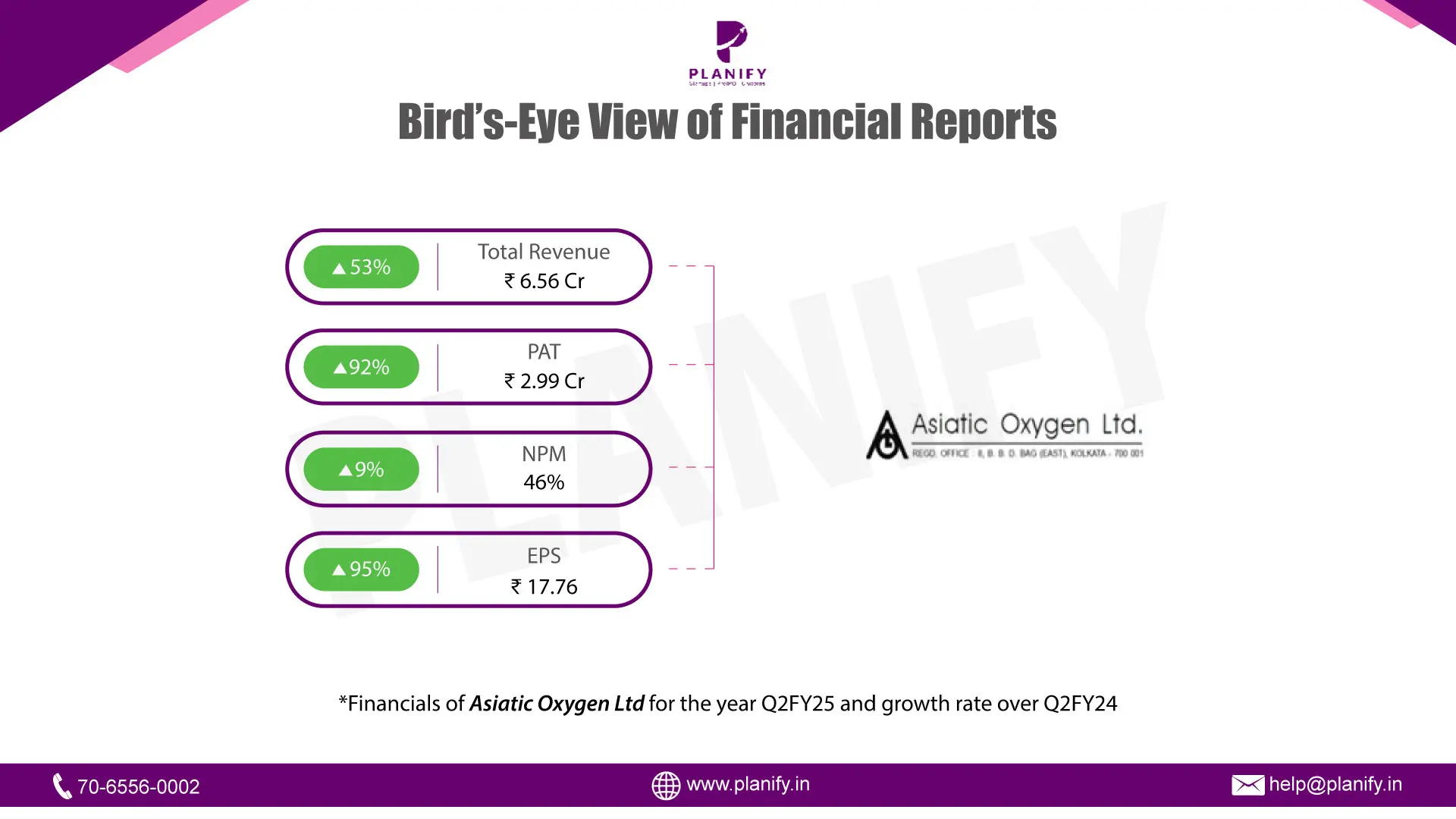

ASIATIC OXYGEN LIMITED has demonstrated a strong financial performance for the second quarter of Fiscal Year 2025 (Q2FY25) compared to the same period last year (Q2FY24).

Stay Connected, Stay Informed –

Don’t miss out on exclusive updates, market trends, and real-time investment opportunities. Be the first to know about the latest unlisted stocks, IPO announcements, and curated Fact Sheets, delivered straight to your WhatsApp.