Planify Feed

Date: Tue 23 Dec, 2025

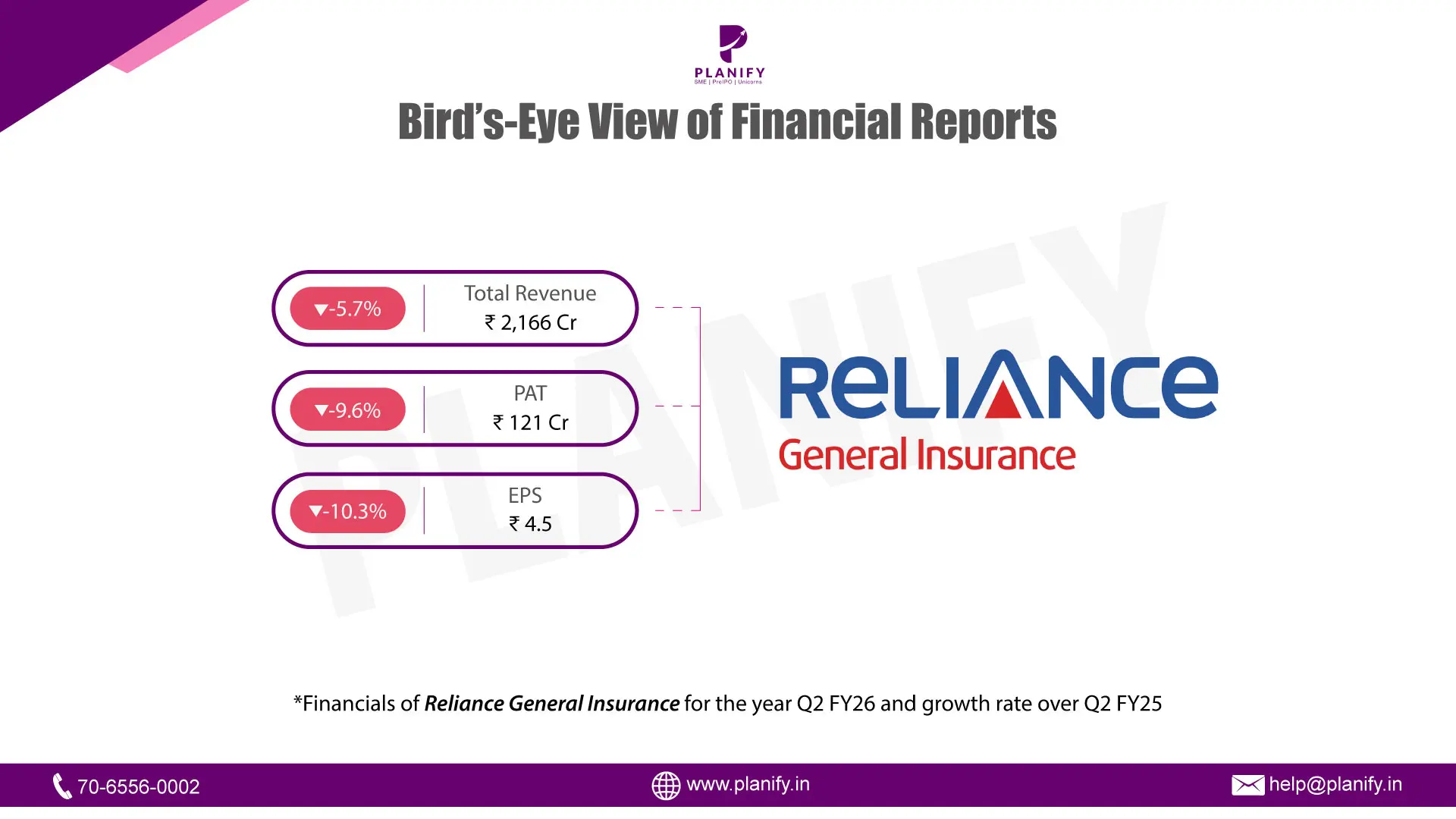

Financial Performance (Q2 FY26 vs Q1 FY25): IndusInd General Insurance reported a moderated financial performance in Q2 FY26, with total revenue declining by 5.7% to ₹2,166 crore, compared to ₹2,296 crore in Q1 FY25. The dip suggests a slight contraction in top-line growth during the period. Profit After Tax (PAT) declined by 9.6% to ₹120.5 crore, compared to ₹133.36 crore in Q1 FY25. Consequently, Earnings Per Share (EPS) decreased by 10.3% to ₹4.51, from ₹5.03 in the previous period. The simultaneous decline in revenue and profitability points to potential pressures on premium collections or investment income, impacting the overall bottom line.

Operational Metrics (Q2 FY26): Operational performance highlights a substantial volume of business activities. The total number of policies issued during the current year stood at 49,70,736, indicating a very strong market presence. Claims activity was also significant, with 27,13,250 claims registered during the current year. Service efficiency metrics showed 1.16 policy-related complaints per 10,000 policies and 4.44 claim-related complaints per 10,000 claims. The grievance redressal mechanism appeared robust, with the majority of pending complaints (1,205) being less than 15 days old, reflecting a focus on timely resolution.

Strategic Developments: The company is operating under a new identity, having transitioned from Reliance General Insurance Company Limited to IndusInd General Insurance Company Limited. This rebranding likely marks a significant strategic pivot, possibly aligning with broader group objectives or ownership changes. The high volume of policies and claims underscores the company's continued operational scale despite the financial dip. While specific capital allocation details for this quarter were not highlighted in the snippets, the operational data suggests a continued emphasis on maintaining service levels and managing a vast customer base amidst the corporate transition.

Date: Mon 22 Dec, 2025

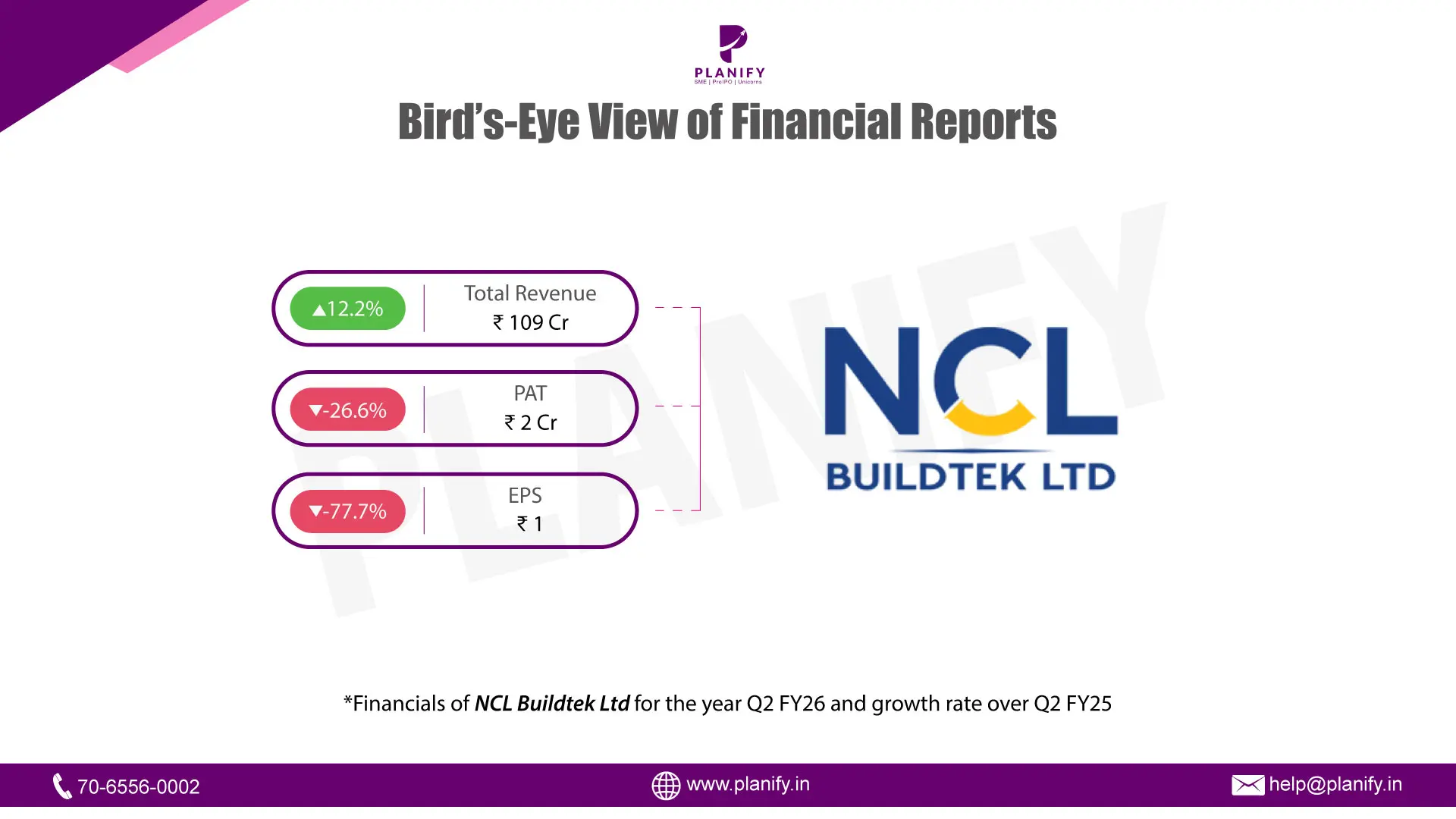

Financial Performance (Q2 FY26 vs Q2 FY25): NCL Buildtek Ltd reported a mixed set of numbers for Q2 FY26. Revenue from Operations (Consolidated) increased by 12.2% year-on-year (YoY) to ₹10,852.52 lakh, compared to ₹9,673.59 lakh in Q2 FY25. However, despite the growth in topline, Profit After Tax (PAT) declined by 26.6% YoY to ₹234.64 lakh, down from ₹319.51 lakh in the same quarter last year. This drop occurred even though Profit Before Tax (PBT) (after exceptional items) rose to ₹333.14 lakh from ₹194.81 lakh in Q2 FY25. The decline in PAT was primarily driven by a significant tax expense of ₹98.50 lakh in the current quarter, compared to a tax credit adjustment in the previous year. Consequently, Earnings Per Share (EPS) (including exceptional items) fell to ₹1.22 from ₹5.47 in the corresponding period last year.

Operational Metrics (Q2 FY26 vs Q2 FY25): Operational performance varied significantly across business segments. The Coatings segment posted strong growth, with revenue rising to ₹2,560.97 lakh from ₹2,188.84 lakh last year, and segment profit nearly doubling to ₹341.56 lakh. The Windoors segment remained the largest contributor, with revenue increasing to ₹5,867.59 lakh from ₹4,863.83 lakh. However, margins remained tight; the consolidated Operating Margin stood at 5%, while the Net Profit Margin was recorded at 2% for the quarter. The Interest Coverage Ratio was reported at 1.56 times, reflecting the impact of finance costs, while the Debtors Turnover Ratio stood at 1.88 times.

Strategic Developments: During the quarter, the company recorded an exceptional item gain of ₹79.99 lakh, which supported the profit before tax figures. While the Windoors and Coatings divisions showed resilience and growth, the Walls segment faced headwinds, reporting a segment loss of ₹84.08 lakh compared to a minor loss of ₹0.98 lakh in Q2 FY25. The company’s consolidated Net Worth stood at ₹23,060.09 lakh as of September 30, 2025, maintaining a stable capital base despite the pressure on bottom-line profitability. The financial results were reviewed by the Audit Committee and approved by the Board of Directors on November 13, 2025.

Date: Mon 22 Dec, 2025

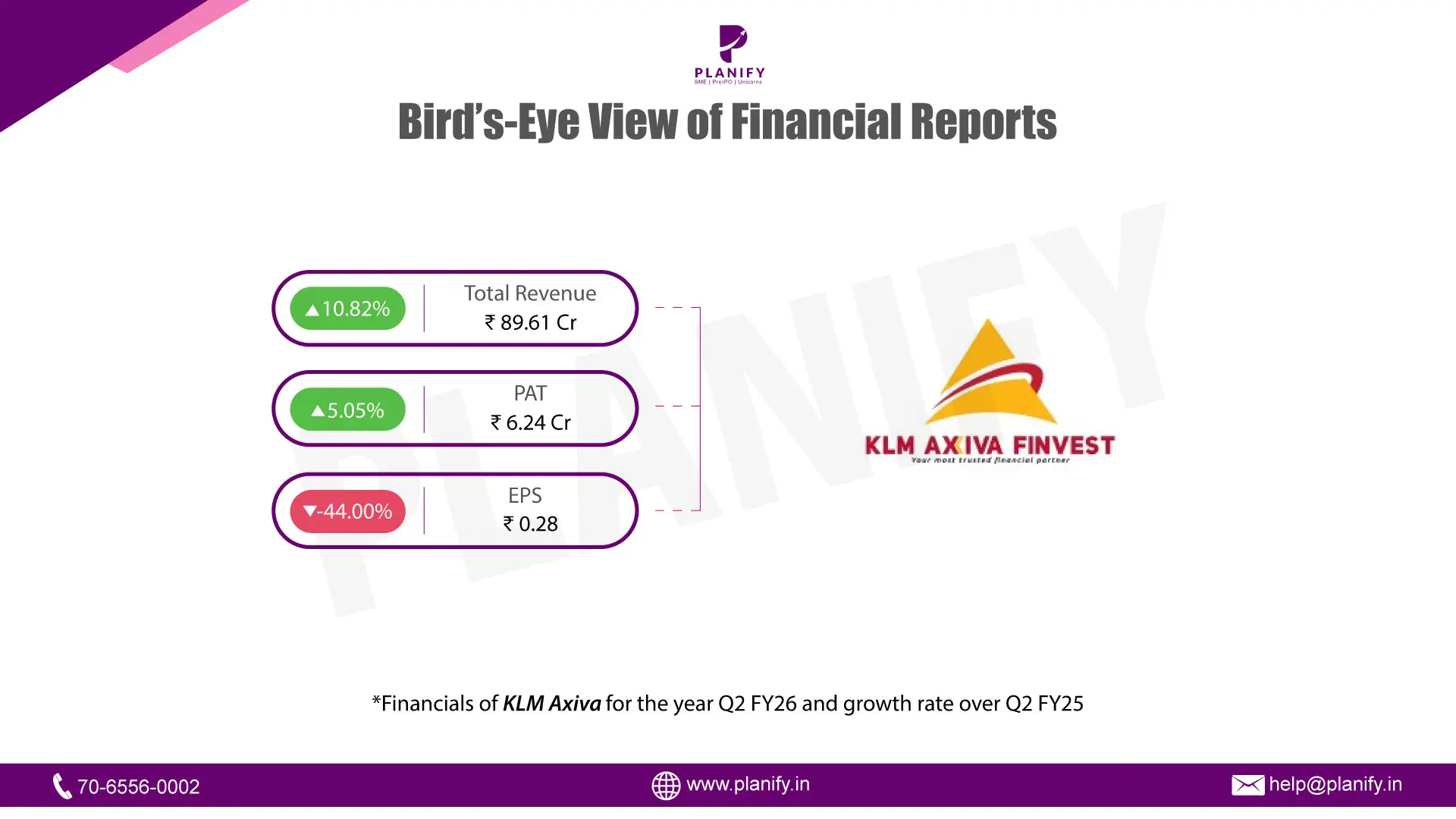

Financial Performance(Q2 FY26 vs Q2 FY25): KLM Axiva Finvest reported a mixed financial performance in Q2 FY26, with total income increasing marginally by 10.82% year-on-year (YoY) to ₹89.61 crore, compared to ₹80.86 crore in Q2 FY25. The modest growth was primarily supported by stable interest income, while other income also contributed during the quarter. Profit After Tax (PAT) increased by 5.0% YoY to ₹6.2 crore, compared to ₹5.9 crore in Q2 FY25. Earnings Per Share (EPS) stood at ₹0.28, lower than ₹0.50 reported in the same quarter last year.

Operational Metrics (Q2 FY26 vs Q2 FY25): Operational performance during the quarter reflected pressure on profitability metrics. Operating margin declined to 4.2% in Q2 FY26 from 7.6% in Q2 FY25, while net profit margin moderated to 1.2% from 3.6% in the previous year. The interest service coverage ratio stood at 1.08 times, indicating tighter coverage compared to historical levels due to higher finance costs. The debt-to-equity ratio remained elevated at 5.4 times, reflecting the leveraged nature of the balance sheet.

Strategic Developments: Net worth stood at ₹291.1 crore as of September 2025, providing capital support for ongoing operations. The company continues to focus on its core lending activities, with no material changes in business segments or strategy during the quarter. Overall performance in Q2 FY26 reflects stable loan growth and asset quality, while profitability remained under pressure due to higher costs and leverage.

{kind=link}

Date: Mon 22 Dec, 2025

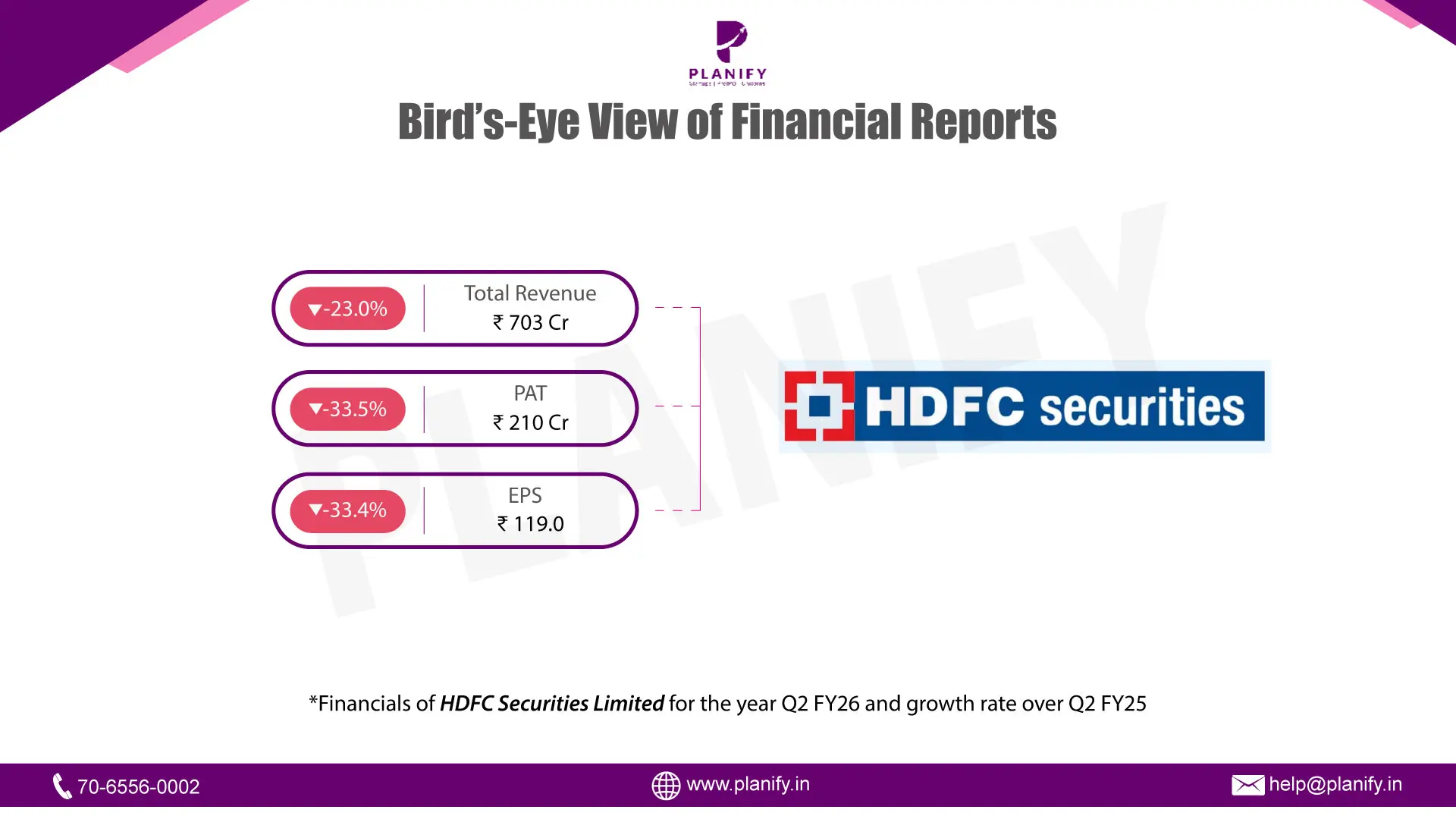

- Financial Performance (Q2 FY26 vs Q2 FY25): HDFC Securities reported a weaker financial performance in Q2 FY26, with total revenue declining by 23.2% year-on-year (YoY) to ₹701 crore, compared to ₹913 crore in Q2 FY25. The decline was mainly due to lower fees and commission income along with losses on fair value changes during the quarter. Profit Before Tax (PBT) fell by 31.6% YoY to ₹282 crore from ₹412 crore in the same quarter last year. Profit After Tax (PAT) declined by 33.2% YoY to ₹211 crore, compared to ₹315 crore in Q2 FY25. Earnings Per Share (EPS) also declined by 33.8% YoY to ₹118.2, from ₹178.5 last year.

- Operational Metrics (Q2 FY26 vs Q2 FY25): Operational performance saw pressure on margins during the quarter. Operating margin declined to 40% in Q2 FY26 from 45% in Q2 FY25, while net profit margin reduced to 30% from 35% last year. The interest service coverage ratio stood at 2.9 times, slightly lower than 3.0 times in Q2 FY25, reflecting higher finance costs. The debt-to-equity ratio remained elevated at 3.39 times, while debtors turnover improved to 0.9 times from 0.8 times, indicating better collection efficiency.

- Strategic Developments: During the quarter, the company allotted 83,382 equity shares under employee stock option schemes and granted 17,250 stock options, continuing its focus on employee retention. HDFC Securities also declared and paid an interim dividend of ₹90 per share, reflecting confidence in cash flows despite near-term earnings pressure. The GIFT City subsidiary remains small and had no material impact on consolidated performance. The company’s net worth increased to ₹3,520.1 crore, up 10.9% YoY, providing a strong capital base. The financial performance during the quarter reflects prevailing capital market conditions, including lower trading activity and subdued investor participation. While near-term results remain linked to market sentiment, the company’s prudent risk management and stable client base support long-term sustainability.

Date: Mon 22 Dec, 2025

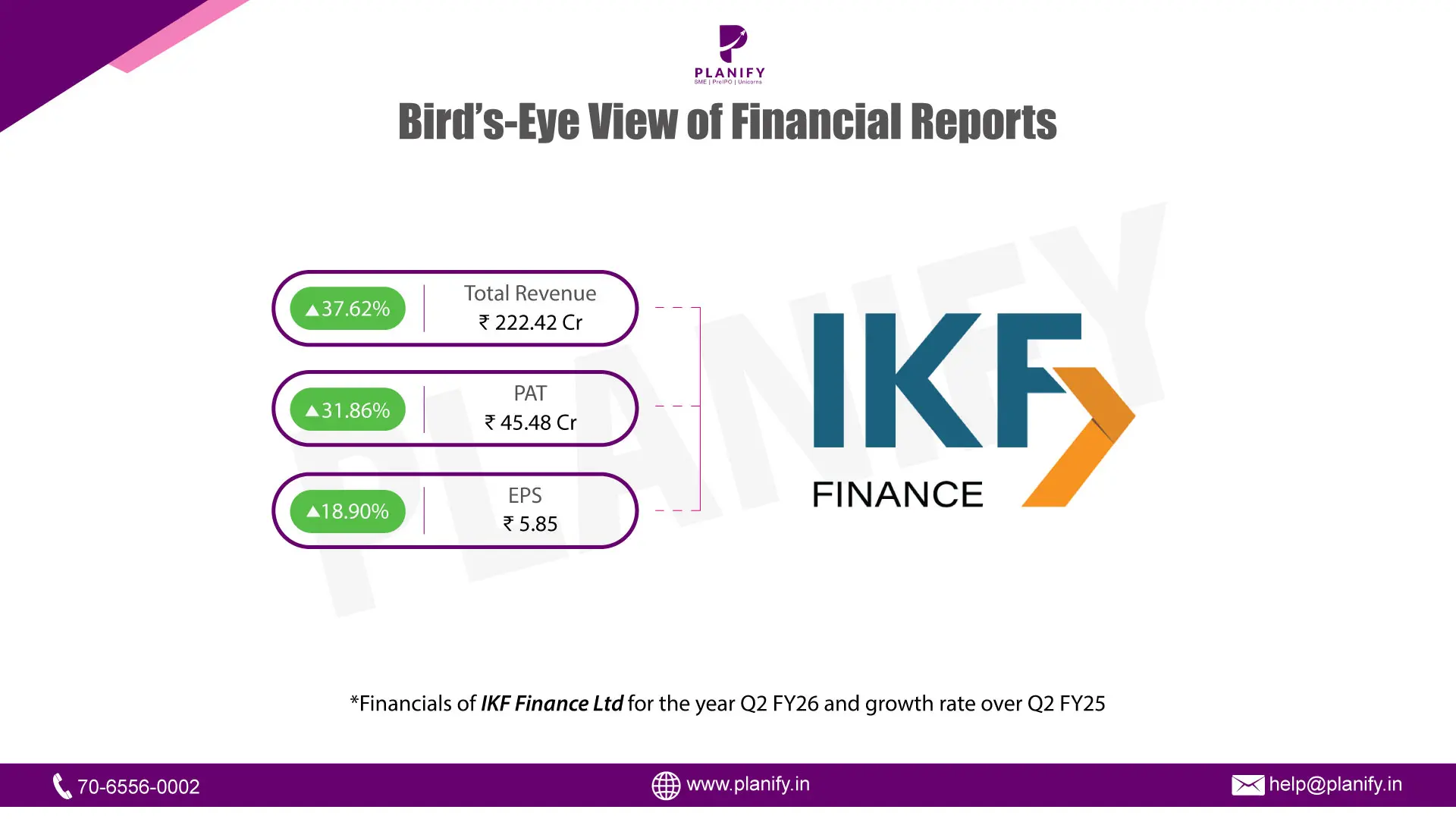

Financial Performance (Q2 FY26 vs Q2 FY25): IKF Finance reported a strong financial performance in Q2 FY26, with total income increasing by 37.6% year-on-year (YoY) to ₹222.42 crore, compared to ₹161.62 crore in Q2 FY25. The growth was primarily driven by a sharp rise in interest income, which grew 39.4% YoY to ₹207.2 crore, supported by steady loan book expansion and stable yields. Profit Before Tax (PBT) rose by 31.8% YoY to ₹61.0 crore from ₹46.3 crore in the corresponding quarter last year, despite higher impairment charges. Profit After Tax (PAT) increased by 31.9% YoY to ₹45.5 crore, compared to ₹34.5 crore in Q2 FY25. Earnings Per Share (EPS) improved to ₹5.85, up from ₹4.92 reported in the same quarter last year.

Operational Metrics (Q2 FY26 vs Q2 FY25): Operational performance remained healthy during the quarter, supported by operating leverage and cost discipline. Net profit margin stood at 20.2% in Q2 FY26, broadly stable compared to 21.0% in Q2 FY25, despite elevated credit costs. The debt-to-equity ratio improved meaningfully to 2.31 times from 3.54 times last year, reflecting balance sheet strengthening through equity infusion. Capital adequacy remained strong at 30.9%, well above regulatory requirements.

Strategic Developments: During the quarter, IKF Finance strengthened its balance sheet through preferential allotment of equity shares, supporting growth and deleveraging. Net worth increased sharply to ₹1,798.8 crore as of September 2025, up 92.6% YoY. The loan book expanded to ₹4,946.3 crore, reflecting steady disbursement momentum. The company maintained adequate liquidity, with a liquidity coverage ratio of 594.1%, providing comfort on near-term obligations. Overall performance in Q2 FY26 reflects strong growth momentum, improving leverage metrics, and stable asset quality, with credit costs and funding conditions remaining key monitorables going forward.

Date: Thu 18 Dec, 2025

For decades, Studds has been synonymous with affordable, mass-market helmets.

Studds Accessories Limited formally an Indian manufacturer of two-wheeler helmets and motorcycle accessories has been a dominant name in head protection for riders.

Founded in 1983 by the Khurana family, with Madhu Bhushan Khurana and Sidhartha Bhushan Khurana in leadership roles, Studds Accessories has spent nearly four decades building India’s largest helmet manufacturing business. The company’s portfolio spans full-face, open-face, flip-up helmets and a range of riding gear marketed under its own brand names: Studds and SMK.

From Mass to Premium: The Strategic Shift

India’s largest two-wheeler helmet maker is accelerating its shift up the value chain, aiming to double the share of premium helmets in its revenue mix over the next two years, a move that signals changing consumer behaviour as much as corporate strategy.

According to industry commentary and statements from the company’s Managing Director, Studds Accessories expects to double the revenue share of premium helmets from around 15.5% to ~30% within the next two years.

The backdrop is compelling. India remains the world’s largest two-wheeler market, but helmet consumption is evolving beyond basic compliance. Rising disposable incomes, stricter safety awareness, and aspirational buying especially among urban riders are pushing demand toward higher-priced, feature-rich helmets. Studds is positioning itself right at this intersection.

- Premium helmets, typically priced multiple times higher than entry-level models, offer structurally better margins. For Studds, this means profit growth can outpace volume growth, even if overall industry demand remains steady.

- The company has been expanding its premium portfolio with better ventilation systems, lighter materials, aerodynamic designs, and global safety certifications, features that appeal to both domestic riders and export markets.

- Exports are another quiet lever. Studds already has a strong overseas presence, and premium products improve competitiveness in developed markets where pricing power is higher and safety norms are tighter. As premium penetration rises, average realisation per helmet improves, reducing dependence on sheer volume-led growth.

Date: Wed 17 Dec, 2025

What began as a ₹75-lakh funding pitch on Shark Tank India has translated into tangible market gains for investors. Ravelcare, the personal-care brand that gained early visibility through the show, delivered a ~55% listing premium on its SME IPO turning a televised pitch into a real capital-market outcome.

About Ravelcare

Ravelcare began as a digital-first beauty and personal care brand founded in 2018 by Ayush Varma, offering personalised haircare, skincare, and bodycare products through its own website and major marketplaces like Amazon, Flipkart, and Myntra. Its early strategy combined data-driven formulation with direct-to-consumer engagement, a model that helped it carve out a niche in a highly competitive category.

Shark Tank India Spotlight

- Ravelcare appeared on Shark Tank India Season 2, where Ayush Varma pitched for ₹75 lakh for a 2.5% equity stake, valuing the business at around ₹30 crore. The show created a significant boost in brand awareness and online traction. In the episode, investor Anupam Mittal offered ₹75 lakh for a 10% stake, with the condition that the company hit projected numbers within two years.

- However, public records and reporting do not confirm any post-show deal actually closing on those terms. What the brand did gain from the exposure was elevated consumer recognition and stronger engagement, which helped bolster demand heading into its IPO.

RavelCare IPO Performance

The IPO drew exceptional investor interest, with overall subscription reaching 437.6 times, led by retail, NII, and QIB bids. Anchor investors had already committed ₹6.83 crore before the public bid opened.

On December 8, 2025, Ravelcare debuted on the BSE SME platform at around ₹201 per share, roughly a 55% premium above its ₹130 issue price, marking a rare and strong listing performance for an SME consumer brand.

The Shark Tank appearance served more as a brand catalyst than a traditional funding milestone. Its real value for investors lies in the company’s execution track record, retail traction, and how effectively it deploys capital toward deeper penetration, distribution, and manufacturing integration.

Date: Sun 14 Dec, 2025

Do you know India’s first indigenous thrombectomy device is being built by S3V Vascular?

It’s the same company that secured India’s first licence for an expandable titanium spinal cage, placing it at the frontier of neuro-spine innovation.

S3V Vascular Technologies, the Mysuru-based med-tech manufacturer, is emerging as one of India’s most ambitious players in neurovascular and cardiovascular devices. The company has spent the past decade building capabilities across stents, balloons, microcatheters, and guidewires.

- Backed by the Government of India’s Technology Development Board, S3V is developing India’s first fully indigenous mechanical thrombectomy device, a life-saving tool used to remove blood clots in stroke patients, a category long dominated by expensive imports.

- S3V Vascular Technologies had earlier attracted backing from veteran investor Madhusudan Kela, reinforcing confidence in India’s indigenous medtech innovation story.

S3V’s product family includes coronary devices (PTCA balloon catheters; 3V Paulo), stent systems (3V Siris/3V Neil), hydrophilic PTCA balloons, and newer neurovascular lines (Krome, clot-retriever concepts). The company is explicitly pursuing patents on key thrombectomy and catheter-construct innovations. That IP push is central to its strategy to move up the value chain, from contract manufacturing to proprietary, higher-margin devices.

S3V raised significant private capital (reported ~₹300 crore in a recent funding round) from high-profile investors and industrial backers, and has committed capex for an integrated manufacturing unit, previously reported as a ₹70–300 crore scale investment depending on the phase of facility buildout.

Date: Sun 14 Dec, 2025

Sun Drops Energia Private Limited, part of the KP Group and known for its presence in solar power EPC and clean-energy solutions has taken a major step toward scaling its corporate structure.

The company has formally called an Extraordinary General Meeting (EGM) on December 29, 2025, seeking shareholder approval to convert from a private limited company into a public limited company.

Sun Drops Energia Private Limited, the renewable energy arm of the KP Group’s KPI Green Energy platform, has strengthened its project pipeline by securing new contracts to develop solar power projects totaling 62.20 MW under the Captive Power Producer (CPP) segment. This order builds on Gujarat’s renewable energy push and expands the company’s operational footprint in the utility-scale solar sector.

- Under India’s Distributed Renewable Energy Bilateral Purchase (DREBP) Policy and the Gujarat Renewable Energy Policy-2023, Sun Drops Energia won Letters of Award from multiple clients to execute the projects, expected to be completed by FY 2025-26 in phased tranches.

- This 62.20 MW addition brings the unit’s CPP portfolio to 152.34 MW, underpinning a broader order book of 1.60 GW in captive solar commitments held by KPI Green Energy and its subsidiaries.

- Converting Sun Drops Energia into a public entity positions it to scale aggressively into solar, hybrid power, and emerging BESS opportunities.

With expanding project wins, a deeper order pipeline, and a planned IPO on the horizon, Sun Drops Energia is shaping up as KPI Green's next growth engine aiming to move from a fast-scaling subsidiary to a capital-powered renewable platform.

Date: Fri 12 Dec, 2025

India’s mutual fund industry is on the cusp of a landmark moment as ICICI Prudential Asset Management Company prepares for its long-awaited IPO directly stepping into comparison with the listed heavyweight HDFC AMC.

While HDFC AMC currently manages an AUM of ₹8.81 lakh crore with a market capitalisation of ₹1.10 lakh crore, ICICI Prudential AMC already commands a larger AUM of ₹10.87 lakh crore, making it the bigger asset manager by scale even before listing.

At the proposed IPO valuation of ₹1.07 lakh crore, ICICI Prudential AMC is entering the markets almost neck-to-neck with HDFC AMC’s current valuation, signaling aggressive confidence in its franchise strength, distribution depth, and profitability profile.

ICICI Prudential AMC looks to diversify into alternative asset classes

Share Price vs IPO Band

HDFC AMC Price: ₹2,646

ICICI Prudential AMC IPO Band: ₹2,061 – ₹2,165

Return on Equity (ROE)

HDFC AMC: 32.4%

ICICI Prudential AMC: 82.8%

(Nearly 2.5× higher capital efficiency)

Market Share

HDFC AMC: 11.5%

ICICI Prudential AMC: 13.3%

(ICICI leads in industry share.)

AUM:

ICICI: ₹10.87 lakh crore

HDFC: ₹8.81 lakh crore

ICICI is bigger.

P/B Ratio:

ICICI Prudential AMC: 10.3–10.8x

HDFC AMC: 14.2x

ICICI is cheaper.

- ICICI Prudential AMC is all set to open its IPO from December 12, 2025, a move that could reshape how investors view mutual-fund houses in the public markets.

- And interestingly, it’s the same business model through which Planify investors previously created substantial returns with HDFC AMC during its pre-IPO phase.

The question now is: could ICICI Prudential AMC be the next big opportunity?

The company’s biggest strength is its scale, and given the success Planify investors saw in HDFC AMC, another major opportunity in the same sector is now coming into view.

Date: Fri 05 Dec, 2025

Garuda Aerospace founded by Agnishwar Jayaprakash has formally converted itself into a public company, dropping “Private” from its name as a preparatory step toward a potential IPO.

To strengthen governance ahead of a potential listing, the company has also added new independent directors to its board.

Solid FY25 Performance

- In FY25, Garuda posted ₹118 crore in revenue, up from ₹110 crore in FY24.

- Profit After Tax stood at ₹17.5 crore, continuing a streak of profitability in a typically capital-intensive industry.

- For FY26, the company targets ₹365 crore in revenue, pointing to aggressive growth plans backed by expanding manufacturing and export ambitions.

- The firm boasts India’s largest commercial drone fleet: 400+ drones and 500 trained pilots, operating across 84 cities, producing over 30 drone models and offering 50+ services.

What Makes Garuda Stand Out — Strategy & Strengths

Strong funding backing: In April 2025, Garuda raised ₹100 crore in a Series B led by Venture Catalysts; later followed by investment from Narotam Sekhsaria Family Office and existing backers, boosting firepower ahead of public listing.

Scaling manufacturing capacity: With plans to ramp up production from 8,000 drones per year to 12,000–15,000, the company is building a production base comparable to global drone manufacturers.

Regulatory get-rights and export licence: Garuda has secured DGCA certifications, and won export clearances to ship drones to markets like US, Australia, and Middle East paving way for global ambitions.

Diversified use-cases beyond agriculture: From precision agriculture and disaster relief to defence-grade drones and logistics solutions , Garuda targets multiple high-growth verticals, reducing reliance on a single segment.

These advantages place Garuda as one of the few drone-tech firms in India with a credible path to scale, export, and diversified business models.

Date: Fri 05 Dec, 2025

Wakefit Innovations, one of India’s leading home-and-sleep solutions brands, opens its IPO subscription window on December 8, 2025.

The offer comprises a fresh issue of roughly ₹377 crore plus an Offer-for-Sale, valuing the company at around ₹6,000–6,400 crore.

Backed by promoters Ankit Garg and Chaitanya Ramalingegowda, Wakefit has moved beyond mattresses and built a diversified home-furnishing portfolio; beds, sofas, wardrobes, décor, and more, sold through online, offline, and its own stores.

Over the years, the company has quietly built a vertically integrated engine:

The IPO is expected to strengthen working capital, expand manufacturing capacity, and deepen Wakefit’s presence across Tier-2/3 India, markets that now contribute more than 45% of sales.

FY25: Growth Amid Losses

- Revenue from operations rose about 29–30% in FY25 to ₹1,305 crore.

- The company remained EBITDA-positive with ₹90.8 crore EBITDA in FY25.

- However, net loss widened to ₹35 crore, compared with ₹15 crore loss in FY24, driven by higher operating expenses including material, marketing and store expansion costs.

- In H1 FY26 alone (six months through Sept 2025), Wakefit reported ₹741 crore revenue and a small profit after tax of ₹35.5 crore, suggesting early signs of turnaround post-IPO filing.

With its tightly integrated manufacturing engine, expanding omni-channel footprint, and a growing home solutions portfolio, Wakefit enters the public markets with the fundamentals of a business built for scale, a mix that makes the IPO worth watching.

Date: Tue 02 Dec, 2025

OYO’s parent company, PRISM, is finally putting its long-awaited public-listing story back on track.

PRISM, the parent company behind OYO, is making its most serious IPO push yet. It has called an Extraordinary General Meeting (EGM) on 20 December 2025 to seek shareholder approval for a ₹6,650-crore fresh equity raise. At the same time, it has proposed a 1:19 bonus share issue, with December 5 set as the record date.

Alongside the IPO, shareholders will vote to increase authorised share capital to ₹2,491 crore, a structural move signaling readiness for significant public-market commitments.

A Company Built for Scale, Now Rebuilt for Discipline

OYO founded by Ritesh Agarwal, scaled faster than any Indian hospitality startup, branding thousands of hotels, homestays, and vacation homes across India, Europe, and Southeast Asia.

But hyper-expansion came with high burn, lease obligations, and inconsistent property economics.

The last two years have been about repair, not expansion.

- PRISM has reduced costs, tightened compliance, improved hotel partner incentives, and focused on profitable geographies.

- The company’s shift back to a franchise-first, asset-light model has improved cash flows and reduced volatility.

- PRISM is cleaning up governance, revising authorized share capital, and simplifying shareholder tiers.

All this, signals the first meaningful step toward that future. Can the Hospitality Giant Finally Earn Public-Market Trust?

OYO’s rebound will ultimately be judged by its ability to turn improving occupancy into steady, year-round margins only then will public markets may reward it with a valuation grounded in fundamentals rather than optimism.

Date: Sat 29 Nov, 2025

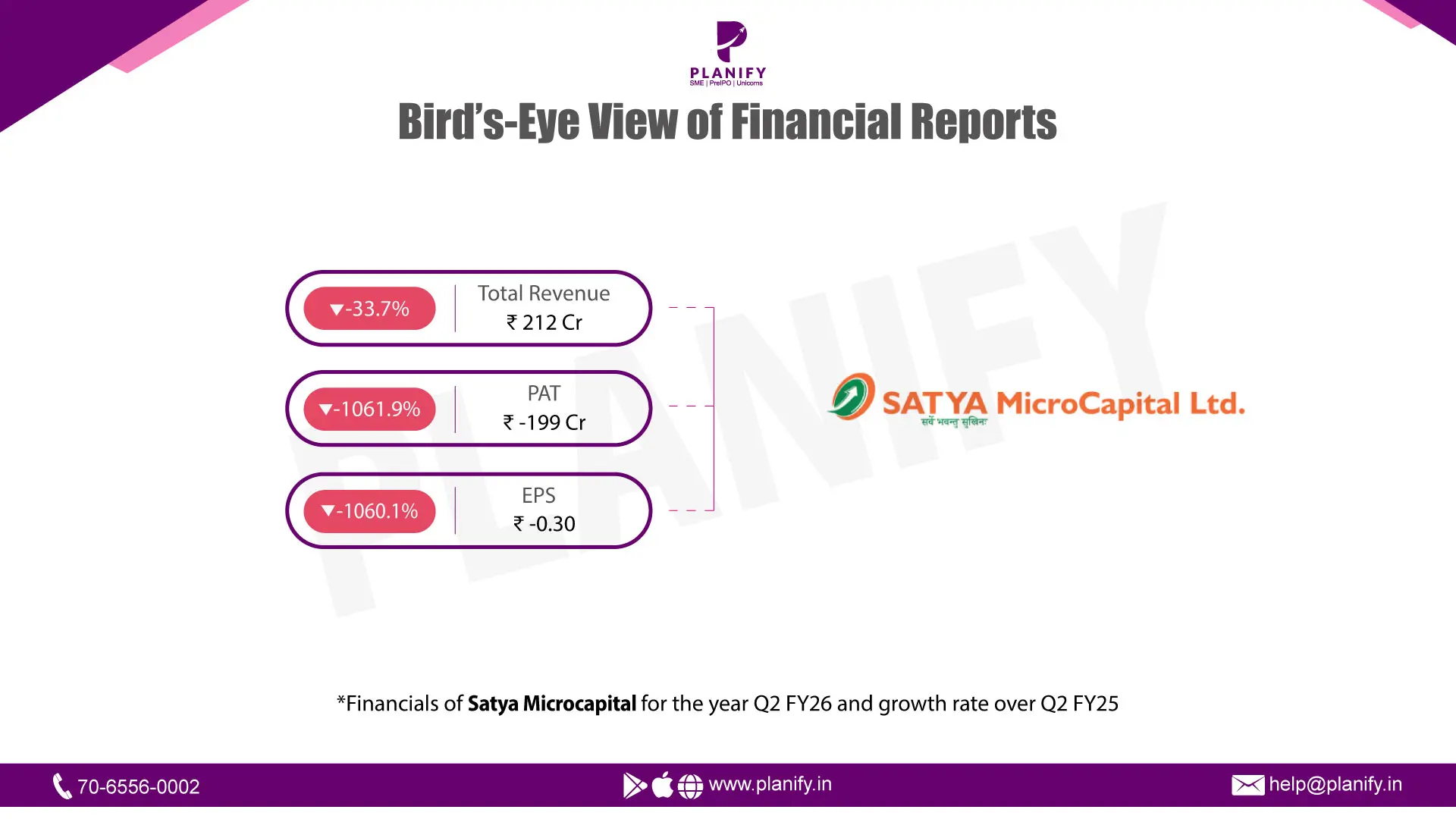

- Financial Performance (Q2 FY26 vs Q2 FY25): In Q2 FY26, Satya Microcapital reported total income of ₹212 crore, down 33.7% YoY from ₹320 crore in Q2 FY25. Interest income dropped to ₹182 crore, down 34.4% YoY from ₹277 crore, while fee/commission income also fell significantly. Though Finance costs decreased sharply to ₹121 crore, down 18.3% YoY from ₹148 crore, Impairment on financial instruments remained high at ₹92 crore, up 364.6% YoY (vs ₹19.7 crore last year), driven by higher expected credit losses. As a result, Profit Before Tax (PBT) came in at a steep loss of ₹156 crore, compared to a profit of ₹28 crore in Q2 FY25 — a deterioration of 662.5% YoY. Profit After Tax (PAT) stood at a loss of ₹199 crore, significantly worse than the ₹21 crore profit in Q2 FY25. Basic EPS for the quarter was ₹(30.34) compared to ₹3.16 a year earlier.

- Operational Metrics (Q2 FY26 vs Q2 FY25): Gross NPA (GNPA) ratio stood at 12.51%, worsening from ~1.2% a year ago, while Net NPA (NNPA) was 6.56% (vs 0.42% in FY25), reflecting severe portfolio stress. The Provision Coverage Ratio (PCR) was 50.94%, lower than the previous year’s 65% level, suggesting a reduced buffer against potential portfolio risks. Capital adequacy remained weak at 11.16%, below the RBI requirement of 15%, though it improves to 15.92% post the November 2025 equity infusion as disclosed. The loan book on the balance sheet was ₹2,938 crore as of Sept 30, 2025, down sharply from ₹3,535 crore in FY25, reflecting portfolio contraction amid elevated credit costs. Total assets were ₹4,439 crore, lower than March 31, 2025 levels (₹5,599 crore), driven by reduced disbursements and deleveraging. Net worth stood at ₹597 crore, significantly lower due to accumulated losses, compared to ₹959 crore as of March 31, 2025.

- Strategic Developments: Satya Microcapital’s Q2 FY26 results indicate a period of acute financial stress. The business reported a steep fall in revenue combined with a surge in credit costs, leading to heavy losses. Asset quality weakened sharply, with GNPA jumping to over 12% and NNPA crossing 6%, pressuring provisioning and capital ratios. The company also breached key regulatory thresholds — CRAR fell to 11.16% and qualifying asset ratio dropped below 60%, both highlighted by auditors. However, Satya undertook corrective steps: a ₹101.9 crore equity infusion in November 2025 improved CRAR to 15.92%, and management has stated that discussions with investors and lenders are ongoing for further capital support. The loan book contraction and decline in total assets show that Satya is operating in a risk-containment mode, prioritizing recoveries and liquidity over growth. Going forward, stabilizing asset quality, rebuilding capital buffers, improving recoveries, and restoring lender confidence are essential for operational continuity. The next few quarters remain crucial as the company attempts to regain regulatory compliance, strengthen collections, and gradually normalize disbursements.

Date: Sat 29 Nov, 2025

PharmEasy was once heralded as India’s health-tech unicorn, a one-stop digital pharmacy + diagnostics + tele-health platform.

But by 2024, heavy losses, falling valuations and management changes had shaken investor confidence.

API Holdings (the parent) had grown aggressively through acquisitions like Thyrocare, but the integration was messy and cash burn worsened.

Now, under its new CEO Rahul Guha, PharmEasy is making bold moves to shift from “growth at any cost” to “profitable, sustainable scale.

And the numbers now reflect a business that is finally pulling itself back.

- PharmEasy reduced its net loss by ~40% in FY25, even with flat revenue of ₹5,872 crore, showing meaningful operating discipline.

- Procurement efficiency jumped from ~40% to nearly 85%, sharply reducing cost leakages and improving margins.

- High-cost loans were refinanced, lowering interest burden and stabilizing API Holdings’ balance sheet.

- The company shut non-core experiments and redirected capital to high-margin, recurrence-heavy segments chronic medication, diagnostics, and in-house procurement.

- Thyrocare’s diagnostics arm showed a turnaround too, giving the group a profitable anchor and smoother cash flows.

- Monthly burn dropped from ~₹50 crore to under ₹2 crore, marking one of the fastest burn reductions in Indian health-tech.

So, while top-line growth is modest, bottom-line stress has eased and that’s a critical first step for any turnaround.

It’s fair to say, based on the latest data that PharmEasy is showing margin improvement and financial stabilization. The internal procurement, cost control, and debt / expense rationalization have helped reduce burn and shrink losses.

But the business remains loss-making as of FY25. Until EBITDA turns positive and the core pharmacy business becomes cash-flow positive, the margin story remains cautiously optimistic.

Now, PharmEasy is no longer the high-burn startup chasing growth at any cost. It’s trying to become a lean, recurring-revenue healthcare services engine with scale, sustainability, and clarity.

Stay Connected, Stay Informed –

Don’t miss out on exclusive updates, market trends, and real-time investment opportunities. Be the first to know about the latest unlisted stocks, IPO announcements, and curated Fact Sheets, delivered straight to your WhatsApp.